AI Banking Assistant Guide: Boost CX & Cut Costs for CXOs

The most important number in conversational banking isn't a chatbot containment metric. It's the scale of capital moving into the category. The global artificial intelligence in banking market is projected to rise from USD 31.29 billion in 2025 to USD 396.6 billion by 2034, at a 32.6% CAGR, according to Straits Research's artificial intelligence in banking market analysis. For a banking CXO, that reframes the discussion immediately. This isn't a peripheral service tool. It's a control point for cost, service, and competitive position.

Boards often treat the AI banking assistant as a digital channel upgrade. That's too narrow. In practice, it sits at the intersection of customer experience, front-office productivity, compliance execution, and revenue orchestration. The institution that deploys it well doesn't just answer queries faster. It redesigns how account servicing, onboarding, repayments, support, and guided sales happen at scale.

That matters beyond BFSI as well. EdTech lenders, property finance businesses, wealth platforms, trading firms, and any enterprise with regulated customer conversations are facing the same pressure: deliver immediate support without increasing service complexity. An AI banking assistant is becoming the operating layer for that shift.

Table of Contents

- The Trillion-Dollar Shift to Conversational Banking

- Defining the Modern AI Banking Assistant

- The Strategic ROI Quantifying the P&L Impact

- A CXOs Implementation Roadmap

- Navigating Compliance and Integration Challenges

- AI in Action Success Metrics from Indian Banking Leaders

- Securing Your Edge in the Future of Finance

The Trillion-Dollar Shift to Conversational Banking

Banks are no longer debating whether conversational AI matters. The investment case was established earlier. The board-level question now is narrower and more consequential: which use cases change unit economics, control risk, and improve customer lifetime value within the next planning cycle.

That framing matters because conversational banking is not a channel project. It is an operating model decision. Institutions that deploy AI into high-volume service journeys can reduce avoidable contact-center demand, improve response consistency, and capture interaction data that manual teams rarely structure well enough to use. For leadership teams comparing priorities, the primary benchmark is not chatbot novelty. It is whether the bank can lower cost-to-serve while improving compliance discipline and conversion across digital touchpoints.

The first deployments usually produce the clearest returns in repeatable journeys with clear process rules: service requests, onboarding guidance, collections reminders, dispute intake, employee help desks, and product eligibility screening. Banks evaluating the shift from scripted bots should understand the difference between chatbots in banking and more capable AI assistants. The technology choice affects more than customer experience. It determines whether the bank is buying a lighter self-service layer or building an asset that can support revenue, service, and control functions at scale.

Why this changes competitive logic

A capable AI banking assistant increases service capacity without requiring routine support headcount to rise in parallel with customer volume. It also standardises explanations across app, web, messaging, and voice interactions, which reduces variability in regulated communications and creates cleaner audit trails. Those outcomes affect margins and supervision quality at the same time.

There is also a less obvious strategic effect. Once conversational workflows are connected to core systems, the bank gains a reusable interface for execution, not just assistance. The same architecture can handle loan-status updates, KYC document follow-up, payment reminders, card controls, and internal policy queries. That is why the market is shifting from standalone bots to broader AI customer service agents that can act on systems, not only answer questions.

The competitive implication is straightforward. Banks that reach production maturity early set customer expectations for response speed, availability, and precision. Banks that delay inherit a more expensive path. They must modernise under pressure, after service standards have already been reset by faster competitors.

Why CXOs should act before the market forces it

Late adoption creates two balance-sheet problems. Manual servicing stays expensive, and the bank loses time to build the controls, integrations, and governance needed for safe automation. Those capabilities cannot be added overnight once the market expects instant support.

There is also a revenue consequence. In retail banking, lending, wealth, and adjacent financial services, response quality now influences conversion and retention alongside pricing. A customer who gets immediate, accurate guidance is more likely to complete onboarding, submit missing documents, and stay inside the bank's ecosystem for the next product.

For a CXO, the strategic priority is clear. Treat the AI banking assistant as enterprise infrastructure with measurable P&L impact, not as a digital feature owned only by the contact centre or app team. The institutions that move first are not just improving service. They are building a lower-cost, more controllable, and more extensible front line for the next phase of banking competition.

