IVR Services in Bank: A CXO’s Guide to AI-Powered CX

Indian banks no longer have the luxury of treating IVR as a low-priority telephony layer. By 2022, IVR handled 25% of India’s 1.2 billion annual banking calls and cut operational costs by 30% for BFSI firms, according to the FICCI-KPMG figures cited here. That single fact should reframe the boardroom conversation. IVR services in bank operations are no longer about “Press 1 for balance enquiry”. They’re about cost structure, compliance, rural reach, and how fast your bank can respond under pressure.

The banks winning in India are redesigning voice as an intelligent service layer. They’re tying IVR into UPI flows, Aadhaar-linked processes, CRM-led personalisation, and multilingual support. Banks that keep running rigid menu trees will continue pushing customers to agents, increasing operating cost, and losing trust at the exact moment support quality has become a competitive differentiator.

Table of Contents

- The Hidden Cost of Your Current IVR System

- From Touch-Tones to Conversations The IVR Evolution

- Quantifying the ROI of Modern IVR Services

- Advanced IVR Use Cases Transforming Indian Banking

- IVR Architecture and Core Banking Integration

- Ensuring Security and Compliance in Voice Banking

- Your Roadmap to IVR Modernisation in 2026

- Frequently Asked Questions about IVR in Banking

- How long does it take to move from a legacy IVR to a conversational AI platform

- Can modern IVR work with older on-premise core banking systems

- Is AI-IVR the same thing as a voice bot

- Which banking journeys should be automated first

- Will customers still need access to human agents

- What should the executive committee track after go-live

The Hidden Cost of Your Current IVR System

Most bank leaders underestimate how much damage a poor IVR creates. They see it as a customer irritation. It’s worse than that. It’s an operating model failure that pushes low-value demand into expensive human channels.

India exposes this weakness sharply. A critical gap remains for India’s 190 million unbanked adults, where traditional IVR fails because low literacy and language barriers break the interaction flow, as noted in this analysis of IVR gaps in Indian banking. The same source states that 55% rural drop-offs are tied to poor multilingual support, while modern Voice AI reaches 91% connect rates versus 47% for traditional IVR.

Legacy IVR creates three board-level problems

First, it inflates service cost. When customers can’t complete a simple task in self-service, they press for an agent. Your bank then pays agent-level cost for routine work such as card blocks, balance queries, PIN resets, EMI dates, and status checks.

Second, it hurts CX at scale. Frustration in banking voice support doesn’t stay inside the contact centre. It affects app ratings, branch complaints, retention, and service trust. If your executive team reviews only average call volumes and misses the deeper relationship between failed automation and dissatisfaction, you’re managing the wrong dashboard. A stronger way to think about this is through customer sentiment metrics such as CSAT and DSAT in service operations.

Third, it limits market expansion. If your voice channel can’t support multiple Indian languages smoothly, your acquisition and service economics outside metro markets remain weak.

Practical rule: If your IVR mainly serves as a gatekeeper to agents, it isn’t automation. It’s queue management.

The real issue isn’t IVR itself

Banks shouldn’t conclude that IVR has failed. Old IVR has failed. The difference matters.

Touch-tone menus were built for predictable tasks and narrow pathways. Indian banking now requires contextual support across savings, lending, payments, fraud alerts, KYC, and service requests. Customers don’t think in menu trees. They speak in intent. “My UPI transaction failed.” “I need my loan statement.” “Block my card now.” “Why was my EMI bounced?”

That’s why conversational AI-powered IVR has moved from optional upgrade to strategic necessity. It doesn’t just route calls. It interprets intent, authenticates quickly, completes routine journeys, and escalates only when value or complexity justifies human intervention. Executives should treat that shift as a competitive reset.

From Touch-Tones to Conversations The IVR Evolution

By the late 2000s, IVR was already standard infrastructure in Indian banking. Banks adopted it for one reason. Scale. Customer growth was outrunning branch capacity, and the call centre could not absorb every balance enquiry, card block request, or cheque book request without driving up service cost.

The first generation of IVR solved that operational problem well enough. It was built for fixed journeys and repeatable prompts. Press a number, hear a menu, complete a simple task, or get routed to an agent. That model matched the banking environment of the time, when voice demand was narrower and product complexity was lower.

Its limit was obvious. Menu trees break the moment the customer asks a real question.

