Settlement of Claims in Insurance: A CXO Guide to Mastering the Process

When an insurer settles a claim, they’re making good on their promise. It’s the moment they pay you, the policyholder, for a loss that’s covered by your policy. For any business leader, this process isn't just an administrative chore; it's a make-or-break moment that tests your company's financial resilience and public reputation.

A smooth settlement showcases operational excellence, while a difficult one can expose your organization to significant financial and reputational risk.

Why Claim Settlement Is a C-Suite Priority

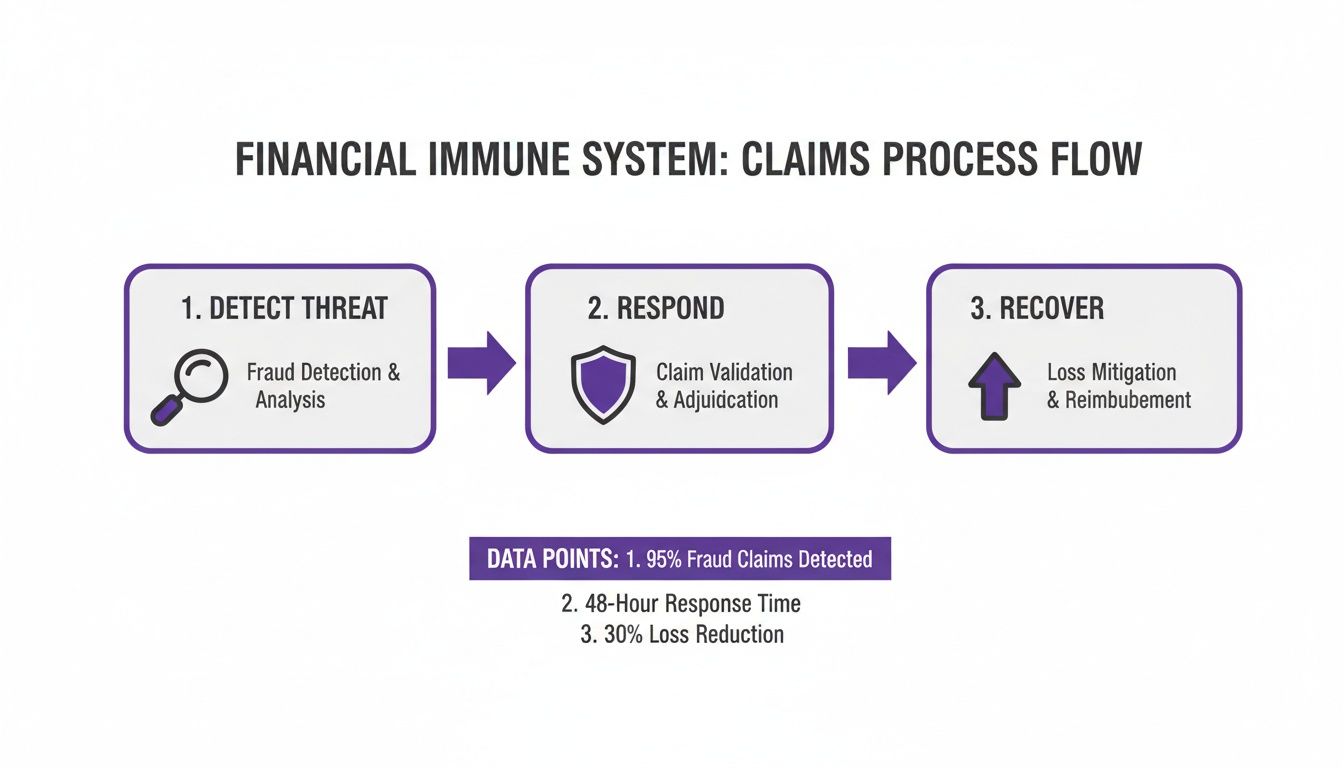

It’s easy for senior executives to see the claims process as a back-office function—a necessary but unglamorous part of managing risk. This is a strategic misstep. Think of your company’s claim settlement process as its financial immune system. When a crisis strikes—be it a major supply chain disruption, a critical data breach, or catastrophic damage to physical assets—this system determines how quickly and effectively your business recovers.