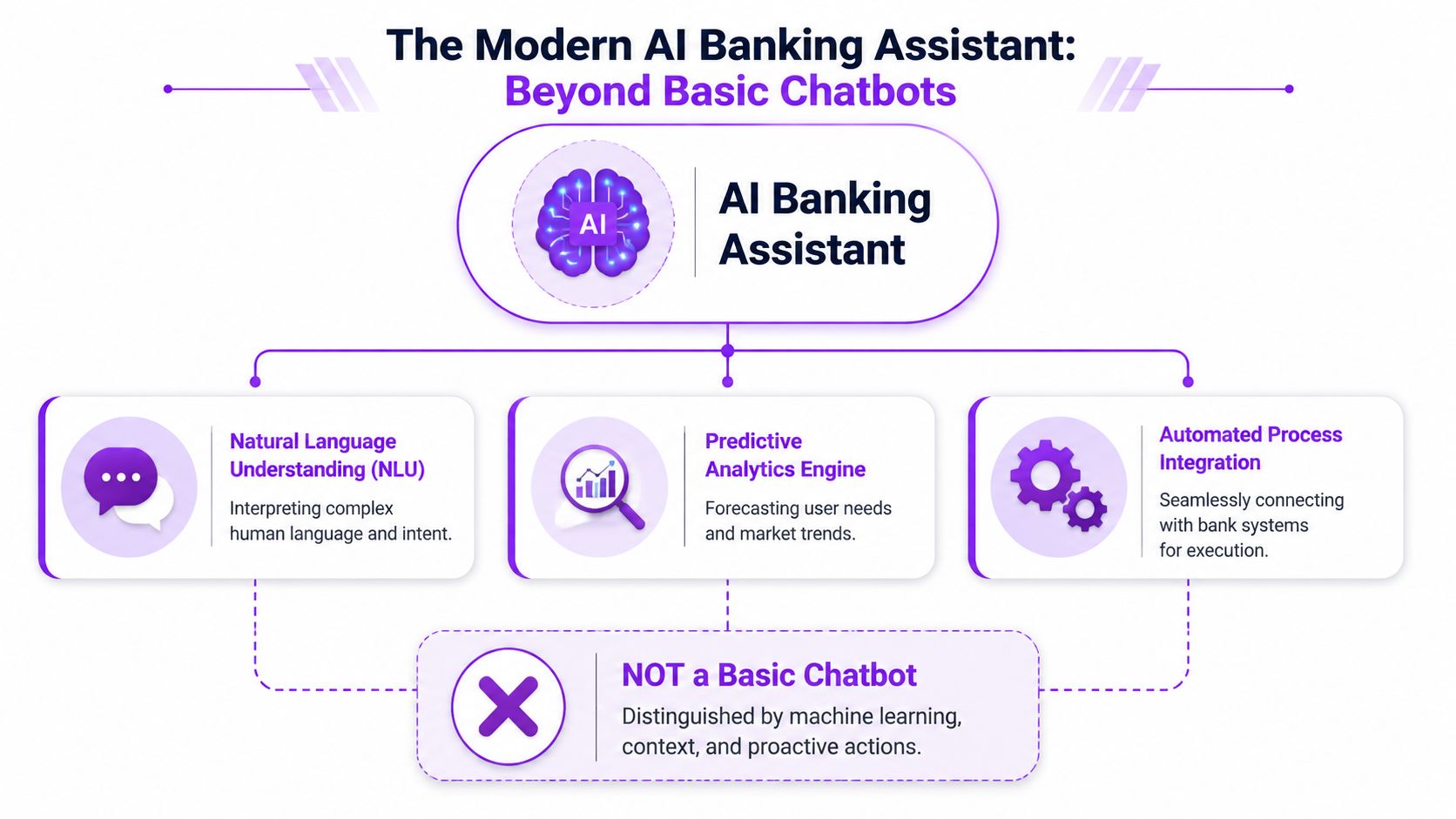

Defining the Modern AI Banking Assistant

The easiest way to misunderstand an AI banking assistant is to think of it as a smarter FAQ bot. A modern assistant is something different. It interprets user intent, pulls regulated data with consent, performs domain-specific financial analysis, and responds in language the customer can act on.