That gap became more expensive as Indian banking shifted to always-on payments, instant account servicing, and mass digital adoption across metro, semi-urban, and rural markets. UPI disputes, Aadhaar-linked verification issues, failed auto-debits, and multilingual service requests do not fit neatly into DTMF logic. A caller saying, “My UPI payment failed but the money is debited,” expects resolution, not a maze of options.

The second phase of IVR evolution was integration. Leading banks stopped treating IVR as a standalone telephony tool and started connecting it to CRM, core banking, payments systems, fraud controls, UPI workflows, and Aadhaar-based identity processes. That shift changed the role of voice. IVR stopped being a front-end filter and became part of the transaction and service layer.

For Indian banks, this is the strategic dividing line. Global IVR articles usually focus on generic call routing and self-service. That is not enough here. In India, the voice channel has to work across multiple languages, low digital comfort segments, regulatory scrutiny, and payment ecosystems that move in real time. If your IVR cannot verify identity safely, surface account context instantly, and support UPI and Aadhaar-linked journeys, it is already behind the market.

Now the market is entering the third phase. Conversation.

A modern AI-IVR does not ask customers to translate their problem into a menu path. It identifies intent from natural speech, pulls relevant customer context, authenticates with policy controls, and completes the task or routes the interaction with full context attached. That is how a bank cuts repeat calls, improves first-contact resolution, and protects agent capacity for revenue and exception handling.

Language support decides whether this works at national scale. India is not a one-language voice market, and executives should stop buying IVR platforms as if it were. The winning systems are trained for code-switching, accent variation, and intent recognition across tier-1, tier-2, and rural usage patterns. RBI compliance also raises the bar. Banks need clear consent flows, auditability, and reliable escalation paths, not flashy demos.

Voice quality plays a bigger role than many committees assume. Customers judge trust in seconds, especially during fraud alerts, payment failures, or KYC-related interactions. Banks evaluating conversational systems should assess realistic text-to-speech voices carefully because poor speech synthesis reduces comprehension and confidence, particularly in multilingual service journeys.

The practical conclusion is simple. Legacy IVR automated menus. AI-IVR automates intent-led banking journeys, tied directly to UPI, Aadhaar, compliance controls, and core systems. In the Indian market, that is now a competitive requirement, not a channel upgrade.

Quantifying the ROI of Modern IVR Services

A 45% reduction in average handling time should end the debate. A 2023 BCG India report, cited in this analysis of IVR performance metrics, found that BFSI IVR deployments reduced average handling time from 420 seconds to 231 seconds per call, while raising call containment to 58% nationally. That is not a service improvement story. It is a margin story.

Indian banks should evaluate IVR the same way they evaluate any large technology programme. Start with cost-to-serve, agent productivity, abandonment, first-contact resolution, and customer retention. Then test whether the platform can support India-specific journeys such as UPI dispute status, Aadhaar-linked verification steps, and multilingual self-service without pushing callers back to an agent.

The financial case gets stronger at scale. The same report cites public sector banks deflecting 35 million calls per month and generating ₹1,200 crore in annual savings. It also notes that NLP-led upgrades reduced abandonment from 18% to 7%. For any bank with a large retail base, those numbers point to a direct operating benefit. They also point to lower queue pressure during peak events such as tax periods, EMI spikes, fraud waves, and payment outages.

What ROI looks like in banking operations

Reduced handling time lowers staffing pressure in the contact centre. Higher containment shifts routine demand out of assisted channels. Lower abandonment protects service quality during peaks. Better personalisation improves completion rates for self-service journeys that customers would otherwise drop.

The same source reports CSAT of 78 out of 100 for upgraded IVR in private banks, compared with 62 out of 100 for legacy systems. It also reports that CRM-led personalisation increased self-service adoption by 28% in Hindi-belt states. That matters in India because voice performance is not judged only on speed. It is judged on whether the bank can recognise intent accurately across mixed-language speech patterns and complete the task in one call.

Legacy IVR vs AI-Powered IVR

| Metric | Legacy Touch-Tone IVR | Conversational AI-IVR |

|---|---|---|

| Average handling time | 420 seconds per call before optimisation in the cited BFSI benchmark | 231 seconds per call in the same benchmark |

| Call containment | Lower, because menu trees push many callers to agents | 58% nationally in the same report |

| Monthly deflection in public banks | Limited | 35 million calls per month in the same report |

| Annual savings | Weak economics when routine calls still require agent support | ₹1,200 crore in annual savings in the same report |

| Abandonment | 18% before NLP-led improvement | 7% after NLP-led improvement in the same report |

| CSAT | 62 out of 100 for legacy systems | 78 out of 100 after AI upgrades in the same report |

A board-level review should force precision. If the business case does not show how many balance enquiries, card blocks, UPI status checks, EMI reminders, KYC follow-ups, and fraud confirmation calls will move to automation, the model is incomplete. If the vendor cannot map savings by language, queue, geography, and call type, the committee should reject the proposal.

