What Is Compliance in Banking? A Strategic Guide for Leaders

So, what is compliance in banking, really? For a senior leader, it's not just about rules; it's the strategic framework guiding your institution through the complex waters of financial regulation. Think of it as a sophisticated navigation system—one that not only avoids catastrophic risks but also charts a direct course to enhanced reputation, stakeholder trust, and sustainable profitability.

Why Banking Compliance Is a Strategic Advantage, Not a Burden

For any executive, viewing compliance as merely a "cost of doing business" is a critical strategic error. It’s not an operational burden; it’s a powerful business enabler. A robust compliance program is the bedrock that protects your institution's reputation, its operational stability, and, ultimately, its long-term enterprise value. In an industry where trust is the ultimate currency, compliance is your most valuable strategic asset.

The stakes are immense. Non-compliance carries a financial sting far greater than the investment in getting it right. In fact, a 2023 global study found that the average cost of non-compliance for financial firms reached $14.82 million, a figure that has risen 45% over the last decade. And that number doesn't even begin to quantify the catastrophic, and often permanent, damage a public scandal inflicts on a brand and its market capitalization.

The True Scope of Compliance

Effective banking compliance transcends a mere box-ticking exercise. It's a living, breathing commitment across the entire organization to operate with integrity and manage risk proactively. This strategic commitment manifests in several critical business areas:

- Protecting Financial Integrity: This is about preventing the bank from being used as a conduit for illicit activities, such as money laundering or terrorist financing.

- Ensuring Consumer Trust: Adherence to regulations that shield customers from unfair, deceptive, or abusive banking practices is non-negotiable for brand loyalty.

- Safeguarding Data: It means implementing rigorous security measures to protect sensitive customer information from data breaches, a top-of-mind concern for every board.

- Maintaining Market Stability: Following regulations that contribute to a stable and transparent financial system for all participants, bolstering investor confidence.

For a high-level overview, this table summarizes the core pillars every financial leader must master.

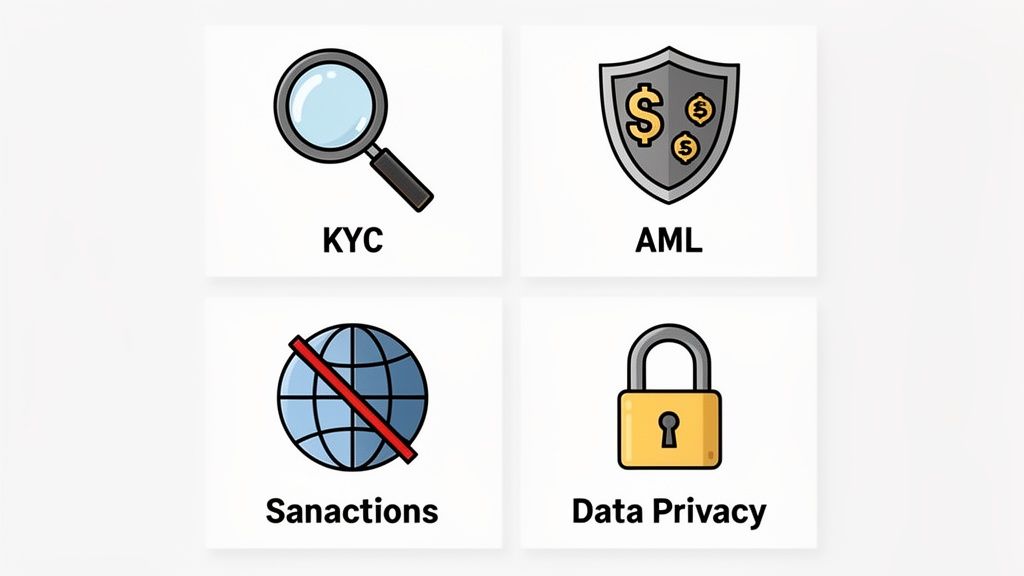

The Core Pillars of Banking Compliance

| Compliance Pillar | Primary Objective | Key Regulatory Body (India) |

|---|---|---|

| KYC & AML | Prevent illicit financial activities by verifying customer identities and monitoring transactions. | Reserve Bank of India (RBI) |

| Sanctions Screening | Ensure the bank does not conduct business with individuals or entities on official sanctions lists. | Ministry of Finance; RBI |

| Consumer Protection | Safeguard customers from unfair or deceptive practices, ensuring transparency and fairness. | RBI; SEBI |

| Data Privacy | Protect sensitive customer data from unauthorised access and breaches. | Ministry of Electronics and Information Technology (MeitY) |

These pillars are not siloed functions; they are interconnected components of a unified strategy to build a resilient and trustworthy institution.