A well-oiled claims process works just like a healthy immune system. It immediately identifies the threat (the loss), triggers a coordinated response (submitting the claim and initiating the investigation), and works to restore the body to health (the final payout). If that system is slow or inefficient, the initial damage metastasizes, leading to prolonged financial bleed and lasting reputational harm.

A Test of Corporate Resilience

Every claim is a public test of your company's operational integrity. Settling a claim swiftly and fairly sends a powerful signal to your customers, investors, and partners. It demonstrates that your organization is well-managed, resilient, and capable of navigating a crisis effectively.

Conversely, a drawn-out, contentious process broadcasts operational weakness and can rapidly erode trust at every level. This is precisely why proactive oversight from the C-suite is non-negotiable.

For a CXO, mastering the claims process transforms a potential liability into a showcase of corporate integrity. It’s your opportunity to prove that your risk management frameworks aren't just theoretical exercises—they deliver tangible financial recovery when it matters most.

The Strategic Advantage of a Claims-Ready Culture

Ultimately, superior claims management provides a distinct competitive advantage. It means that when a crisis hits, your leadership team isn’t mired in reviewing policy minutiae or scrambling for documentation.

Instead, you can focus on strategic decision-making, confident that the financial safety net you've invested in will function as intended. Instilling this "claim readiness" into your corporate culture is a core leadership responsibility. As we’ll explore in this guide, the insights gained from handling claims can sharpen everything from daily operations to long-term risk strategy.

To see how modern tools are being put to work in this area, you can learn more about speech technology in our recent case studies. This is how you transform the reactive task of settling claims into a powerful strategic asset.

The Five Stages of the Insurance Claim Lifecycle

For any senior leader, it's easy to see insurance claims as just a series of administrative hoops to jump through. But that’s a mistake. The best way to manage a claim is to view it as a predictable, structured business process—one you can actively steer, not just passively endure.

Think of it as a controlled response to a crisis. Each stage has a clear objective, key stakeholders, and crucial decision points that can either accelerate your recovery or bog you down in costly delays. Let's walk through these phases using a high-stakes, all-too-common scenario: a major cybersecurity breach at a financial services firm.

This process is your company's financial immune system in action. It’s designed to move from detecting a threat right through to a full recovery.

The claim isn't just paperwork; it’s the mechanism that allows your business to move from crisis to recovery, ultimately making you more resilient.

The entire lifecycle can be broken down into five distinct phases. Understanding what happens in each, who is involved, and how long it should take is the first step toward mastering the process.

The 5 Stages of the Claim Settlement Lifecycle

| Stage | Primary Objective | Key Stakeholders | Typical Timeline |

|---|---|---|---|

| 1. Notice of Loss | Formally alert the insurer that a covered event has occurred and initiate the claim. | Your internal response team, risk manager, legal counsel, insurance broker. | Immediate to 24-48 hours after discovery. |

| 2. Investigation | Validate the claim against the policy, assess the extent of the loss, and determine liability. | Insurer's claims adjuster, forensic experts, your technical & finance teams. | Days to weeks, depending on complexity. |

| 3. Assessment | The insurer issues a formal coverage determination and an initial valuation of the loss. | Insurer’s claims team, your CFO, legal team, and risk manager. | Weeks to a month after the investigation concludes. |

| 4. Negotiation | Reach a mutually agreeable settlement figure based on evidence and policy interpretation. | Senior leaders from both your organisation and the insurer. | Weeks to months, often the longest phase. |

| 5. Payment & Closure | The insurer pays the agreed amount, and the claim file is officially closed. | Your finance department and the insurer's payment processing team. | Days to a week after the settlement agreement is signed. |

Each stage builds on the last, and a misstep in an early phase can cause significant problems down the line.

Stage 1: The Initial Report or Notice of Loss

This is where it all begins. The Initial Report, officially known as the First Notice of Loss (FNOL), is your formal alert to the insurer that something has happened. Getting this right—and doing it quickly—is absolutely critical. A slow or sloppy notice can give the insurer a reason to question the claim from the get-go.

Executive Example: Your Chief Technology Officer confirms a significant data exfiltration event. Your pre-defined incident response plan is activated. A designated leader immediately contacts your cyber insurance carrier's dedicated claims hotline. The FNOL provides the time of discovery, known facts (even if incomplete), and the immediate containment steps being taken. This prompt, professional action satisfies a critical policy condition and starts the settlement clock on your terms.