What separates an assistant from a chatbot

In India, advanced AI banking assistants are defined by three connected capabilities: data ingestion through RBI-regulated channels, financial analysis using borrower logic such as FOIR and CIBIL scoring, and context-aware multilingual responses. That same architecture can deliver up to 93% language detection accuracy, according to GoCredit's explanation of AI personal finance assistants.

That definition matters because most customer-facing bots still operate on scripts. They detect keywords, route to articles, and fail when context shifts. A true AI banking assistant can process real statements and reports with user consent, compute affordability or obligations, and translate the result into next actions.

For a CXO, this is the practical distinction:

- Basic chatbot: Good for static questions such as branch timings or card-blocking instructions.

- AI banking assistant: Useful for workflows such as pre-qualification guidance, account servicing, KYC support, EMI understanding, and transaction-linked customer help.

If you want a broader view of how conversational systems mature from support bots into operational service layers, Prometheus Agency's guide to AI customer service agents is a useful companion read. For a banking-specific perspective on use cases and deployment patterns, this overview of chatbots in banking adds relevant context.

The business capabilities that matter to leadership

The value of an AI banking assistant is easiest to see when mapped to business outcomes rather than model features.

| Capability | What it does in practice | Why leadership should care |

|---|---|---|

| Secure data ingestion | Pulls data from regulated channels with customer consent | Reduces manual verification friction |

| Financial logic execution | Applies FOIR, EMI, and scoring logic consistently | Improves decision support and standardisation |

| Multilingual conversation | Handles English, Hindi, or mixed-language interactions | Expands usable access across demographics |

| Action-oriented responses | Converts analysis into next best actions | Lifts completion rates in customer journeys |

| System integration | Connects to banking workflows and records outcomes | Enables execution, not just conversation |

A practical example makes this real. In lending, a customer asks whether a new obligation is affordable. A rules-based bot can only share generic education. An AI banking assistant can, with consent and system access, analyse obligations, estimate affordability, and tell the customer what document or action comes next.

Practical rule: If the system cannot ingest real financial context, apply banking logic, and return an auditable response, it isn't yet a strategic AI banking assistant.

That's the standard leaders should apply in procurement conversations.