Consider a practical example: A global bank's AI-powered system flags a series of small, seemingly unrelated international payments originating from a high-risk jurisdiction. This triggers an alert, and the compliance team discovers a sophisticated layering scheme designed to circumvent sanctions. By blocking the transactions, the bank not only averts a multi-million-dollar fine but also protects its correspondent banking relationships and reinforces its reputation as a diligent global partner.

This is the shift from reactive, rule-following compliance to a proactive, strategic powerhouse. A strong compliance culture drives customer loyalty, attracts top-tier talent, and creates a stable foundation for growth. It signals to the market, regulators, and your customers that you are a reliable, forward-thinking partner.

In this guide, we'll dissect the essentials of banking compliance, from the operational details of KYC and AML to navigating India's dynamic regulatory environment. Our goal is to equip you with the strategic insights needed to transform your compliance function from a cost center into a tangible competitive advantage that delivers lasting value.

Navigating the Core Areas of Banking Compliance

To truly master banking compliance, you must understand its core pillars not as separate checklists, but as deeply interconnected components of your institution's holistic risk management strategy. For an executive, translating these complex regulations into decisive actions is what protects the firm and unlocks pathways for sustainable growth.

Each pillar targets a specific risk category, from financial crime to consumer harm. Excelling in these areas is fundamental to a bank's resilience and market leadership. Let's break down what they involve at a strategic level.

Anti-Money Laundering and Counter-Terrorism Financing

At the forefront is the battle against illicit finance. Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) regulations are designed to prevent banks from being exploited by criminal enterprises. This legally mandates that banks monitor transactions, identify suspicious activity, and report findings to the authorities.

This is far from a procedural formality. It positions your institution as a critical gatekeeper in the global financial system. A world-class AML/CTF program is what insulates your brand from entanglement in serious crime, protecting your reputation and avoiding multi-billion-dollar fines. For example, global AML penalties exceeded $5 billion in 2022, underscoring the severe financial risk of failure.

India's robust focus on AML/CTF has not only fortified its financial system but also cemented its status as a global leader. Inward remittances are projected to reach a staggering $135.46 billion in FY 2025—the highest in the world. This achievement is directly supported by frameworks like the RBI's Payment Aggregator Cross-Border (PA-CB) license, which enforces strict fund segregation and capital adequacy.

Know Your Customer: The Foundation of Risk Management

The bedrock of any effective AML program is Know Your Customer (KYC). In essence, this is the process of verifying your customers' identities and understanding the nature of their financial activities. It is your first and most critical line of defense.

A robust KYC process includes:

- Customer Identification Program (CIP): Validating a customer's identity against reliable, independent documentation.

- Customer Due Diligence (CDD): Assessing a customer's risk profile based on their industry, geography, and transaction patterns.

- Enhanced Due Diligence (EDD): Conducting a deeper investigation into high-risk clients, such as politically exposed persons (PEPs), where scrutiny is intensified.

A failure in the KYC process creates a significant blind spot, rendering downstream monitoring and suspicious activity detection nearly impossible.

Sanctions Screening: A Global Imperative

Sanctions screening involves the critical task of checking customers and transactions against official lists of prohibited individuals, entities, and nations. These lists are maintained by governments and international bodies to enforce foreign policy and national security objectives.

For any bank with international operations, this is non-negotiable. A single transaction with a sanctioned party can trigger monumental fines, severe reputational damage, and de-risking actions that could cut off access to vital financial markets like the US dollar clearing system.

Practical Example: A European bank recently utilized an advanced AI screening tool that cross-referenced a payment with shipping manifests and vessel tracking data. The system flagged a transaction destined for a neutral port but linked to a vessel previously associated with a sanctioned entity. The bank blocked the payment, preventing a potential OFAC violation that could have cost hundreds of millions in penalties.

This demonstrates that proactive screening isn't just a compliance task—it's an active defense against enabling illicit global activities.

Consumer Protection and Data Privacy

Beyond financial crime, a significant portion of compliance focuses on safeguarding the customer. Consumer protection laws mandate fairness and transparency from banks, prohibiting deceptive marketing, predatory lending, and undisclosed fees. Adherence to these rules is fundamental to building long-term customer loyalty and brand equity.