Four ROI questions that matter

- How much avoidable agent demand exists today? Measure the volume of repetitive calls that should be contained in self-service, especially balance checks, card controls, dispute status, and branch or product information.

- What is each failed automation attempt costing the bank? Repeat calls increase telecom cost, agent workload, and compliance exposure because authentication and disclosures must be repeated.

- Where can voice personalisation raise completion rates? Customer context from CRM, UPI systems, and service history should shorten the path to resolution.

- What high-value work can agents take back once volume drops? Collections, wealth servicing, business banking support, and exception handling produce better returns than answering routine status queries.

Banks that want a clearer benchmark for automation economics should review how an AI call bot for banking self-service and support changes containment, routing accuracy, and cost per resolved interaction.

The recommendation is simple. Approve IVR modernisation only if the business case is tied to measurable gains in AHT, containment, abandonment, CSAT, and redeployed agent capacity. In the Indian market, where UPI volumes are high, language variation is wide, and RBI scrutiny is real, AI-IVR should be treated as core service infrastructure. Not as a telephony upgrade.

Advanced IVR Use Cases Transforming Indian Banking

The strongest argument for AI-IVR isn’t theory. It’s the breadth of banking journeys it can now handle without creating dead ends for customers.

The foundation still matters

Banks should start with high-frequency, low-risk interactions. Balance enquiries, mini-statements, card hotlisting, cheque book requests, branch hours, EMI due-date reminders, and transaction status calls remain ideal self-service journeys. These are not glamorous use cases, but they create immediate operational relief when executed well.

The mistake is stopping there. Modern ivr services in bank operations can now support journeys that directly affect onboarding, security, and product conversion.

Four use cases with real strategic value

Voice-led KYC and verification

When IVR connects to Aadhaar-linked workflows and customer records, the bank can guide callers through structured verification in a familiar voice channel. That matters in markets where app completion is inconsistent or digital literacy is uneven. The interaction becomes more inclusive, especially when offered in regional languages.

Fraud intervention and proactive risk calls

Conversational IVR can contact a customer when suspicious behaviour appears, confirm whether a transaction is genuine, and trigger the next step. That’s faster than waiting for inbound complaint volume to spike. It also creates a consistent response path during fraud events.

Smart routing for customer value tiers

A salaried retail customer, a mass affluent customer, and a high-value corporate treasury user should not enter the same queue architecture. AI-IVR can identify customer type early and route accordingly, reducing friction for premium segments without abandoning service efficiency.

Assisted lending and collections journeys

Voice can pre-qualify borrowers, confirm document status, explain EMI obligations, and nudge payment completion. If the system understands natural responses instead of forcing keypad input, completion improves and agent intervention becomes more targeted.

A useful way to think about this broader shift is through the rise of the AI call bot in customer operations, where voice automation stops being a narrow support tool and becomes an execution layer across service and revenue workflows.

What agentic AI changes

Some banks are already seeing meaningful impact from conversational IVR powered by agentic AI. According to this analysis of agentic AI and conversational IVR in banking, banks report a 30 to 40% reduction in call centre volume when the system autonomously handles tasks such as account transfers, credit card approvals, and fraud detection without human escalation.

That matters because it expands the role of IVR from triage to transaction completion.

A quick visual overview helps frame the shift in customer experience:

What executives should prioritise first

- High-volume service journeys: Card block, account balance, transaction status, and statement requests should be automated first.

- Risk-sensitive moments: Fraud alerts and unusual activity confirmation deliver customer trust quickly.

- Onboarding support: KYC guidance and verification flows reduce drop-offs in complex customer journeys.

- Collections and reminders: Voice is effective where immediacy and acknowledgement matter.

The strongest AI-IVR programmes don’t try to replace the contact centre. They remove waste from it.