Stage 2: Investigation and Assessment

As soon as your notice is in, the insurer assigns a claims adjuster or a full team to dig in. Their job is to verify that the event is covered, figure out the scale of the damage, and determine what the insurer is on the hook for. This is where your organisation's preparation and transparency really shine.

As a leader, your role here is to remove internal friction. Ensure the adjuster receives organized documentation and has direct access to key personnel. This demonstrates good faith and dramatically accelerates the process.

The insurer will want to know everything. For our cybersecurity breach, their investigation will likely involve:

- Forensic Analysis: The insurer's tech experts will work with your IT team to find the root cause and full impact of the breach.

- Documentation Review: They’ll need to see incident reports, system logs, and every invoice for costs you've incurred, from credit monitoring services to PR consultants.

- Liability Evaluation: The team will also assess the risk of lawsuits from customers or fines from regulators.

Stage 3: Negotiation and Coverage Determination

After the investigation wraps up, the insurer will send over a coverage determination. This is their official position: what they believe is covered, what’s excluded, and their opening offer for the value of the loss. It's important to remember that this is almost never the final number. It’s the start of a negotiation.

Your job is to be ready with a well-documented counter-valuation. If there’s a disagreement, it doesn't mean the insurer is acting in bad faith. It usually just comes down to different interpretations of the policy wording or how the loss is calculated.

Executive Example: The insurer’s initial offer for your business interruption loss is 25% lower than your CFO’s projections. Instead of an adversarial response, your team presents data-driven financial models illustrating pre-breach revenue trends and evidence of customer contracts lost as a direct result of the incident. This evidence-based approach transforms a potential conflict into a collaborative exercise to arrive at an accurate figure.

Stage 4: Settlement and Agreement

This is the deal-making stage. The goal is to land on a number that both sides can live with. A successful negotiation ends with a settlement agreement, a binding contract that lays out the final payment amount and releases the insurer from any future liability for this specific incident. This is the moment the claim moves from being a problem to a solution.

Quick and fair claim processing is fast becoming a key measure of an insurer’s quality. For instance, general and health insurers in India managed to settle 81.13% of claims within three months during FY2023-24, highlighting a real push for better efficiency. You can read more about these claim settlement trends and statistics.

Stage 5: Final Payment and Claim Closure

The last step is the wire transfer. The insurer pays the agreed-upon amount, and once the funds are in your account, the claim is officially closed. This injection of capital is the ultimate purpose of your insurance policy—it’s what enables your company to fund recovery, repair its reputation, and restore financial stability. For any CXO, this is the moment that validates your investment in a robust risk management strategy.

Navigating Common Roadblocks: Why Claims Get Delayed or Denied

Everyone wants a smooth, quick claim settlement, but the reality on the ground can be a lot messier. For any senior leader, understanding where the process can break down isn't about pointing fingers—it's about smart risk management. When you can anticipate the common sticking points, you can build them into your company's processes and strengthen your position long before a claim is ever filed.

Often, the line between a straightforward payout and a drawn-out dispute is simply preparation. Knowing the pitfalls is half the battle.

Gaps in Documentation and Reporting

By far, the most common reason for a claim to get bogged down is poor documentation. It's a simple truth: when a loss happens, the burden of proof is on you. If your information is vague, incomplete, or slow to arrive, you’re giving the insurer a perfectly valid reason to hit the brakes while they ask for more detail. This isn't just about shuffling paper; it's about presenting a clear, undeniable case for your loss.

Executive Example: A fire damages a key production line in your factory. You submit a claim, but your asset register hasn't been updated in three years, and maintenance logs are inconsistent. The insurer’s adjuster cannot verify the machinery's existence or value. Your team is now forced into a reactive scramble for old purchase orders and financial statements, stalling the entire process for weeks and delaying critical capital injection.

A claim backed by weak evidence is an open invitation for delays and disputes. As a leader, mandating real-time, accurate documentation is not administrative minutiae—it is fundamental risk mitigation.

Another classic mistake is late reporting. Every policy has a clause that demands you notify the insurer promptly after a loss. Waiting days, let alone weeks, can seriously compromise your claim. It prevents the insurer from doing their own timely investigation, which can be grounds for denial.

