The Strategic Meaning of Compliance in Banking: A C-Suite Guide

When we discuss compliance in banking, we are moving beyond a mere set of rules. We're addressing the entire legal and ethical framework—a complex web of laws, regulations, and internal policies—that a financial institution must navigate to operate and thrive. For any senior executive, this isn't a box-ticking exercise; it's fundamental to institutional stability, shareholder value, and sidestepping truly staggering financial and reputational penalties.

What Does Banking Compliance Actually Mean for Your Bottom Line?

For a Director or CXO, understanding banking compliance isn’t about memorising legal jargon. It’s about architecting a foundation for trust that underpins sustainable, profitable growth.

Consider compliance not as a rulebook holding you back, but as the advanced navigation and threat detection system on a multi-billion dollar supertanker. It doesn't just keep you on the legally required route; it actively steers you away from hidden dangers—like sanctions violations or data breaches—that could sink the entire enterprise.

A robust compliance culture is the very bedrock of shareholder value and customer loyalty. When proactively managed, compliance ceases to be a cost centre and becomes a quantifiable competitive advantage. For example, a 2022 Deloitte report found that for every dollar invested in compliance, financial institutions saw an average return of $3 in avoided losses and improved efficiency. In India’s dynamic regulatory climate, a proactive, tech-driven approach is non-negotiable for market leadership.

The Real-World Cost of Non-Compliance

Let's be clear: ignoring these rules has immediate and severe consequences. The penalties aren’t a remote possibility; they are a frequent reality for institutions that fail to maintain vigilance.

Just this past June, the Reserve Bank of India (RBI) imposed penalties totalling INR 53.95 lakh on various banks and NBFCs for failing to adhere to critical regulations. These fines are a stark reminder of the RBI's zero-tolerance stance on KYC (Know Your Customer) and AML (Anti-Money Laundering) directives. For a CXO, this isn't just a fine; it's a public statement about the institution's operational integrity.

Compliance is the strategic guardrail that separates sustainable growth from catastrophic failure. For leaders, it's not about the cost of adherence but the immense, often unrecoverable, cost of neglect.

Beyond Penalties: Strategic Business Risks

The fallout from a compliance breach extends far beyond the initial fine. It can trigger a cascade of devastating business challenges that directly impact your P&L and threaten your institution's long-term viability. For an executive, the mandate is to foresee these connections before a crisis materializes.

Here are the key risks to factor into your strategic planning:

- Reputational Damage: News of a compliance failure spreads instantly in the digital age. A 2023 survey by PwC revealed that 87% of CEOs believe a damaged reputation is the single biggest threat to revenue. A breach can shatter customer trust overnight, potentially triggering a deposit run and leaving you with a tarnished brand that requires years and millions in marketing spend to repair.

- Operational Disruption: A regulatory investigation can bring core business operations to a grinding halt. It diverts senior management's focus from strategic growth to crisis management, placing every decision under intense scrutiny and paralysing day-to-day activities. A major US bank estimated that post-scandal remediation efforts consumed over 1.5 million employee hours in a single year.

- Technological Vulnerability: A surprising number of compliance failures are rooted in legacy technology. To understand how this exposes your organisation, review our guide on the risks of outdated software.

Ultimately, a forward-thinking compliance strategy is simply good governance. It’s about protecting the bank, its customers, and its shareholders, creating a resilient enterprise capable of thriving in a demanding financial landscape.

The Five Pillars of a Modern Compliance Framework

A resilient compliance strategy rests on several key pillars. For any leader in banking, understanding compliance isn't just about checking boxes; it's about a strategic appreciation of how each domain impacts business risk and opportunity. Let's examine the five critical areas every modern financial institution must master.

Think of it like building a skyscraper. A deep foundation of trust, reinforced by solid compliance, is what supports the entire structure, allowing for both stability and vertical growth.