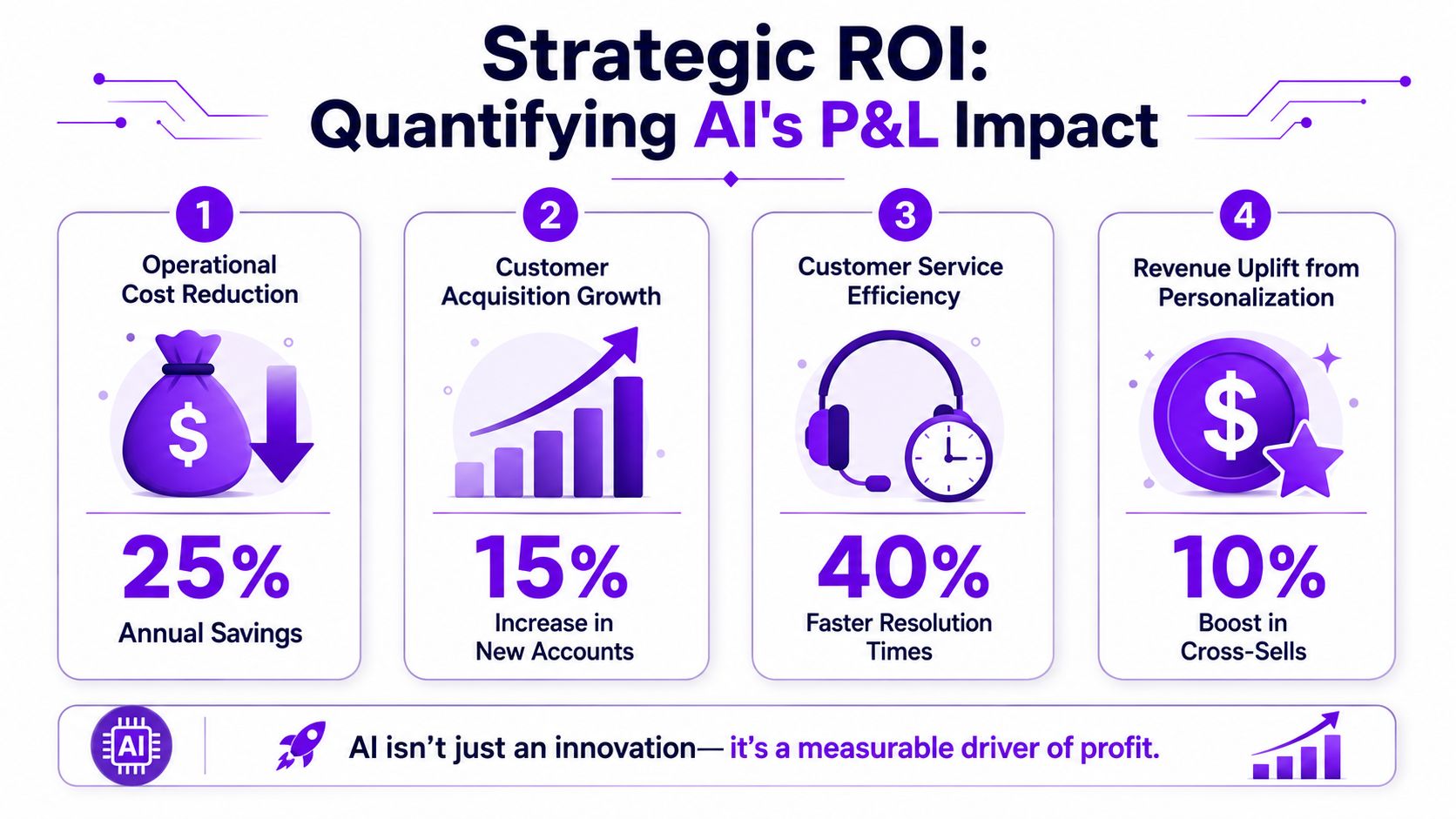

The Strategic ROI Quantifying the P&L Impact

A banking AI programme starts to matter at board level when it changes operating profit, not when it adds another digital touchpoint. The aggregate potential cost savings from AI applications in banking are estimated at $447 billion, with $416 billion tied to front and middle office operations, according to the AIQRATE Global AI Adoption Report for BFSI. That concentration matters because AI banking assistants sit directly inside those cost centres: service, fulfilment, collections support, onboarding, and employee operations.

Where the Savings Originate

The strongest business case is operating model redesign. Call deflection is only one component, and often not the largest one.

The larger savings pool usually comes from removing avoidable work across the service chain. An assistant that resolves routine requests at first contact reduces repeat interactions, shortens handling time for escalated cases, and improves adherence to standard operating procedures. In regulated environments, that consistency has financial value because it lowers rework, reduces exception volumes, and limits the manual checks created by incomplete or inconsistent customer interactions.

For a CXO, four cost levers matter most:

- Routine service automation: High-frequency queries such as balance checks, onboarding status, payment reminders, and document guidance can shift from human queues to AI-led handling.

- Response-time compression: Faster resolution reduces abandonment, lowers queue volatility, and improves staff productivity because agents receive fewer partially handled cases.

- Process standardisation: Consistent prompts, disclosures, and next-step guidance reduce downstream correction work across operations and compliance teams.

- Extended service coverage: 24/7 support improves utilisation of digital channels without requiring equivalent growth in staffed operations.

Document-heavy workflows create another source of value that is often missed in chatbot business cases. If a bank wants an assistant to support lending, disputes, onboarding, or servicing, it must also improve how financial records are read and structured. The operational link is direct: better document ingestion increases straight-through processing and reduces analyst review time. A useful reference is this guide on AI analysis of financial documents, which shows why document intelligence often improves the economics of conversational banking more than interface design alone.

Why the ROI Case Extends Beyond Cost Takeout

AIQRATE also reports that over 80% of financial firms in India use AI to some extent. At that level of adoption, AI is no longer a differentiation story by itself. The strategic question becomes where the bank applies it to produce superior economics.

That shifts the ROI discussion from a narrow service metric to a P&L framework with three components:

- Efficiency improvement through lower manual servicing demand and lower rework.

- Revenue support through faster journey completion, better lead follow-up, and fewer drop-offs in sales and servicing flows.

- Risk control through standardised disclosures, auditable interactions, and tighter policy execution.

