Your Strategic Guide to Chatbots in Banking for 2026

For banking leaders, the conversation around chatbots has moved on. The question is no longer if they should be adopted, but how fast they can be deployed for maximum strategic advantage. This isn't a far-off concept; it’s an immediate operational reality that’s already separating the market leaders from the laggards.

We’re seeing chatbots in banking evolve from simple query-bots into sophisticated AI agents that directly drive revenue, slash operational costs, and build measurable customer loyalty. For a CXO, this represents a pivotal opportunity to transform a cost center into a profit-generating asset.

The Undeniable Shift to Conversational Banking

The very fabric of how banks engage with their customers is undergoing a radical transformation. The legacy model—characterised by branch visits and long call centre queues—is being decisively replaced by instant, on-demand digital conversations. This isn’t merely about convenience; it’s a board-level priority fuelled by hard data on customer adoption, efficiency gains, and bottom-line impact.

Investing in AI-powered conversations has stopped being a cost-centre discussion. It’s now about securing a critical competitive edge. For CXOs, the real question is, "How do we deploy this technology to capture market share and optimize our P&L?"

The Data Mandating Immediate Action

The modern banking customer, especially from the digitally native Millennial and Gen Z demographics, doesn't just prefer instant service—they expect it as a baseline. They manage their financial lives from their smartphones and have zero tolerance for friction or delays. Every slow interaction is a direct risk to customer retention and lifetime value.

This is where the strategic muscle of a well-architected chatbot becomes clear. They deliver the 24/7 availability and immediate, accurate resolutions that foster loyalty and prevent churn. To get a deeper sense of how AI is rewriting the rules, it's worth exploring expert analysis like this guide on Chatbots in Banking: Revolutionising Customer Service and Operations.

For executives, the most powerful argument is the direct line between chatbot deployment and core business metrics. Well-designed automation can handle up to 80% of routine customer queries, freeing up your expert human agents to focus on complex, high-value work like wealth management, loan advisory, and resolving high-stakes complaints—activities that directly generate revenue.

Suddenly, your support function isn't just a helpline; it's a strategic asset for growth.

Chatbots in Banking At a Glance for 2026

The following table provides a snapshot of key metrics that demonstrate the strategic impact of chatbot adoption, offering a clear business case for banking CXOs.

| Metric | Data Point | Business Implication for CXOs |

|---|---|---|

| Operational Cost Reduction | Up to 30% | Reduces overhead in customer service centres, directly boosting the bottom line. A chatbot interaction costs between $0.50-$0.70, compared to $6-$12 for a human agent. |

| Lead Conversion Uplift | 15-20% | Engages prospects 24/7, pre-qualifies leads, and shortens the sales cycle. For example, Bank of America's 'Erica' has helped drive significant digital sales growth. |

| Customer Satisfaction (CSAT) | Over 90% | High satisfaction from instant, accurate responses builds loyalty and reduces churn by up to 25%. |

| Agent Productivity | +25% | Automates repetitive tasks, allowing human agents to focus on complex, advisory roles that drive revenue and deepen relationships. |

These figures aren't just projections; they represent the tangible returns that leading banks are already achieving, turning their customer service operations into profit centres.

The Numbers Don't Lie

The global adoption data tells a very clear story for any director evaluating market trends. By 2025, India had already become the world's largest market for banking chatbot interactions, managing over 250 million conversations every month. This highlights an incredible digital acceleration within the region's BFSI sector that cannot be ignored.

This boom is part of a broader pattern across the Asia-Pacific region, where banks hit a staggering 79% chatbot adoption rate, leaving other global markets far behind. What’s critically important for leadership is that customers are fully on board with this shift:

- Customer satisfaction with banking chatbots reached an impressive 84%, demonstrating a clear preference for automated efficiency.

- Users consistently praised the 24/7 availability and speed of resolution as key drivers of their positive experience.

- A massive 87% of enquiries were fully resolved in under 60 seconds without needing to be passed to a human agent, a clear indicator of massive efficiency gains.

These aren't just interesting statistics; they are proof of a tested, scalable model for boosting operational efficiency while quantifiably improving the customer experience.