This underscores the strategic reality that compliance isn’t a cost centre. It's the core enabler of the institutional reputation required to fuel sustainable growth and market leadership.

Pillar 1: Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT)

View AML and CFT protocols as the financial industry's critical role in global security. These regulations mandate that banks must actively detect, investigate, and report suspicious activities indicative of criminal proceeds or terrorist funding.

For leadership, this is a zero-tolerance domain. A failure here doesn't just lead to fines; it can make your bank an unwitting node in transnational criminal networks. The IMF has repeatedly warned that weak AML/CFT controls can destabilise national economies and lead to a bank being de-risked by international correspondent banks.

A stark example is the case of a global bank fined nearly $2 billion for allowing drug cartels to launder hundreds of millions of dollars. The reputational damage was catastrophic, and the subsequent internal remediation and monitoring costs exceeded an additional $1 billion, demonstrating the devastating financial impact of weak controls.

Pillar 2: Know Your Customer (KYC) and Customer Due Dligence (CDD)

Know Your Customer (KYC) and Customer Due Diligence (CDD) are the foundational processes for verifying client identity and assessing associated risks. This extends far beyond collecting an Aadhaar card; it involves developing a comprehensive risk profile to ensure your services are not being exploited for illicit purposes.

From a business perspective, efficient KYC is a competitive advantage. A seamless, digital-first process can reduce customer onboarding time by over 80%, creating an excellent first impression and building trust. Conversely, weak KYC exposes the bank to fraud and intense regulatory scrutiny under laws like India’s Prevention of Money Laundering Act (PMLA).

Consider the European bank that was hit with a €775 million penalty for severe CDD lapses. The institution failed to properly vet thousands of high-risk clients over several years, enabling significant money laundering. The fallout included the massive fine, a complete overhaul of its executive board, and a multi-year ban on acquiring new businesses in certain segments.

Pillar 3: Data Privacy and Security

In the digital economy, data is as valuable as capital. This pillar governs how banks collect, process, store, and—most critically—protect customer information. Regulations like India's Digital Personal Data Protection Act (DPDPA) impose stringent rules, with severe penalties for non-compliance.

For the C-suite, a data breach is a top-tier crisis. It can destroy customer trust in an instant, trigger class-action lawsuits, and result in staggering fines. A 2023 IBM report calculated the average cost of a data breach in the financial sector at $5.9 million. Investing in robust cybersecurity and data governance is not an IT expense; it is a fundamental investment in brand equity and business continuity.

A single data breach can cost a company millions, but the loss of customer trust can be permanent. Protecting data is synonymous with protecting the brand.

Pillar 4: Consumer Protection and Fair Practices

This pillar ensures that banks treat their customers fairly, transparently, and ethically. It encompasses everything from fair lending and transparent product disclosures to ethical debt collection practices. Regulators like the RBI are increasingly focused on this area to eliminate predatory behaviour and prevent the mis-selling of financial products.

A demonstrated commitment to fair practices directly enhances brand reputation and cultivates long-term customer loyalty, which can increase customer lifetime value by as much as 300%. Conversely, practices like aggressive sales tactics or hidden fees can lead to swift public backlash and forceful regulatory intervention.

One of the most notorious examples involved a US bank fined $185 million for secretly creating millions of fraudulent customer accounts. The scandal forced the CEO's resignation, led to a 40% drop in new account openings, and inflicted years of damage on the bank's public image.

Pillar 5: Prudential Regulations

Finally, prudential regulations focus on the financial health and stability of the bank itself. These are the rules governing capital adequacy, liquidity management, risk concentration, and stress testing to ensure the institution can withstand severe economic shocks without collapsing.

For executives and board members, this is about foundational solvency. Adherence to prudential norms, such as the Basel III framework, is non-negotiable for maintaining investor confidence and ensuring long-term institutional viability. A failure here could contribute to systemic risk, making it a paramount concern for regulators globally.