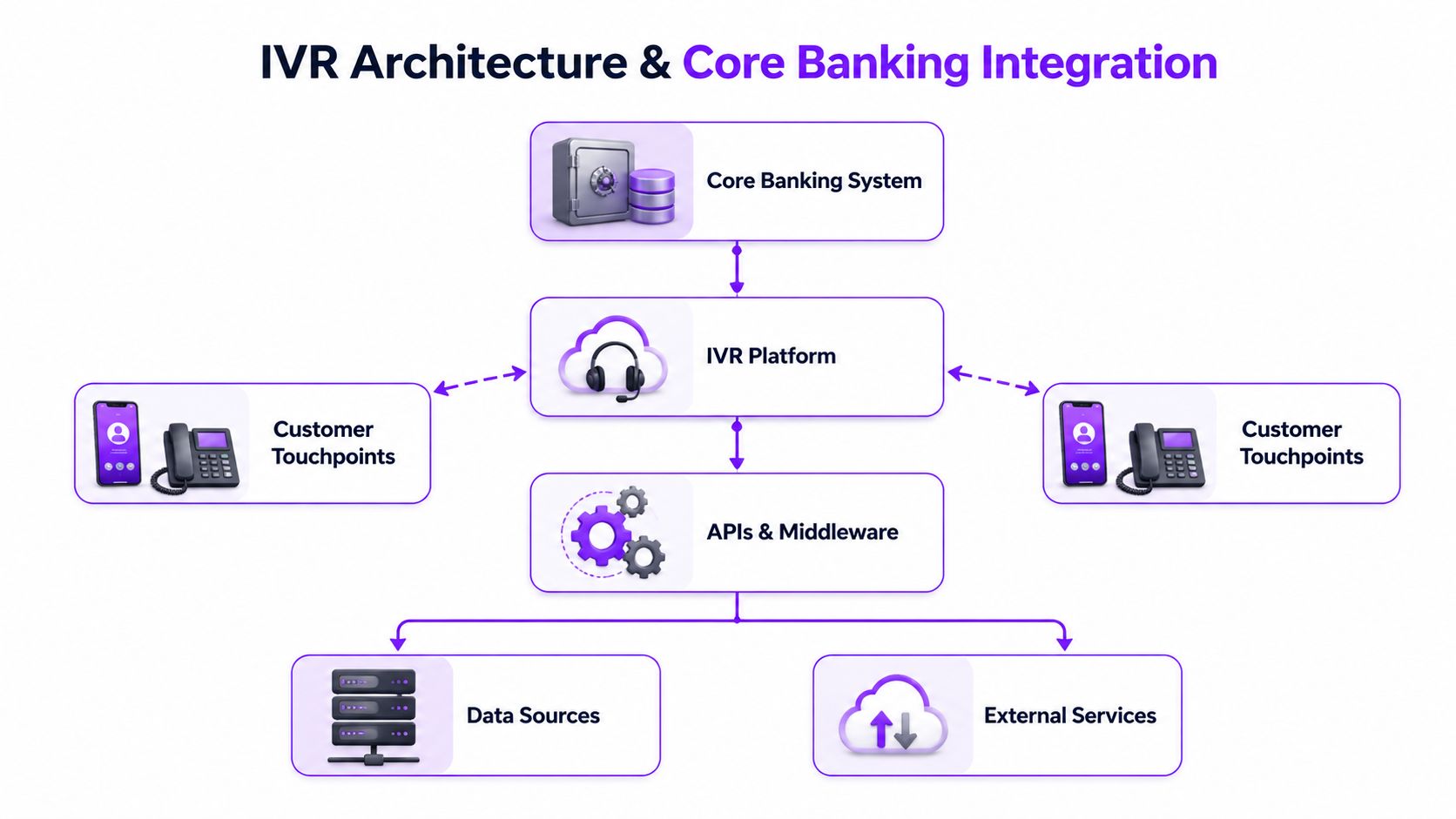

IVR Architecture and Core Banking Integration

Most banking leaders ask the right question too late. Not “Can AI-IVR speak naturally?” but “Can it work cleanly with our existing systems?” If the answer is weak, the project stalls in architecture review, risk review, or operations review.

A modern banking IVR should be treated as an intelligent orchestration layer sitting on top of existing infrastructure. It doesn’t need a rip-and-replace programme to create value. It needs disciplined integration.

Think of it as a control layer, not a phone tree

The cleanest mental model is a central nervous system.

The Core Banking System remains the system of record for balances, transactions, accounts, loans, and servicing events. The IVR platform sits in front as the interaction engine. It interprets speech, authenticates the caller, queries connected systems, and delivers the right action or response.