Unlocking ROI with High-Value Chatbot Use Cases

For banking leaders, the true potential of chatbots in banking isn't just about answering, "What's my balance?". While that's a decent start, the use cases that truly move the needle on your P&L are the ones that generate revenue, slash operational costs, and foster genuine customer loyalty. It’s time to shift the conversation from simple cost-cutting to building a strategic profit centre.

These advanced applications are where you'll see a powerful, measurable return on your investment. Think of it as the difference between a simple FAQ bot and a dedicated digital financial specialist working for your bank 24/7.

Automating High-Volume Account Servicing

Every bank gets flooded with routine, yet crucial, customer requests. We're talking about tasks like updating personal details, ordering a new card, checking transaction history, or changing a PIN. Individually they seem small, but in aggregate, they consume a huge amount of agent time and resources in a traditional call centre, representing a significant operational drag.

An intelligent chatbot can take over these processes completely. By integrating securely with your core banking systems via APIs, the bot can authenticate a customer and handle their request from start to finish, with no human hand-off needed.

- Practical Example: A customer misplaces their debit card late on a Friday night. Instead of anxiously waiting for the bank to open on Monday, they open the banking app and tell the chatbot, "I've lost my card." The bot immediately authenticates them via biometrics or a PIN, blocks the old card, confirms the delivery address on file, and dispatches a new one. A stressful, urgent problem is solved in minutes, at virtually no cost.

This level of self-service automation has a direct, positive impact on your operational efficiency. Data shows that automating these high-volume tasks can save over four minutes per inquiry, freeing up your skilled agents to focus on more complex, advisory conversations that build relationships and revenue.

This shift helps your contact centre evolve from a reactive support desk into a proactive relationship-building hub. For more on this, you might be interested in our deep dive into how data and AI will transform contact centres for financial services.

Supercharging Loan Pre-Screening and Lead Qualification

One of the most financially rewarding uses for chatbots in banking is right at the top of the sales funnel—in loan origination and pre-screening. A well-trained AI agent can act as the perfect front-line qualifier, engaging potential borrowers 24/7 and gathering all the essential information before a human loan officer ever steps in.

Imagine someone browsing your mortgage products at 10 PM. A chatbot can pop up and start a conversation: "Hi, interested in a home loan? I can check your eligibility in 90 seconds." It then asks key qualifying questions about their income, loan amount, and property details. In an instant, you've turned a passive website visitor into an actively qualified lead in your CRM.

Key Benefits of AI in Loan Pre-Screening:

- Increased Conversion: Bots are always on, capturing leads that would otherwise be lost after business hours. This 24/7 engagement has been shown to lift lead-to-booking rates from a typical 2% to as high as 8%.

- Enhanced Accuracy: An AI agent can achieve up to 97% accuracy in qualifying leads based on your predefined criteria, ensuring your expert loan officers only spend their valuable time on high-potential applicants.

- Faster Processing: Automating the initial data collection significantly shortens the "time-to-yes," improving the customer's experience and making it less likely they'll shop around with your competitors while waiting.

The result is a highly efficient, data-driven sales pipeline where your human experts can focus their skills on final approvals and building client relationships, not on tedious data entry.

Driving Engagement and Reducing Churn

The tangible return from chatbots is becoming undeniable, especially in competitive markets like India. Recent findings show that Indian banks using chatbots are seeing remarkable results, including up to a 40% increase in user engagement and a 25% reduction in customer churn projected by 2025. These gains come directly from providing instant, helpful service that keeps customers happy and loyal.

This success is also reflected in operations, where 67% of banks now use bots for essential tasks like onboarding, payments, and screening. By successfully automating 90% of these interactions, they are not just making the customer's journey smoother but also achieving major cost reductions. For a CXO, these are not soft metrics; they translate directly into higher customer lifetime value and lower acquisition costs.

These numbers build a powerful business case. They show that a strategic chatbot programme is a direct investment in both customer retention and operational excellence. By focusing on these high-value applications, banking leaders can secure a strong competitive edge and deliver clear, positive returns to the business.

Getting Chatbot Architecture and Integration Right

As a leader, you don’t need to write the code yourself, but understanding the technical blueprint for your chatbot is absolutely critical. The architectural choices you make today will directly shape your bot's intelligence, security, and ability to scale. Make the wrong call, and you're looking at expensive rework, security vulnerabilities, and a failed project.