Key Banking Compliance Pillars and Their Business Impact

The table below summarises these core compliance areas in the Indian context, highlighting the strategic risks and opportunities they present. It's a quick reference for understanding not just what you need to do, but why it matters to the business.

| Compliance Pillar | Primary Objective | Key Regulations (India) | Business Impact of Failure |

|---|---|---|---|

| AML/CFT | Prevent financial crime and terrorism financing. | Prevention of Money Laundering Act (PMLA), RBI Master Directions | Massive fines, reputational ruin, loss of banking licenses, criminal liability. |

| KYC/CDD | Verify customer identity and assess risk. | RBI Master Direction on KYC, PMLA Rules | Onboarding friction, fraud losses, regulatory penalties, enabling illicit activities. |

| Data Privacy | Protect sensitive customer financial data. | Digital Personal Data Protection Act (DPDPA), IT Act | Data breaches, loss of customer trust, significant fines, class-action lawsuits. |

| Consumer Protection | Ensure fair and transparent treatment of customers. | RBI Fair Practices Code, Consumer Protection Act | Public backlash, customer churn, regulatory intervention, brand damage. |

| Prudential Rules | Maintain the bank’s financial stability and solvency. | RBI regulations based on Basel III norms | Systemic risk, loss of investor confidence, regulatory takeover, bank failure. |

Ultimately, mastering these five pillars is not just about avoiding penalties. It is about building a resilient, trustworthy institution that customers and markets can rely on, which is the only real path to long-term success.

Navigating India's Key Regulatory Landscape

To truly grasp the strategic meaning of compliance in banking, one must understand the architects of the rules. In India, the regulatory environment is a dynamic system shaped by powerful institutions tasked with ensuring economic stability and consumer protection. For any CXO, understanding these regulators and their strategic priorities is essential for proactive leadership, not reactive crisis management.

Think of it as a financial ecosystem. Each regulator governs its domain, but they all converge on a common goal: a strong, transparent, and trustworthy financial system. A strategic understanding of their mandates reveals the "why" behind every new directive and policy shift.

The Apex Regulators Shaping Indian Banking

At the pinnacle of India’s financial oversight are two primary bodies. Their mandates directly shape your bank's operational models, risk appetite, and long-term growth strategy. While their purviews differ, their influence frequently intersects, creating a comprehensive supervisory framework.

-

The Reserve Bank of India (RBI): The RBI is the central bank and the ultimate banking authority. Its role extends far beyond monetary policy. It is the primary supervisor for all banks and non-banking financial companies (NBFCs), setting binding regulations for everything from capital adequacy (a minimum Capital to Risk-Weighted Assets Ratio of 9%) to KYC norms. An RBI directive is not a suggestion; it is a mandate that can compel immediate changes to operational processes.

-

The Securities and Exchange Board of India (SEBI): While the RBI oversees banking, SEBI regulates the securities and capital markets. If your institution engages in investment banking, asset management, or deals in publicly traded securities, you operate under SEBI's jurisdiction. Its regulations are designed to protect investors, prevent market manipulation, and ensure fair practices.

Landmark Legislation and Its Strategic Impact

Compliance is driven not just by regulators, but by the foundational laws they enforce. These acts are more than dense legal texts—they are the frameworks that define the boundaries of your business operations, carrying significant implications for both risk and reputation.

These laws are the 'why' behind the daily compliance grind. They connect your bank's operations directly to national priorities like economic stability and investor protection, making compliance a strategic imperative.

For any senior executive in the BFSI sector, a working knowledge of this legislation is non-negotiable.

The Prevention of Money Laundering Act (PMLA), 2002

The PMLA is the cornerstone of India’s framework to combat money laundering and terror financing. This legislation empowers agencies like the Financial Intelligence Unit (FIU-IND) to track, investigate, and prosecute suspicious financial flows.