Intricately linked to this is data privacy and security—a paramount concern for every senior leader. Banks are custodians of vast amounts of sensitive personal and financial data, and protecting it from breaches is a critical fiduciary duty. Regulations like India's Digital Personal Data Protection Act (DPDP Act) impose strict standards on data collection, usage, and security. A data breach can result in not only immense financial penalties but also an irretrievable loss of customer confidence.

To understand how industry leaders are navigating the intersection of technology, customer experience, and compliance, see our recap of a Voice Summit discussion with top financial services brands.

Understanding India's Regulatory Landscape

For any senior leader operating in Indian banking, a strategic understanding of the regulatory architecture is essential. Navigating compliance is not about rote memorization of rules; it's about appreciating the intent of the regulators who have designed the system to ensure stability, protect consumers, and maintain market integrity.

At the apex of this structure is the Reserve Bank of India (RBI). As the nation's central bank, established by the RBI Act of 1934 and further empowered by the Banking Regulation Act of 1949, the RBI is the ultimate supervisor of all banking firms in India. Its directives are not mere suggestions—they are foundational mandates that shape your institution's operational strategy, risk appetite, and growth trajectory.

The RBI’s purview is comprehensive. It sets the standards for everything from capital adequacy ratios and lending norms to the granular details of your KYC and AML frameworks. Its proactive supervision is designed to keep the banking sector resilient and responsive to evolving economic conditions.

The Key Players Shaping Financial Rules

While the RBI is the principal regulator, it collaborates with several other key bodies that govern specific segments of India's financial ecosystem. Understanding their distinct mandates is crucial for a holistic view of compliance.

- Securities and Exchange Board of India (SEBI): For institutions engaged in capital markets, SEBI is the primary regulator. It oversees securities, mutual funds, and market intermediaries, with a core mission to protect investor interests and ensure market fairness.

- Enforcement Directorate (ED): The ED is the country's premier financial investigation agency. It enforces economic laws and combats financial crime, intervening in cases of serious misconduct, particularly concerning foreign exchange and money laundering.

- Financial Intelligence Unit (FIU-IND): The FIU serves as the central repository for receiving, analyzing, and disseminating information on suspicious financial transactions. Banks are legally obligated to file Suspicious Transaction Reports (STRs) and Cash Transaction Reports (CTRs) with the FIU, making it a pivotal partner in combating financial crime.

These agencies form a multi-layered regulatory framework that demands strategic oversight from banking leadership. While each has a distinct mission, their collective goal is the safeguarding of India's financial system.

Core Legislation You Cannot Ignore

The authority of these bodies is anchored in powerful legislation. The most critical of these is the Prevention of Money Laundering Act (PMLA), 2002. This is more than a legal statute; the PMLA is the definitive operational playbook for combating money laundering, empowering authorities to seize assets linked to criminal proceeds. For any senior executive, a deep, practical understanding of PMLA obligations is non-negotiable.

A landmark example of regulatory evolution was the RBI's recent strategic overhaul, which involved implementing over 80 regulatory changes to streamline compliance and stimulate economic growth. This initiative signaled a move from crisis-era controls to growth-oriented policies, eliminating thousands of outdated circulars to free up bank balance sheets. These reforms were instrumental in boosting credit growth during a 'Goldilocks year' that saw inflation at just 2.2% and GDP growth hit 8%. You can explore more on these impactful regulatory shifts in the government's annual report.

This action by the RBI highlights a critical reality for every executive: the regulatory landscape is not static. It is a dynamic environment that evolves in response to economic needs and emerging threats.

Success requires proactive engagement, not passive compliance. By viewing regulators as partners in building a stable financial system, you can align your institution’s strategic goals with the national agenda. This transforms compliance from a defensive necessity into a true competitive advantage.

How to Build a Resilient Compliance Program

In today's dynamic financial landscape, a "check-the-box" compliance program is a liability waiting to happen. The objective is not mere adequacy; it is resilience. A resilient program anticipates risk, adapts swiftly to regulatory shifts, and fortifies the entire institution. This strength is not accidental—it is meticulously engineered with a structured approach that begins with executive leadership.

An effective program is not a separate function; it's woven into the corporate DNA. This starts with a clear "tone from the top," where the board and senior leadership don't just endorse compliance but champion it. When leaders consistently prioritize ethical conduct over short-term gains, that ethos permeates every level of the organization.

Establishing the Framework for Success

The organizational structure of your compliance function is critical. To ensure its authority and independence, the compliance department must have a direct reporting line to the board of directors or a dedicated board committee. This structure is the industry gold standard, as it mitigates conflicts of interest and guarantees that critical compliance matters receive the C-suite visibility they require.