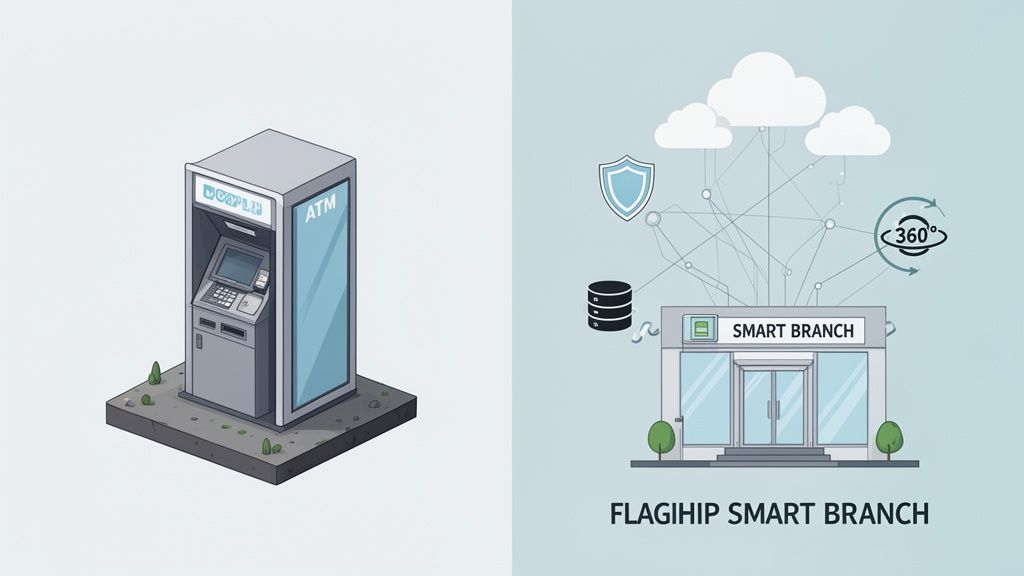

A simple analogy helps frame this for strategic planning. A standalone bot is like a pop-up ATM – handy for a few basic tasks but completely separate from your core operations. A fully integrated bot, on the other hand, is your flagship smart branch. It’s deeply woven into your entire banking ecosystem, ready to deliver sophisticated, personalised services at scale.

The Two Core Architectural Models

Choosing an architecture isn't just an IT decision; it's a strategic one that determines the chatbot's ROI potential. Your choice defines how deeply the chatbot can tap into customer data and your core systems to perform meaningful actions.

Get this wrong, and you'll create frustrating dead-ends for customers and minimal business value. Get it right, and the bot becomes a powerful, indispensable part of your digital service offering.

1. Standalone Architecture (The "Pop-Up ATM")

This model is a self-contained island, completely disconnected from your main banking systems. It’s perfect for answering general questions about things like branch hours, product features, or basic FAQs. It's often faster and cheaper to deploy, but its usefulness and business impact are severely capped.

- What it does: Responds to pre-programmed questions. It has no access to customer-specific data and can't perform any transactions.

- Best for: A limited-scope pilot project or as an information source on a public-facing marketing website.

- The business risk: It can’t handle transactions or provide any real, personalised help. For anything meaningful, the conversation is handed off to a human agent, often leading to a disjointed and frustrating customer experience.

2. Integrated Architecture (The "Smart Branch")

For any serious, ROI-focused deployment of chatbots in banking, this is the only viable path. Here, the chatbot is securely wired into your core banking platform, CRM, and other key systems using APIs (Application Programming Interfaces). This connection is what allows the bot to authenticate users and actually do things on their behalf.

For any executive focused on results, the integrated model is where the true ROI is found. It turns the bot from a simple FAQ directory into a transactional powerhouse that can resolve up to 80% of common customer queries end-to-end, from blocking a lost card to initiating a payment, without any human intervention.

This architecture is the bedrock for creating a 360-degree customer view, enabling the kind of smart, efficient service that modern customers demand.

APIs: The Unsung Heroes of Integration

Think of APIs as the secure, digital couriers that allow your chatbot to communicate with your bank's existing infrastructure. Without them, your chatbot is isolated and ultimately, not very useful from a business perspective. A robust API strategy is what allows a chatbot to perform valuable actions like checking a real-time balance, executing a fund transfer, or updating a customer's contact details in your CRM.