Between them sits APIs and middleware. That layer matters because most banks run mixed estates. Some functions are modern and API-ready. Others still live in older systems that require controlled connectivity.

The integration points that matter most

Core Banking System

The IVR pulls live account status, recent transactions, EMI schedules, and service eligibility. If the integration is delayed or batch-based, the customer hears stale information. That destroys trust immediately.

CRM and customer profile systems

Personalised IVR depends on context. The system should know the caller’s segment, language preference, active products, recent complaints, open service requests, and campaign eligibility. That’s how you move from generic menus to relevant conversations.

Payment and ecosystem rails

UPI-linked flows, Aadhaar-supported steps, card systems, loan origination systems, and credit bureau interfaces all expand what voice can complete. Without these links, the IVR only informs. With them, it resolves.

Risk, logging, and monitoring tools

Every banking voice interaction should feed audit trails, alerts, and operational analytics. If a conversation triggers a compliance risk or repeated authentication failure, downstream systems need to know.

What good implementation looks like

- Start with a narrow, high-volume journey: For example, card hotlisting or transaction status.

- Use middleware to isolate complexity: Don’t let the IVR directly depend on every backend variation.

- Separate orchestration from business logic: Keep rules maintainable so product, risk, and operations teams can govern change.

- Design for fallback: If an API fails, the caller should still receive a useful guided outcome or fast agent transfer.

A bank doesn’t need a perfect architecture map before it starts. It needs a practical one. The strongest programmes begin with one or two service journeys, prove stability, then extend into lending, payments, and proactive outreach. That’s how ivr services in bank environments scale without becoming another fragile channel project.

Ensuring Security and Compliance in Voice Banking

Security concerns often slow IVR modernisation. They shouldn’t. In banking, a well-designed voice channel can strengthen control, consistency, and auditability compared with loosely managed human-led processes.

The baseline has changed. Modern IVR systems now use multi-factor authentication through voice biometrics combined with OTP verification, and they process authentication in seconds, according to this overview of IVR security in banking. The same source states that these systems maintain continuous backend communication and can automatically trigger notifications for high-risk indicators such as payments from unexpected locations or multiple failed PIN attempts.

Why voice can be more secure than many legacy flows

Human-assisted verification often relies on static questions. Those questions are easy to social-engineer, inconsistent across agents, and poorly suited for high-volume environments. Voice-led authentication, by contrast, creates a more structured and repeatable control layer.

That doesn’t mean voice biometrics should stand alone. In banking, the right model is layered.

- Voice biometrics: Confirms who is speaking.

- OTP verification: Confirms possession of the registered device or contact path.

- Backend risk checks: Confirm whether the context of the request looks suspicious.

- Policy-led escalation: Sends high-risk cases to agent review or additional verification.

Compliance should be designed into the call flow

RBI alignment, internal audit expectations, and customer consent handling need to be built into the orchestration itself. Prompts, disclosures, authentication checkpoints, and action logs must be standardised. A regulated voice journey is not just a conversation. It is a governed process.

That’s why banks should pay close attention to control design, retention policies, and reviewability. If your team is assessing what that framework should look like in a regulated environment, this practical guide to compliance in bank voice workflows is a useful starting point.

Fraud detection must be immediate, not retrospective

One of the strongest advantages of AI-IVR is speed. If a suspicious transaction or pattern appears, the bank can trigger a voice workflow immediately. It can validate intent, warn the customer, log the interaction, and route the case based on risk.

Teams designing these controls should also study practical approaches to real-time fraud detection, because the value sits in orchestration across signals, not in any single rule.

A secure voice channel doesn’t ask only “Is this the customer?” It also asks “Does this request make sense right now?”

The executive checklist

| Control area | What the bank should require |

|---|---|

| Authentication | Voice biometrics plus OTP for sensitive actions |

| Auditability | Full logging of prompts, customer responses, and system decisions |

| Escalation | Clear fallback path for high-risk or failed verification cases |

| Data handling | Tight controls on storage, access, and retention of sensitive voice data |

| Monitoring | Real-time alerts for suspicious patterns and failed authentication sequences |

The strategic point is simple. Security is not a reason to delay IVR modernisation. It is one of the strongest reasons to accelerate it, provided the bank implements voice with proper governance.

Your Roadmap to IVR Modernisation in 2026

Most banks don’t fail in IVR transformation because the technology is immature. They fail because they buy loosely, govern weakly, and pilot the wrong journeys. If your executive committee wants measurable impact, the roadmap has to be disciplined from day one.