For your bank, this mandates robust AML transaction monitoring and reporting systems. Failure is not an option and can lead to crippling penalties, including asset seizure and imprisonment for key executives. The cost of a PMLA violation is existential. A recent report revealed that global financial institutions were fined over $5 billion for AML failures in a single year, a stark reminder of the financial stakes.

The Digital Personal Data Protection Act (DPDPA), 2023

The DPDPA is India’s comprehensive data privacy law, analogous to Europe's GDPR. It establishes strict, non-negotiable rules for how businesses must obtain consent, process, and secure the personal data of Indian citizens. For banks, which are custodians of vast amounts of sensitive financial data, this act represents a paradigm shift.

Strategically, the DPDPA mandates a complete overhaul of data governance. It requires explicit customer consent, purpose limitation for data usage, and mandatory breach notifications. The penalties for non-compliance are severe, with fines up to ₹250 crore per instance. However, the greater cost is the erosion of trust. In banking, trust is the ultimate currency, and a major data breach could destroy it instantly. Investing in compliant data architecture is no longer just good practice; it’s a critical defense for your brand and balance sheet.

Turning Compliance from a Cost Centre into a Competitive Edge

For too long, leadership teams have viewed compliance as a pure cost centre—a defensive necessity to avoid fines. This mindset is not just outdated; it's a profound strategic miscalculation. A modern C-suite perspective on compliance in banking reframes it as a powerful growth engine and a key differentiator in a competitive market.

A world-class compliance framework is no longer just about defense. It's about building an unshakeable foundation of trust that attracts high-value corporate clients, who now frequently include compliance posture in their due diligence, and reassures retail customers. When your institution is known for its integrity, you become the preferred partner in a crowded marketplace.

Building Trust Through Operational Excellence

Robust compliance processes do more than satisfy regulators; they drive tangible improvements in operational efficiency. By standardising procedures to meet regulatory requirements, banks inherently reduce error rates, minimise rework, and enhance overall efficiency. This creates a smoother, more reliable experience for both customers and employees.

Consider the customer onboarding process. A well-designed, compliant KYC protocol not only mitigates risk but also leverages technology to streamline verification. This can reduce customer onboarding cycles from weeks to hours, accelerating time-to-revenue and improving customer satisfaction scores by over 15% in some cases.

Investing in your compliance infrastructure isn't merely about avoiding penalties; it's about building a resilient, reputable brand positioned for long-term market dominance.

Unlocking New Markets and Opportunities

In a globalised economy, a strong compliance posture is a prerequisite for international expansion. Foreign financial institutions will only establish correspondent banking relationships with partners who can demonstrate adherence to global standards like AML and CFT. Without this, access to cross-border payments and trade finance is severely restricted.

India's recent experience provides a powerful case study. The country's concerted compliance push in its banking and payments sector has been a key factor in propelling inward remittances to a record $135.46 billion in a recent fiscal year—the highest in the world. This surge demonstrates how regulatory discipline directly builds international trust, making cross-border payments more efficient and fuelling economic growth. You can find more insights on this trend in a report on India's payment growth from IBSi.

This success proves that rigorous compliance isn't a barrier to growth. It is a catalyst for building the international credibility required to become a major player on the world stage.

The Strategic Advantages of Proactive Compliance

Shifting from a reactive to a proactive compliance culture delivers tangible benefits that align directly with C-suite objectives. A proactive approach involves anticipating regulatory trends, embedding compliance into product design (Compliance-by-Design), and leveraging it as a tool for strategic advantage.

The rewards of this strategic shift are clear and measurable:

- Enhanced Brand Reputation: A clean compliance record becomes a powerful marketing asset, signalling stability and trustworthiness to the market.

- Greater Investor Confidence: Shareholders reward institutions that manage risk effectively. Studies show that companies with strong governance, including compliance, often trade at a premium.

- Attraction of Premium Clients: High-net-worth individuals and large corporations actively seek banking partners with a reputation for airtight security and ethical conduct.