When you're assessing vendors, their API capabilities should be a top-tier consideration. A provider with a well-documented, secure, and flexible API-first platform will dramatically reduce integration timelines and costs. This is also how you future-proof your investment, making it easier to add new features and capabilities as your business needs evolve.

This is especially true as you look toward the next frontier of customer interaction. For instance, incorporating advanced features like voice AI is almost entirely dependent on this strong architectural base. You can explore more on the strategic value of voice AI in banking to see where the industry is headed.

Ultimately, a deeply integrated approach doesn't just make customers happier; it also strengthens security and compliance. By funnelling all communication through secure, encrypted API calls, you minimise vulnerabilities and ensure you're adhering to strict financial regulations.

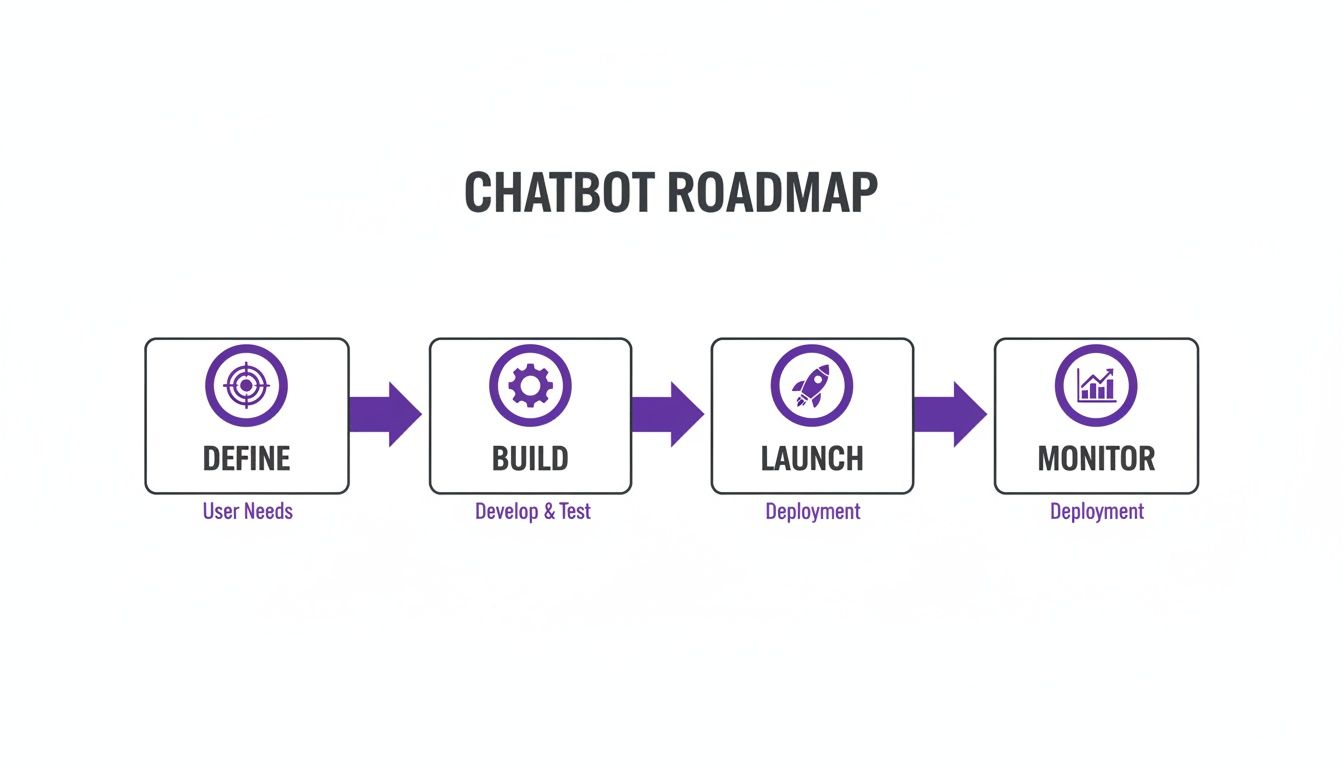

Your Roadmap for a Successful Chatbot Rollout

Bringing a chatbot into your bank isn't just an IT project. It’s a major business transformation that demands strong executive leadership and a clear, step-by-step plan. A successful launch is all about connecting the technology to tangible business results from day one. This roadmap is designed to help leaders steer their teams, ask the right strategic questions, and ensure the investment pays off.