This is why the highest-return deployments usually sit where repetitive demand, compliance sensitivity, and commercial value intersect. A bank that applies an AI assistant to balance enquiries alone may save cost. A bank that applies it across onboarding, payment support, collections communication, internal agent assistance, and document-led workflows can improve margin, service quality, and control at the same time.

The strongest returns come from using AI banking assistants in workflows where labour intensity, regulatory exposure, and conversion opportunity overlap. That is where cost reduction becomes a durable competitive advantage, not a one-time efficiency project.

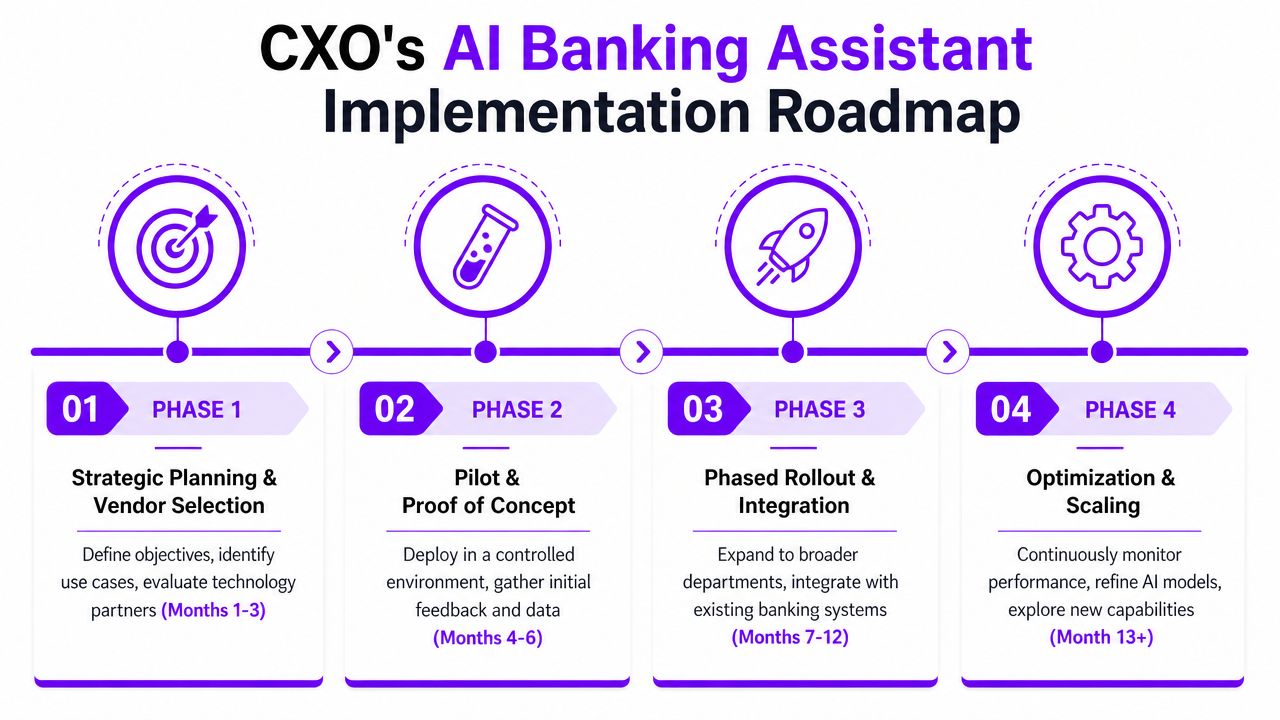

A CXOs Implementation Roadmap

An AI banking assistant fails most often when leaders try to deploy it as a giant transformation programme. It succeeds when they treat it as a staged operating redesign with tight control points.

Phase one starts smaller than most boards expect

Start with a high-volume, bounded workflow. Internal IT support is often a strong first use case because it offers measurable volume, lower regulatory risk, and clear escalation paths. In customer operations, narrow use cases work best first: onboarding status checks, KYC document guidance, loan application status, or payment reminder support.

The goal of phase one isn't channel transformation. It's proving four things:

- Accuracy under real demand: Can the assistant answer consistently?

- Escalation control: Does it know when to hand over?

- System connectivity: Can it pull the right data and log actions cleanly?

- Governance fit: Are compliance, legal, and operations comfortable with the control model?