With a solid structure in place, the next step is developing comprehensive policies and procedures. These are not static documents. They are the dynamic operating system for compliant behavior, continuously updated to reflect new regulations, emerging threats, and business evolution. To build a robust system, it is vital to understand its core components, which you can explore further by reading What Is a Compliance Program and How Do You Build One?

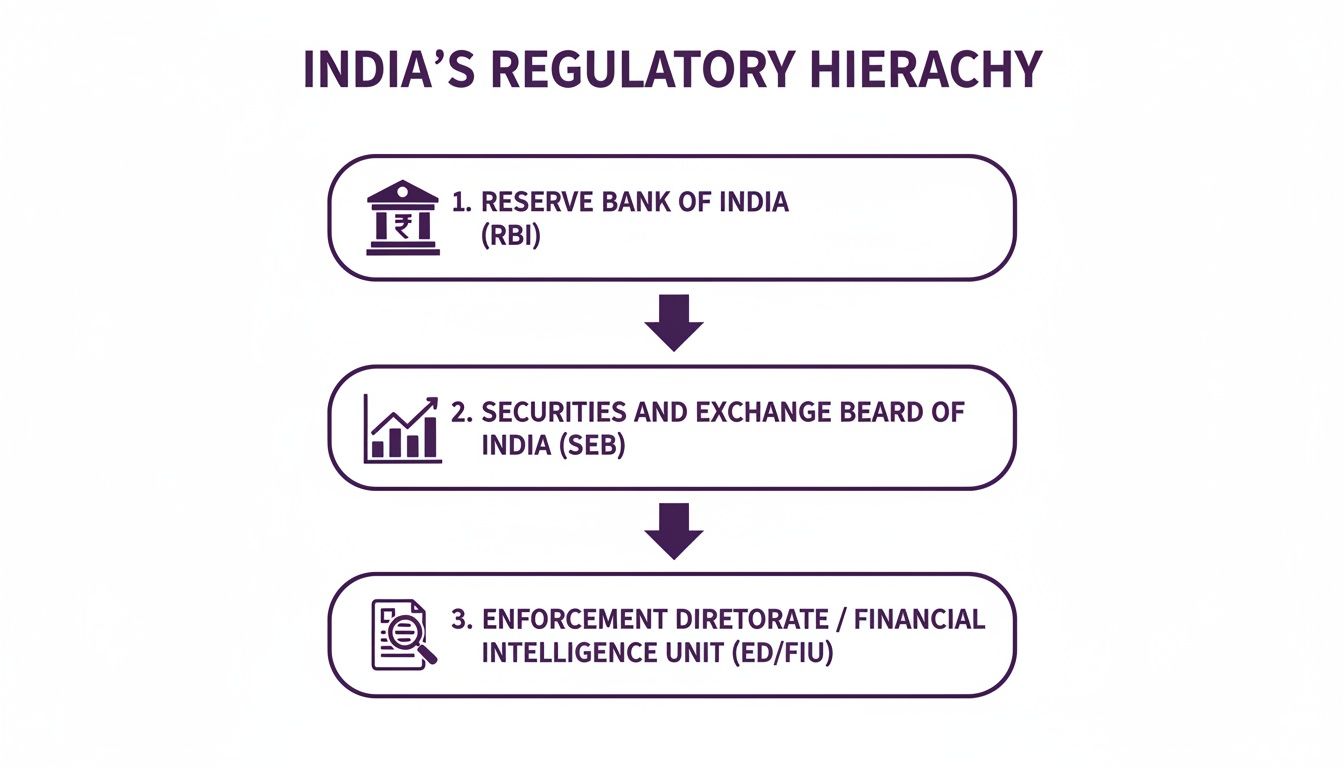

The infographic below illustrates the key regulatory bodies that shape these policies in India.

This hierarchy depicts the multi-layered supervisory environment created by the RBI, SEBI, and investigative bodies like the ED and FIU—a complex ecosystem that every Indian financial institution must strategically navigate.

From Reactive to Proactive Monitoring

Leading compliance functions are not just responding to issues; they are actively hunting for them. This requires a paradigm shift from periodic, manual audits to continuous monitoring. By leveraging technology to analyze transactions and customer activities in real-time, you can detect anomalies and potential red flags long before they escalate into material breaches.

For instance, an automated system can instantly flag a sudden, anomalous spike in cash deposits into a single account or a complex pattern of international wire transfers indicative of trade-based money laundering. This data-driven approach allows your compliance experts to focus on investigating genuine risks rather than being mired in routine manual checks. Modern AI-powered tools dramatically enhance the accuracy and efficiency of monitoring. Learn more about how technology is revolutionizing this space in our guide on regulatory compliance for Voice AI.