Getting from an idea to a fully operational AI agent involves more than just good programming. You need a structured approach to manage stakeholder expectations, mitigate risks, and achieve organisational buy-in. By following these phases, you can keep your chatbot project on track, within budget, and aligned with your most critical business goals.

Phase 1: Define Your Goals and Success Metrics

Before you even think about vendors or code, the first job for leadership is to define what success actually looks like for your bank. Vague ambitions like “improving the customer experience” are not actionable. You need specific, measurable targets that link directly to your bank's Key Performance Indicators (KPIs).

For instance, a solid, executive-level goal sounds like this: "Reduce call volumes for 'password reset' and 'transaction history' queries by 70% within six months, leading to an estimated operational cost saving of ₹X million." This gives your teams a clear finish line and a justifiable business case.

Key Questions for Your Leadership Team:

- Which specific, high-volume, simple customer queries are consuming the most agent time and budget right now?

- What is our current cost-per-interaction for these queries, and what is our target CPI post-automation?

- How will we measure customer satisfaction (CSAT) with the chatbot, and what is the target score needed to protect and enhance brand perception?

Phase 2: Select the Right Vendor Partner

Picking your technology provider is one of the most critical decisions you'll make. This isn't just a software procurement; you are selecting a strategic partner who must genuinely understand the banking domain. A vendor with proven experience in the BFSI sector will already be aligned with your requirements for security, data privacy, and regulatory compliance.

Look for partners who offer a robust, API-first architecture. This is non-negotiable for integrating the chatbot into your core banking systems, CRM, and other platforms. Without these deep integrations, your chatbot will be little more than a fancy FAQ page, unable to deliver the transactional value that drives real ROI.

A classic mistake is selecting a vendor based solely on the lowest price. This often results in a low-quality, standalone bot that frustrates customers and ultimately fails, with 63% of such interactions leading to no resolution at all. The real value comes from a system that can successfully handle at least 60-80% of conversations without human intervention.

Phase 3: Prepare Your Data and Launch a Pilot

An AI is only as intelligent as the data it’s trained on. Before going live, your team needs to collate a clean, well-organised dataset of past customer conversations (anonymized, of course). This data is what teaches the chatbot's Natural Language Processing (NLP) models to understand the specific intent and vocabulary your customers use.

Once the initial training is done, it's time for a careful, phased rollout, starting with a small pilot program to prove the concept and business case.

Actionable Pilot Program Steps:

- Start Small: Kick things off with one, well-defined use case, like handling requests for account balances or recent transactions.

- Internal Launch: First, roll out the chatbot to a controlled group of employees to gather feedback in a safe, internal environment.

- Beta Test: Next, offer it to a select group of tech-savvy customers who have opted-in to test new features.

- Analyse and Iterate: Closely monitor performance metrics, collect user feedback, and continuously refine the chatbot's responses before a full public launch.

Phase 4: Monitor Performance and Navigate Regulations

A chatbot is not a "set and forget" technology. Constant monitoring and data-driven optimization are crucial for its long-term success and ROI. Your team should be tracking KPIs like resolution rate, agent handover rate, and CSAT scores in real-time. This data provides the insights needed to identify areas for improvement and strategically expand the chatbot's capabilities.

Beyond the technology, rigorous regulatory compliance is paramount. Financial institutions must ensure their AI tools comply with all consumer protection laws. For example, the CFPB's issue spotlight addresses concerns about bank use of AI chatbots and offers valuable guidance on compliance. This ensures your chatbot is not only effective but also responsible, secure, and legally sound.

When you invest in new technology, the board is going to ask one simple question: what’s the return? For chatbots in banking, the answer isn't just about trimming costs. It's about generating real, measurable value that impacts the entire business. As a leader, you need to focus on the Key Performance Indicators (KPIs) that tie chatbot performance directly to the bank's bottom line.

A well-executed chatbot initiative delivers clear wins in three key areas: operational efficiency, customer experience, and business growth. By tracking the right metrics, you can build a solid business case that justifies the investment and paves the way for future AI projects.