A useful planning reference for cross-functional teams is Cyber Command's article on developing an AI roadmap for businesses. It's relevant because most banking failures start as alignment failures, not model failures.

Scale only after the control model works

Once the pilot proves reliable, scale through adjacent journeys rather than through mass rollout. That usually means expanding across channels and complexity in this order:

- Single workflow to multi-workflow

- Text interactions to voice and app support

- Informational support to transaction-linked execution

- Customer-facing use cases to employee-facing assistance

This sequence matters. A bank that jumps directly into advisory or exception-heavy journeys without testing control logic first creates unnecessary model risk and organisational friction.

Start with use cases where the institution already knows the right answer path. That makes auditing, tuning, and stakeholder confidence far easier.

AI Banking Assistant Vendor Evaluation Checklist

A procurement team shouldn't evaluate vendors only on demos. They should assess operational fit, governance maturity, and deployment discipline.

| Evaluation Criterion | Key Questions to Ask | Red Flags to Watch For |

|---|---|---|

| Integration readiness | How does the platform connect to core systems, CRMs, KYC tools, and audit logs? | Vague claims about “easy integration” with no architecture detail |

| Multilingual capability | Can it manage mixed-language queries and domain-specific terminology? | Generic language support with no banking context |

| Compliance controls | How are disclosures, consent, retention, and traceability handled? | No clear answer on audit trails or policy enforcement |

| Escalation design | When does the assistant transfer to a human, and what context follows? | Handoffs that force customers to repeat information |

| Security posture | How is sensitive financial data handled in storage and transit? | Unclear data boundaries or weak governance explanations |

| Analytics and tuning | What review tools show failure patterns, drift, and workflow drop-offs? | No practical reporting for operations and compliance teams |

| Scalability model | What happens when volume spikes or additional channels are added? | Capacity claims without operational evidence |

| Implementation support | Who owns onboarding, training, and workflow design? | Heavy customer dependency for core setup steps |

The strategic insight is simple. The right vendor doesn't merely provide an assistant. They provide a controllable operating layer that the bank can govern, expand, and measure over time.

Navigating Compliance and Integration Challenges

Many vendors present the AI banking assistant as a clean customer experience upgrade. That framing is incomplete. In regulated environments, the harder problem isn't getting an assistant to respond. It's ensuring the response is correct, governable, and defensible.

The largest risk is confident error at scale

A 2024 study highlighted the risk of AI-induced misinformation potentially eroding $17 billion in consumer trust across India's BFSI sector. The same analysis noted that only 12% of the 89 million user interactions for financial guidance are verified by human experts, according to this review of AI chatbot risks in the banking industry. This is a critical warning for leadership. A weak assistant doesn't just frustrate customers. It can industrialise bad guidance.

This is why governance must precede scale. Institutions need clear boundaries between informational support, workflow guidance, and advisory content. They also need confidence thresholds that trigger human review.

A practical control model usually includes:

- Approved knowledge boundaries: Limit responses to governed content and authorised calculations.

- Human escalation rules: Route low-confidence, high-impact, or ambiguous interactions to trained staff.

- Transcript and decision logging: Preserve what was said, what data was used, and what action followed.

- Periodic review: Sample interactions for quality, bias, and policy adherence.

For leaders working through the broader operating implications, this CXO-focused guide to mastering compliance in the banking industry is a useful companion.

Integration discipline determines trust

The second challenge is integration. An assistant that sits outside core systems can sound polished while still creating downstream risk. It might provide outdated status information, miss policy nuances, or fail to record an interaction properly.

That's why mature deployments connect conversational interfaces to controlled internal systems, not just to public knowledge repositories. The bank should know which source system informed the answer, which workflow accepted the next action, and which record captured the event.

The compliance issue isn't AI itself. It's unmanaged AI attached to high-stakes banking workflows.

The competitive advantage comes from doing the difficult work competitors avoid. A bank that solves integration and governance well can move faster later, because each new use case sits on a trusted foundation rather than on another isolated pilot.