The Devil in the Details: Policy Wording and Exclusions

Of course, delays aren't always your fault. A huge number of disputes come down to interpreting the policy itself. The dense language, specific definitions, and long lists of exclusions can lead to honest disagreements about what’s covered and what isn’t. This is especially true for newer risks like cyber attacks or business interruption from non-physical events.

An insurer might reject a claim by citing a specific exclusion they feel applies to your situation.

- A Cyber Scenario: You're hit with ransomware and file a claim. The insurer denies it, pointing to a clause that excludes losses from a "failure to maintain adequate security protocols." They argue your unpatched server voids the coverage.

- A Liability Scenario: A customer claims your product injured them. Your policy, however, excludes "known defects." The insurer finds internal emails where your engineers discussed a potential flaw and uses that to trigger the exclusion.

These examples show exactly why C-suite oversight during policy selection is so critical. Understanding what your policy doesn't cover before an incident is your single best defence against a surprise denial.

Disagreements Over Loss Value and Mitigation

Even when everyone agrees the loss is covered, you can still get stuck on one big question: how much is it worth? You and the insurer can have wildly different views on the financial impact. This is a massive issue in business interruption claims, where putting a number on lost profit involves complex forecasts and assumptions.

Executive Example: Following a key supplier's bankruptcy, your CFO projects a business interruption loss of ₹5 crores, based on optimistic sales growth forecasts. The insurer’s forensic accountant uses more conservative historical data and values the loss at only ₹3 crores. This ₹2 crore gap becomes the new battleground, holding up the entire settlement until it can be resolved through painstaking negotiation.

On top of that, insurers expect you to take immediate, reasonable steps to mitigate the damage after a loss. You can't just sit back and watch things get worse. Failing to act can shrink your payout. For instance, if a pipe bursts, you’re expected to start drying things out right away. If you don’t, and mould grows, the insurer may refuse to cover the mould damage, arguing it could have been prevented.

Understanding Your Obligations for a Smooth Settlement

A fast and fair insurance settlement isn’t a one-sided affair; it's a two-way street built on mutual responsibility. For any business leader, grasping this dynamic is the key to turning a disruptive event into a manageable financial recovery. It’s not just about what the insurer owes you—it’s just as much about what your organisation is obligated to provide.

When a loss happens, the relationship with your insurer suddenly becomes a critical partnership. Each side has clear duties designed to keep the process transparent and moving forward. Fulfilling your end of the bargain isn't just about ticking boxes; it's the most direct route to speeding up the timeline and securing the best possible outcome.

The Claimant’s Core Duties

As the policyholder, your responsibilities are proactive. They set the tone for the entire settlement journey and have a massive impact on its speed and success. It helps to think of these duties not as chores, but as strategic moves that strengthen your claim right from the start.

Here’s what’s expected of you:

- Prompt Notification: You must inform the insurer about a loss as soon as reasonably possible. Unjustified delays can give the insurer grounds to question or even deny the claim, as it impedes their ability to investigate.

- Full Cooperation: You are required to cooperate fully with the insurer's investigation. This means providing timely access to relevant documents, property, and personnel. Obstructing this process is a fast track to a dispute.

- Loss Mitigation: You have a duty to take reasonable steps to prevent further damage after an incident. For example, if a water pipe bursts, you must act quickly to dry the area and prevent mould. Insurers will not cover damages that could have been reasonably avoided.

- Meticulous Proof of Loss: The burden is on you to prove the quantum of your financial loss. This demands detailed, organized, and credible documentation to substantiate every component of your claim.

A well-documented proof of loss is your most powerful negotiating tool. It replaces ambiguity with facts, making it difficult for an insurer to dispute the value of your claim and speeding up the entire settlement of claims in insurance.

The Insurer’s Corresponding Obligations

Just as you have duties, so does your insurer. Their obligations are built on the principle of "good faith and fair dealing," a legal concept that requires them to handle your claim honestly and equitably. Their performance here is a direct measure of their integrity.

The insurer’s key responsibilities include:

- Duty of Good Faith: The insurer must act honestly and fairly, without fabricating reasons to deny a valid claim. They cannot use deceptive tactics or unreasonable delays to coerce you into accepting a low settlement.

- Timely Investigation: Once you’ve reported a claim, the insurer has to start a prompt and thorough investigation. They can't just let it sit on a desk without a good reason.