- Improved Decision-Making: The structured data captured for compliance offers invaluable insights into customer behaviour and market trends, informing more precise business strategy.

Ultimately, the message for executives is clear. Pouring resources into your compliance framework is not an expense. It is a strategic investment in building a resilient, reputable brand that can outmanoeuvre competitors and win in the market for years to come.

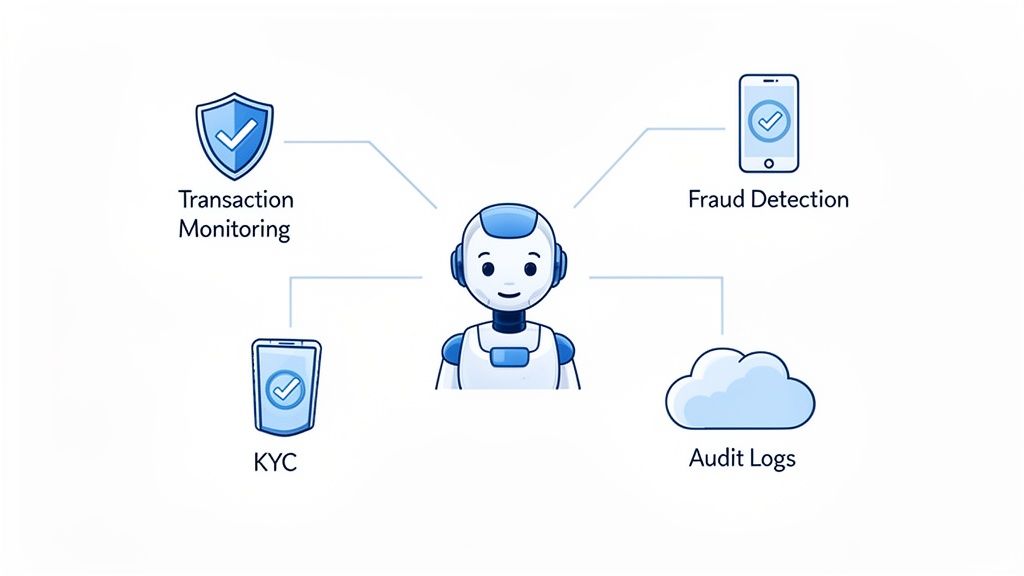

Using Technology to Achieve Compliance at Scale

A compliance strategy is only as effective as its execution. For banking leaders, technology is fundamentally reshaping the compliance meaning in banking. Manual, reactive processes are no longer viable. Instead, tools like Artificial Intelligence (AI) and automation are transforming compliance from a costly obligation into a smart, streamlined function that scales with the business.

This is not about replacing human expertise, but augmenting it. Technology empowers compliance teams to focus their strategic analysis on high-level risks, while intelligent systems manage high-volume, data-intensive tasks with a speed and accuracy that is humanly impossible. It is the optimal synergy: human oversight guiding machine efficiency.

High-Impact Use Cases for Compliance Technology

The application of technology to banking compliance is delivering measurable results today. The field of Regulatory Technology, or RegTech, is pioneering solutions that address the industry's most significant challenges.

Here are three areas where technology is delivering a significant ROI:

-

Real-Time Transaction Monitoring: Legacy systems often flag suspicious activity days late. Modern RegTech platforms use AI to analyse transactions in real-time, detecting complex money laundering patterns (like "smurfing" or layering) that rule-based systems miss. For instance, one leading bank reduced its investigation time per alert from 45 minutes to under 5 minutes using an AI-powered system.

-

Advanced Fraud Detection: AI algorithms analyse thousands of data points per transaction—geolocation, device ID, transaction history, and behavioural biometrics—to identify fraud with unparalleled precision. This reduces false positive alerts by up to 70%, allowing fraud teams to concentrate on genuine threats and improving the customer experience by avoiding unnecessary transaction blocks.