Gauging Operational Efficiency

The most immediate and tangible returns from a chatbot come from making your operations leaner and more effective. These metrics provide a clear view of how well your bot is deflecting routine queries from human agents, directly impacting your operational costs.

Cost Per Interaction (CPI): This is the gold standard for measuring efficiency. Compare the cost of a human-handled interaction (agent salary, benefits, overhead) with the cost of an automated one. A chatbot conversation is a fraction of the price, with leading banks reporting savings between $0.50 to $0.70 per interaction.

Agent Handover Rate: This KPI tracks how often the chatbot needs to escalate a conversation to a human. A high rate is a red flag, indicating poor training or a scope mismatch. A well-tuned chatbot should independently resolve 60% to 80% of the conversations it's designed to handle.

Quantifying the Customer Experience

A superior customer experience is the bedrock of loyalty and retention. While it may seem "softer" than cost savings, these metrics are essential for understanding your customers' perception of your brand.

We’ve all dealt with a frustrating, low-quality chatbot. It’s no surprise that older, clunkier systems can have customer satisfaction rates as low as 29%. But modern conversational AI, which truly understands customer intent, can completely reverse that by providing fast, accurate resolutions.

Here are the key experience metrics to watch:

- Customer Satisfaction (CSAT): After each chat, a simple rating request provides direct, actionable feedback for continuous improvement.

- First Contact Resolution (FCR): Did the chatbot solve the problem on the first try? A high FCR means happier customers and reduced repeat contact volume.

- Average Resolution Time: How quickly does the bot solve an issue? Today’s AI can deliver answers up to 65% faster than older systems. In those "micro-moments" of urgent customer need, speed is a critical differentiator.

This entire process, from defining goals to tracking performance, is a continuous loop. You don't just launch a chatbot and walk away; you constantly monitor and refine it.

As you can see, monitoring KPIs isn't the end of the road. It’s a vital part of a cycle that feeds directly back into making your chatbot smarter and more effective over time.

Connecting Chatbots to Business Growth

Ultimately, the most strategic chatbots do more than just answer questions—they actively contribute to top-line growth. By tracking the right growth-oriented KPIs, you can demonstrate how the bot is not just a cost centre, but a revenue-generating asset. You can also get a much deeper understanding of your customers by learning how speech analytics can help steer chatbot interactions.

- Lead Conversion Rate: If you’re using your chatbot for loan pre-screening or new account opening, track how many conversations convert into qualified leads or completed applications. A 24/7 bot can significantly lift conversion rates by engaging prospects at their moment of interest.

- Customer Churn Reduction: Happy customers are loyal customers. By correlating your CSAT and FCR scores with customer retention data, you can draw a straight line between excellent chatbot service and reduced churn. In fact, some banks have seen churn drop by as much as 25% after implementing an effective AI agent.

By focusing on these concrete, data-backed KPIs, you shift the internal conversation from "How much does it cost?" to "How much value are we creating?" This is how you prove the strategic worth of your chatbot initiative and secure its role as a key pillar of your digital transformation strategy.

The Future of Banking Is Conversational

The chatbots in banking we see today are merely the first chapter. For a forward-thinking leader, the long-term vision must extend beyond current use cases to what's next. This isn’t science fiction; it's the competitive landscape that will separate the market leaders from the laggards in the coming years.

The future of customer-bank interaction will be fluid, proactive, and deeply integrated into daily life. For banks, this means shifting from a reactive problem-solving model to proactively anticipating customer needs before they even arise. The endgame is a true conversational ecosystem that makes your bank an indispensable financial partner.

The Rise of Voice AI and Hands-Free Banking

The next major evolution is the shift from screen-based text to voice. Voice AI is poised to become a dominant channel for banking, driven by its sheer convenience. Customers will manage their finances while driving, cooking, or multitasking, all without touching their phone.

- Practical Example: A customer says, "Ask my bank to transfer ₹5,000 to my sister for our parents' anniversary." A sophisticated voice agent would handle the entire request securely, using biometric voice authentication to confirm their identity and then process the transfer, providing an audio confirmation. This kind of seamless, hands-free experience is the new benchmark for customer convenience.