- Transparent Communication: The insurer must keep you informed about your claim’s status. This includes providing a clear explanation for any decision, whether it’s a payment, a partial denial, or a request for more information.

The industry's commitment to these standards is often reflected in performance metrics. For example, life insurers in India showed strong performance in FY2023-24, collectively settling 96.82% of individual death claims. Private insurers hit an average of 99%, with many top performers settling claims within 30 days. You can find more details on these claim settlement benchmarks.

A Practical Scenario: Product Recall

Imagine your company is forced into a major product recall because of a contaminated component. Fulfilling your duties is what separates a manageable crisis from a financial disaster.

Executive Action: You immediately notify your product recall insurer. Your COO ensures all recalled inventory and samples of the contaminated component are preserved as evidence. Simultaneously, your CFO's team works directly with the adjuster, providing detailed sales figures, production records, and P&L statements to build a robust business interruption claim.

This proactive, cross-functional cooperation enables the insurer to quickly and accurately assess the loss. The result is a faster, more predictable settlement, providing the critical capital your company needs to manage the recall and protect its brand.

Navigating Disputes and Regulatory Hurdles

When an insurance claim settlement stalls, the way forward can feel lost in a fog of legal jargon and red tape. For any senior leader, this is a make-or-break moment. Having a firm grasp of the resolution landscape isn't just helpful—it's a powerful strategic asset. This isn't about winning a fight; it's about making a smart business decision that balances the cost, time, and potential outcome.

Even the most buttoned-up claim can hit a wall. When talks with the insurer break down, you need a clear plan for what comes next. The goal isn't to race into a courtroom, but to work through a set of dispute resolution options, each with its own pros and cons for your business.

Mapping Your Resolution Pathways

When a dispute pops up, you have a few different roads you can take. Each one varies in terms of formality, cost, and how much control you get to keep.

- Mediation: Think of this as a structured, confidential negotiation. A neutral third party—the mediator—facilitates a conversation between your team and the insurer to find common ground. The key advantage is that you retain control; no solution is imposed, and you can walk away if the proposal is not commercially viable.

- Arbitration: This is a more formal, private court proceeding. A neutral arbitrator (or a panel) hears evidence from both sides and then issues a binding decision. It's generally faster and less expensive than litigation, but the decision is typically final, with very limited grounds for appeal.

For a deeper dive into the common challenges and solutions in this process, you can explore this general guide on Navigating Insurance Claims and Disputes.

Choosing between mediation and arbitration is a strategic business decision. Mediation is about collaborative problem-solving to find a mutually acceptable outcome. Arbitration is about presenting your best case and letting an expert make the final call. Your choice depends on your appetite for risk and the strength of your position.

Understanding the Regulatory Framework

Beyond one-on-one disputes, the whole claims game is played within a strict regulatory arena. In India, for instance, the Insurance Regulatory and Development Authority of India (IRDAI) is the referee. The IRDAI sets firm timelines for settling claims, spells out what counts as an unfair practice, and even offers an ombudsman scheme for policyholders who need help.

Knowing that a regulator is watching gives your organisation some serious clout. It forces insurers to operate under a standard of "good faith and fair dealing." If you feel an insurer is dragging its feet or denying a claim without good reason, the regulatory framework gives you a formal complaint channel that can force a fair review—often without the headache and expense of litigation. The legal world itself is also getting smarter about managing these issues; you can see how speech technology is being applied in the legal sector to get better results.

For a CXO, these options aren't just legal boxes to tick. They are strategic tools. Understanding them helps you build a solid business case for any dispute, weighing what you could recover against the cost and disruption to your operations. It’s all about picking the smartest, most efficient path to get the fair settlement your company is owed.

Your Executive Playbook for Faster Claim Settlements

Alright, let's move from theory to action. For any executive, the real goal is to weave a culture of ‘claim readiness’ right into the fabric of the company. It’s about shifting how you think about insurance claims—not as a chaotic, reactive scramble, but as a planned, strategic part of your business. This work starts long before anything goes wrong.

The bedrock of a quick, clean settlement is having a dedicated, cross-functional claims team ready to go. This isn't just one person's job. Pull in people from legal, finance, operations, and risk management. Give them clearly defined roles and a pre-agreed plan for what to do the moment an incident happens. Their immediate, coordinated response is the single biggest factor in getting the process started on the right foot.