-

Predictive Risk Modelling: Instead of merely reacting to past events, advanced analytics can now forecast future compliance risks. By analysing historical data, market trends, and regulatory changes, these models can identify emerging financial crime typologies or predict the impact of new regulations, providing leadership with the foresight to act preemptively.

Engineering Customer-Facing Tools for Compliance

Perhaps the most powerful application of this technology is at the customer interface. Every interaction is a potential compliance event, and tools like Voice AI are proving to be genuine game-changers. An AI agent is more than a customer service bot; it is a meticulously engineered compliance tool.

For example, an AI agent handling KYC verification calls can deliver the regulator-approved script with 100% fidelity, every single time. It never deviates, never forgets a mandatory disclosure, and never misses a critical verification question. This level of consistency is impossible for human teams to maintain at scale.

Technology transforms compliance from a checklist of rules into an embedded, automated, and auditable function within every single business process. This is not just risk mitigation; it is operational excellence.

This consistency creates an ironclad defense during regulatory audits. Every call is recorded, transcribed, and logged, creating a flawless and instantly searchable audit trail. If a regulator questions whether a specific disclosure was made, you can produce definitive, time-stamped proof in seconds. This capability drastically reduces the time and cost associated with audits and regulatory inquiries.

The Tangible Business Gains of Compliant Technology

The benefits of embedding compliance into your technology extend far beyond risk management; they drive significant operational efficiencies and improve the bottom line. By automating routine outreach and verification with Voice AI, banks can achieve unprecedented scale and effectiveness.

A major challenge in customer outreach is contactability. Traditional call centres often struggle with connection rates around a dismal 47%. In contrast, intelligent Voice AI systems—which can optimize call timing and personalize greetings—have been shown to increase customer connection rates to an astonishing 91%.

This is more than an efficiency gain; it's a fundamental enhancement of business capability. You can verify more customers, resolve more issues, and follow up on more leads with the same resources. This blend of human-like interaction and AI-driven compliance is explored in our deep dive into revolutionising banking with a hybrid AI and human customer service model. The data is clear: technology designed for compliance also drives superior business results, turning a regulatory burden into a powerful competitive advantage.

A Practical Compliance Checklist for Executive Leadership

For senior leadership, understanding the meaning of compliance in banking is one thing; assessing your organisation’s resilience is another. This is not a checklist for your compliance officers. It is a strategic tool for the C-suite and board to pressure-test your compliance framework from a governance perspective.

Use these questions to initiate critical conversations and identify potential blind spots before they evolve into material liabilities. An objective self-assessment is the first step toward building a truly robust compliance program.

Strategic Ownership and Accountability

A genuine compliance culture is driven from the top. If leadership treats it as a peripheral function, the entire organization will follow suit. The key is to embed compliance accountability directly into executive responsibilities and incentive structures.

-

Is Compliance Ownership Crystal Clear at the Board Level? Is there a dedicated board committee or a designated director with explicit oversight for compliance? Critically, do they possess the authority and independence to challenge business decisions on regulatory grounds?

-

Are Compliance KPIs Baked into Executive Performance Reviews? Beyond revenue targets, are senior leaders evaluated on their business unit's compliance record, audit outcomes, and risk management effectiveness? A recent survey found that only 34% of firms link executive compensation directly to compliance metrics—a significant gap in accountability.

Technology and Training Investments

Attempting to manage modern compliance with manual processes is an invitation for failure. Technology is your most powerful ally for scaling efforts, but it is only as effective as the people who use it.

-

Are We Investing Enough in Technology to Automate Monitoring? Have you allocated sufficient capital to RegTech and AI tools for automated transaction monitoring and the creation of immutable audit trails? Effective systems drastically reduce human error, which is a factor in over 80% of data breaches. For a baseline on robust systems, review our complete guide to audit logging.

-

Is Our Compliance Training Actually Engaging and Relevant? Have you moved beyond generic annual training modules? High-risk teams—such as trade finance, wealth management, and correspondent banking—require dynamic, scenario-based training that addresses the specific risks they face.