AI in Action Success Metrics from Indian Banking Leaders

Production evidence from Indian banks shows that conversational AI can operate at national scale, not just as a pilot channel. Cutter's analysis of AI banking initiatives in India reports that HDFC's Eva has resolved more than 2.7 million queries from 530,000 unique users since 2017, SBI's SIA handles 10,000 inquiries per second, and ICICI's iPal has interacted with 3.1 million customers, answered 6 million queries, and reached 90% accuracy. The same analysis notes that leading assistants are connected through APIs to banking systems so they can support transactions such as transfers, bill payments, peer-to-peer payments, and loan application submissions.

What scale looks like in production

These cases matter because they point to three distinct sources of economic value.

HDFC's Eva illustrates volume absorption. A bank that shifts millions of routine requests into self-service reduces contact-center load, shortens response times, and preserves human capacity for higher-value interactions. That changes the service cost curve.

SBI's SIA highlights throughput resilience. Handling demand at that level matters less as a technical milestone than as an operating model advantage. A bank can maintain service continuity during peaks without scaling headcount at the same rate.

ICICI's iPal shows why accuracy is the metric that connects customer experience to financial performance. If an assistant can answer millions of queries while holding a defined accuracy threshold, the institution gains a basis for controlled expansion into adjacent journeys such as onboarding support, payment servicing, and product guidance.

A second HDFC data point sharpens the implementation lesson. IFMR GSB's paper on artificial intelligence applications in Indian banking states that EVA processes product and service queries in less than 0.4 seconds with 85% accuracy, while supporting multiple languages including English and Hindi. For CXOs, that combination matters because adoption depends on response speed and language accessibility as much as model quality.

The strategic takeaway is straightforward. Banks are getting returns where assistants are tied to live workflows, measurable service metrics, and multilingual customer demand. Institutions still treating conversational AI as a thin front end will struggle to match those economics.

Leaders comparing channels should also review this perspective on Voice AI adoption in Indian call centers, particularly where the business case depends on shifting high-volume service interactions out of agent queues.

Why these examples matter beyond banking

The broader lesson is operational, not sector-specific. AI assistants perform best in environments with high interaction volume, clear policies, repeatable intents, and a strong need for auditability.

That pattern applies directly to adjacent industries. An EdTech lender can use the model for fee reminders and application guidance. A real estate finance business can use it for pre-qualification support and document follow-up. A trading platform can use it for account servicing, funding guidance, and risk communications.

Production success depends on workflow integration, response quality, and clear commercial targets.

Indian banking leaders have already established the benchmark. The institutions that learn from these examples will treat AI assistants as a P&L instrument, not a channel experiment.

Securing Your Edge in the Future of Finance

The next phase of the AI banking assistant won't be defined by better scripted support. It will be defined by better timing and better judgement. The assistant will move from reactive service to proactive financial engagement, provided the institution has already built the data, governance, and workflow discipline to support that shift.

That evolution changes the competitive map. A bank that already operates a trusted conversational layer can extend it into repayment nudges, contextual product guidance, service recovery, internal agent support, and more precise cross-functional routing. A bank that hasn't built that layer will still be trying to stitch channels together while others are improving decision quality across them.

Many leadership teams underestimate this opportunity. The AI banking assistant isn't only a cost programme and it isn't only a CX programme. It's a reusable execution framework for regulated conversations. Once deployed well, it gives the business a way to scale service, standardise guidance, and capture operational data from every interaction.

For CXOs, the strategic imperative is to treat this as an enterprise capability with clear ownership. The best sponsors are usually cross-functional leaders from operations, digital, risk, and business units, backed by a board-level expectation that the programme must produce measurable commercial outcomes.

Three decisions shape whether the institution leads or follows:

- Choose the first use case carefully: Start where demand is high and workflow boundaries are clear.

- Design governance before expansion: Quality controls and escalation logic should come before broad rollout.

- Build for extensibility: The initial deployment should support later use across voice, mobile, support, and guided sales.

The market is moving fast, but the more useful insight is this: advantage won't come from adopting AI in general. It will come from operationalising the right AI banking assistant in the right parts of the customer and employee journey before peers do.

DialNexa Labs Private Limited helps enterprises deploy human-like Voice AI agents for customer support, qualification, recruitment, and presales across BFSI, EdTech, real estate, software, and other service-heavy sectors. If your team is evaluating how a compliant conversational layer could improve service consistency, reduce routine workload, and scale customer interactions without adding operational drag, explore DialNexa Labs Private Limited to see how custom agents can be launched around your workflows.

Leave a Reply