The Pre-Loss Strategic Checklist

Getting your house in order beforehand can drastically cut down on the friction and delays later. Think of it as building a robust framework that clicks into place the second a loss occurs, so you’re not wasting precious time hunting for basic information while under immense pressure.

- Establish a Claims Response Team: Assemble a core group with a designated leader who has the authority to communicate directly with your broker and the insurer.

- Centralise Key Documents: Maintain a secure, up-to-date digital repository containing all insurance policies, broker contacts, asset registers, and relevant financial records.

- Develop Communication Protocols: Create standardized templates for the first notice of loss and for internal status updates. This ensures consistent, accurate messaging from day one.

This kind of proactive thinking is more important than ever. For example, in FY25, health insurance claims in India shot up by 21.18%, but the amount paid out only grew by 12.88%. That gap hints at some serious processing bottlenecks. This data really underscores why companies need to be on top of their game.

Managing the Insurer Relationship

How you manage the relationship with the insurer's adjuster is critical. It’s easy to see them as an opponent, but that’s a mistake. View them as a professional partner whose job is to verify the claim and close the file. Your job is to make their job easier.

From the very first phone call, aim for a collaborative, professional tone. Hand over well-organised documents, provide reasonable access for them to do their work, and answer their questions quickly. This builds trust and shows you're acting in good faith, which has a direct and positive impact on how fast things move.

To really get your operations in order and protect against fraud, investing in solid insurance claims management software is a smart executive move. Bringing your process up to date isn't just an IT project; it's a strategic investment in your company's financial stability. You can also learn how AI is revolutionising customer service models in banking, which offers some great lessons on how technology can improve these kinds of high-stakes conversations.

By putting this playbook into practice, you change your company’s role from a passive victim of circumstance to an active, prepared participant in the claims process. This control helps you sidestep delays, strengthens your hand in negotiations, and ultimately ensures your business gets the best possible financial outcome from any claim.

Frequently Asked Questions

As a leader, you need straight answers to tough questions, not operational fluff. Here are the things executives really want to know about settling insurance claims, framed for making smart decisions.

What's the One Thing That Speeds Up a Claim Settlement the Most?

Without a doubt, it's immediate and thorough documentation. The moment an incident happens, you need to start a meticulous record of everything—the event itself, the damage, and every conversation that follows. This builds an undeniable foundation for your claim.

For you, this means having solid internal processes in place before anything goes wrong. Your team needs to know exactly what to capture and how.

A well-documented claim leaves no room for doubt. It cuts down the insurer's investigation time and gives you a much stronger hand when it comes to negotiating. It’s the fastest route to a fair settlement.

How Does Our Company's Claim History Impact Future Premiums?

Your claims history is a primary factor insurers use to calculate future premiums. A pattern of frequent or large claims signals higher risk, often leading to increased premiums or higher deductibles.

However, it's not just about the number of claims; how you manage them matters too. If you can demonstrate proactive risk management and full cooperation during the settlement process, you can often mitigate a significant premium hike.

Executive Example: Your company files a major claim for a supply chain disruption. During your next insurance renewal, you present the insurer with a detailed report on your new, diversified sourcing strategy and enhanced supplier vetting process. By proving that you have addressed the root cause, you can effectively argue that the event was a one-off, strengthening your position to negotiate a more favorable premium.

When Is It Time to Bring in the Lawyers?

Bringing in legal counsel should be a strategic decision, not a reactive one. For any complex or high-value claim—particularly those involving director liability, major business interruption, or significant legal exposure—engaging counsel early is prudent.

An experienced lawyer will ensure your rights are protected, all communications are strategically sound, and every policy condition is met. Waiting until a claim is denied places you at a significant disadvantage. The goal is not to be adversarial; it's to have an expert advisor from the outset to navigate complexities and secure the optimal outcome.

At DialNexa, we know that clear communication is everything when you're navigating complex business challenges. Our advanced Voice AI agents can help your teams standardise their outreach and automate routine calls, ensuring every interaction is professional and consistent. This frees up your top people to focus on the high-stakes negotiations that really matter. See how we turn conversations into conversions at https://dialnexa.com.

[…] liability decisions, fraud review, and reserve quality. For teams assessing process boundaries, the settlement of claims in insurance process is a useful reference because each stage carries a different control […]