Proactive Crisis Readiness

The true measure of a compliance program is not its performance on a normal day, but its resilience in a crisis. A post-breach response plan is not a strategy; it's a reactive scramble.

- Have We War-Gamed Our Response to a Major Breach? Have you conducted a full-scale simulation of a major compliance failure, such as a systemic data breach or a significant AML violation? You must stress-test your crisis communications strategy, legal response protocols, and operational continuity plans to identify weaknesses before a real event occurs.

Frequently Asked Questions

Here are straightforward answers to the strategic questions that frequently arise in boardrooms and executive leadership meetings.

What's the Single Biggest Compliance Threat for Indian Banks Right Now?

The primary threat is not a single regulation, but the dangerous intersection of sophisticated cybercrime, data privacy failures, and weaknesses in Anti-Money Laundering (AML) controls. This creates a multi-front compliance crisis.

For example, a cybercriminal doesn't just steal customer data. They use that stolen data to open mule accounts and launder illicit funds. This single event triggers a regulatory nightmare. The bank now faces penalties under the Digital Personal Data Protection Act (DPDPA) for the data breach, and simultaneously, penalties under the Prevention of Money-laundering Act (PMLA) for the subsequent financial crime. The cumulative damage involves massive fines from multiple regulators and a catastrophic loss of customer trust.

How Can We Actually Measure the ROI on Our Compliance Tech?

Looking solely at "fines avoided" provides a very narrow view. To truly measure the ROI of compliance technology, directors should focus on three key areas of value creation.

- Smarter Operations (Cost Savings): Calculate the direct reduction in operational expenditure. If an AI system reduces false positive AML alerts by 70%, you can quantify the saved person-hours. For example, if it saves 20,000 hours of analyst time per year at an average loaded cost of ₹1,500/hour, that's a direct saving of ₹3 crore. More importantly, your top analysts are reallocated to high-value, complex investigations.

- Faster Revenue (Growth Enablement): Measure the acceleration of revenue generation. If automated KYC processes reduce corporate client onboarding from 30 days to 3 days, you begin earning revenue 27 days sooner. This "time-to-revenue" metric is a direct, quantifiable impact on top-line growth.

- Better Business Insights (Strategic Value): Don't overlook the strategic value of the data generated by your compliance systems. This structured, high-quality data provides a clearer view of customer behaviour, risk concentrations, and market opportunities. These insights can inform product development, pricing strategies, and market entry decisions, creating value far beyond the compliance function.

The real ROI of compliance isn't just about avoiding costs; it's about connecting your technology spend to faster growth, smarter risk management, and a data-driven strategy. It reframes compliance from a necessary evil into a genuine competitive edge.

Is AI Changing the Chief Compliance Officer's Job?

Absolutely. Artificial Intelligence is transforming the Chief Compliance Officer (CCO) from a reactive policy enforcer into a proactive, data-driven strategist who is central to the bank's strategic direction.

Previously, the CCO's role was dominated by interpreting dense regulations and managing post-event remediation. Today, with AI providing predictive risk analytics, a CCO can identify potential threats—such as an emerging fraud pattern or a high-risk client segment—before they escalate. By presenting these data-driven insights to the board, a modern CCO can guide proactive risk mitigation strategies, assess the compliance viability of new products, and shape the bank's long-term growth plans. Compliance is no longer a department that says "no"; it's a strategic advisor that enables the business to grow safely and sustainably.

At DialNexa, we understand that robust, tech-enabled compliance is the bedrock of a modern financial institution. Our human-like Voice AI agents are engineered to provide perfectly consistent KYC support, create impeccable audit trails, and ensure every customer interaction meets the highest regulatory standards. We help transform your compliance obligations into a strategic advantage.

Discover how our technology can safeguard your institution and enhance your operational efficiency by visiting https://dialnexa.com.

Leave a Reply