Choose a banking platform, not a generic voice vendor

A vendor demo can be misleading. Smooth voice playback and a polished dashboard don’t prove banking readiness.

Ask harder questions:

- Can the platform support multilingual Indian voice journeys at production quality

- Can it integrate with your CBS, CRM, and payment rails without fragile custom work

- Can policy teams review prompts, scripts, and escalation rules without engineering bottlenecks

- Can the system support secure logging, audit review, and controlled exception handling

Speech recognition quality also matters in Indian banking because callers switch languages, accents, and phrasing quickly. Teams evaluating the underlying stack should understand how models such as OpenAI's Whisper AI are shaping transcription quality and multilingual voice workflows.

Migrate in phases, not in one leap

The fastest route to executive scepticism is a giant transformation promise with no early proof. Replace that with phased delivery.

Phase one

Pick one high-volume, low-risk journey. Card blocking, balance enquiry, or transaction status are good candidates. The objective is operational proof, not grand innovation.

Phase two

Add CRM context and language personalisation, making the experience feel materially different to customers and more valuable to operations teams.

Phase three

Extend into higher-value journeys such as KYC guidance, lending support, fraud confirmation, and collections.

Executive advice: Don’t pilot the most complex journey first. Pilot the journey that will make your COO trust the data.

Manage change inside the bank

Technology teams usually understand the integration challenge. Business teams often underestimate the operating model change.

A modern IVR programme affects:

- Contact centre operations, because call types and escalation patterns shift

- Risk and compliance, because prompts and controls become codified

- Product teams, because service journeys become part of the digital product experience

- Branch and service teams, because customers arrive with different expectations after successful self-service

That means governance matters. One owner should be accountable for customer outcome, operating metrics, and cross-functional prioritisation.

Define a pilot that can survive scrutiny

A credible pilot needs explicit success criteria. Keep it simple and commercial.

Use measures such as:

- containment improvement

- reduction in agent transfers

- lower average handling time

- lower abandonment

- improvement in customer satisfaction for that specific journey

Then review failed calls manually. The learning from failed interactions is often more valuable than the headline success rate. It tells you where language models, backend integration, or policy logic still need work.

Banks that move decisively in 2026 won’t be the ones with the biggest telephony budget. They’ll be the ones with the clearest pilot design, the strongest governance, and the least tolerance for legacy menu sprawl.

Frequently Asked Questions about IVR in Banking

How long does it take to move from a legacy IVR to a conversational AI platform

There isn’t a single standard timeline because migration depends on integration complexity, governance approvals, and the number of journeys being modernised. The practical answer is to avoid treating this as one cutover event. Start with a contained service journey, prove stability, then expand.

Can modern IVR work with older on-premise core banking systems

Yes, if the integration architecture is designed properly. The IVR doesn’t need every legacy system to become modern overnight. Middleware, APIs, and controlled connectors can bridge older systems into a more flexible orchestration layer. What matters is data freshness, reliability, and fallback design.

Is AI-IVR the same thing as a voice bot

Not exactly. A voice bot is usually the conversational engine that understands and responds to speech. A modern IVR system is the wider service framework around that capability. It includes routing, authentication, integration, workflow control, logging, escalation, and policy handling. In banking, you need both.

Which banking journeys should be automated first

Start with high-volume, low-risk tasks that customers frequently need and agents shouldn’t spend time on. Card block requests, balance queries, statement requests, and transaction status checks are usually strong starting points. Once those are stable, expand into KYC guidance, fraud confirmation, and loan servicing.

Will customers still need access to human agents

Yes. Good IVR design doesn’t trap customers in automation. It resolves what should be automated and transfers what should be handled by a person. The bank should define escalation rules clearly so premium customers, vulnerable customers, and high-risk cases move quickly to the right human team.

What should the executive committee track after go-live

Track containment, abandonment, agent transfer rates, average handling time, customer satisfaction for automated journeys, and failure reasons by intent. Review these metrics at journey level, not only at a channel-wide average. That’s where the operational truth sits.

If your bank is evaluating the next step in voice automation, DialNexa Labs Private Limited is worth a serious look. The company builds human-like Voice AI agents for compliant customer support, qualification, and workflow automation across BFSI and other high-volume sectors. For executive teams that want practical pilots, fast deployment, and voice systems that can adapt to real operational journeys instead of generic demos, it offers a credible path from legacy IVR to modern AI-led service.

Leave a Reply