Hyper-Personalisation with Predictive Analytics

In the near future, banking chatbots will evolve from support agents to proactive personal financial advisors. By leveraging predictive analytics, these AI systems will analyze a customer’s spending habits, income, and life events to offer timely, valuable advice.

This isn't just a clever way to cross-sell products. It's about building deep trust by providing tangible value. For example, the AI might notice a customer's savings have dipped for two consecutive months and proactively offer a personalized budget plan. Or, it could identify an opportunity for them to earn a better return by moving funds into a high-yield account, initiating the process with a simple "yes."

This level of hyper-personalisation, which 72% of banking customers state directly impacts their choice of bank, transforms the relationship from transactional to advisory.

The Development of Emotionally Intelligent Bots

One of the final frontiers for AI is understanding and responding to human emotion. The next generation of chatbots in banking will incorporate emotional intelligence, enabling them to navigate sensitive conversations with empathy and care.

Imagine a customer reporting a stolen card, audibly stressed. The bot will detect the distressed tone of their voice or the urgent language in their text. It will immediately switch to a calming, reassuring script, rapidly securing the account while providing clear, empathetic guidance. This ability to manage emotionally charged situations will be crucial for building and preserving customer trust, especially during moments of high stress.

Answering the Tough Questions for Banking Leaders

When considering a major technology investment, the critical questions always surface in the boardroom. Let's tackle the most common concerns banking leaders have about deploying AI chatbots, providing straight answers grounded in real-world data and experience.

What’s the Real-World Cost of a Banking Chatbot?

The investment can vary significantly. A simple FAQ bot might have a low entry cost, but a truly strategic, integrated AI chatbot that connects to your core banking systems will typically require an initial investment ranging from ₹40,00,000 to over ₹2,00,00,000.

However, the initial spend is only half the equation. The metric that matters to any CXO is the return on investment (ROI). Leading banks consistently achieve cost savings of ₹40 to ₹60 for every single interaction the chatbot handles. When scaled across high volumes, a well-deployed system can achieve payback in months, not years.

How Can We Be Sure Our Data Stays Secure and Compliant?

In banking, security is non-negotiable. Any vendor under consideration must demonstrate rock-solid security protocols as a core competency. This includes end-to-end encryption, PII data masking, and full, auditable compliance with regulations like GDPR and India's Digital Personal Data Protection Act.

The chatbot's architecture must function as a secure gatekeeper. It should authenticate a user, wrap their request in layers of encryption, and pass it to your core systems without ever storing sensitive data on its own servers. It is imperative to partner with a vendor who has a proven track record in the BFSI sector and to conduct comprehensive security and compliance audits before signing any contract.

Will These Bots Make Our Human Agents Redundant?

Absolutely not. The strategic goal is to augment your human agents, making them more valuable, not to replace them. The operational reality is that chatbots are perfectly suited for handling the high-volume, repetitive queries that clog phone lines—tasks that constitute nearly 90% of routine service requests.

This automation frees up your experienced staff to focus on complex, high-value conversations that require empathy, judgment, and sophisticated problem-solving—like financial advice, mortgage consultations, and fraud resolution. Your contact centre transforms from a cost centre into a relationship-building and revenue-generating hub.

This strategic shift consistently boosts both employee morale and customer satisfaction. Your best people are deployed on more engaging, impactful work, and customers still receive expert human support when it matters most.

How Soon Will We See a Return on Our Investment?

While every deployment is unique, targeting a positive ROI within 12 to 18 months is a realistic and achievable goal for a full-scale project. The initial returns materialize almost immediately from call deflection away from more expensive human-staffed channels.

A prudent approach is to begin with a pilot programme focused on one or two high-volume, low-complexity use cases. This can demonstrate a tangible ROI in as little as six months, providing a powerful, data-backed business case to secure stakeholder buy-in for a broader, enterprise-wide deployment.

Ready to see how these conversations can translate into measurable business growth? DialNexa develops human-like Voice AI agents that scale up your presales, support, and lead qualification without scaling your headcount. Find out how our platform can deliver up to a 91% connect rate and qualify your leads with 97% accuracy.

Learn more and start building your custom agent at DialNexa.

[…] screening. Banks evaluating the shift from scripted bots should understand the difference between chatbots in banking and more capable AI assistants. The technology choice affects more than customer experience. It determines whether the bank is […]