A recent enforcement trends report found that financial institutions without automated transaction monitoring were 50% more likely to face regulatory action for AML failures. This statistic makes the connection crystal clear: adopting the right technology directly reduces risk.

Embedding a Culture of Compliance

Superior policies and technology are only part of the equation. Their effectiveness is nullified without enterprise-wide adoption. Ongoing employee training is the mechanism that embeds a compliance culture across the organization. This training cannot be generic; it must be practical, relevant, and tailored to specific job functions.

Effective compliance training must address several key areas:

- Specific Regulatory Duties: A relationship manager's understanding of PMLA must be different from that of a back-office operations specialist.

- Identifying Red Flags: Equip employees to recognize suspicious activities they may encounter in their daily roles.

- Reporting Procedures: Implement clear, confidential channels for employees to escalate concerns without fear of retaliation.

Finally, a resilient program requires a robust incident response and reporting protocol. When a potential breach occurs, a clear, pre-defined playbook is needed to investigate, contain, and report the issue to regulators within statutory timelines. A well-rehearsed plan can be the difference between a manageable issue and a full-blown crisis, protecting both the institution and its leadership from severe repercussions.

The True Cost of Getting Compliance Wrong

It's one thing to discuss compliance in theory, but what are the tangible consequences of failure? The true cost extends far beyond regulatory fines. It is a domino effect of reputational collapse, shareholder value destruction, and a deep erosion of customer trust that can take a generation to rebuild. For any executive, understanding these severe, real-world consequences makes it undeniable that a proactive compliance framework is not an expense—it's an essential investment in survival.

When compliance is relegated to a back-office, check-box function, you are engineering a future disaster. The headlines are a constant reminder. Major global banks have been hit with multi-billion-dollar penalties for failures ranging from money laundering and sanctions evasion to consumer mistreatment. But those staggering fines? They are merely the entry point of the financial pain.

The Financial Fallout of Non-Compliance

Beneath the surface of a headline-grabbing penalty lies a cascade of secondary costs that directly impact the bottom line. Consider the aftermath of a major compliance scandal:

- Stock Value Erosion: A serious breach can vaporize billions in market capitalization overnight. In one notable case, a bank's stock plummeted over 30% in the months following a money laundering scandal, wiping out nearly $15 billion in shareholder value.

- Increased Scrutiny: Once an institution is on a regulator's watchlist, it faces years of intense oversight, resulting in higher operational costs, mandatory third-party audits, and business restrictions.

- Loss of Business: Correspondent banking relationships are severed. High-value corporate clients, whose own risk management policies demand trustworthy partners, migrate their business elsewhere.

The common denominator in these failures is almost always a culture that prioritized short-term revenue over long-term integrity, enabled by weak internal controls that were blind to clear warning signs.

A recent report calculated the average cost of a data breach for a financial institution at a staggering $5.97 million. This figure does not even begin to account for the long-tail costs of customer churn and reputational damage.

A Look at the Indian Context

Here in India, the stakes are equally high. The regulatory push for stricter compliance is a direct response to the rise in sophisticated financial fraud and operational risks. For instance, the Department of Financial Services now mandates systematic checks on high-value accounts for any indication of willful default or fraud. This involves rigorous quality controls and third-party audits under the direct supervision of the RBI. A recent KPMG report provides deep insights into how these pressures are reshaping the Indian banking landscape.

In this environment, a deeply embedded culture of compliance is non-negotiable. It requires more than policies; it requires people who understand their personal accountability in protecting the institution. This is where continuous learning becomes paramount, supported by comprehensive regulatory compliance training that ensures every employee—from the frontline teller to the CEO—is equipped to identify and manage risk.

Ultimately, the cost of non-compliance is the price paid for inaction. It's the market share lost to more trusted competitors, the top talent you cannot attract, and the growth opportunities missed because your institution is perceived as a high-risk partner. Investing in a resilient compliance program isn't an expense; it is the most critical investment a bank can make in its own future.

Using Technology to Future-Proof Your Compliance Strategy

Relying on manual, reactive compliance processes is no longer a viable strategy—it is a significant institutional liability. To stay ahead of regulatory evolution and emerging risks, forward-thinking leaders are leveraging technology to transform compliance from a cost center into a data-driven, strategic asset.

This transformation is being driven by Regulatory Technology (RegTech), a suite of solutions engineered to automate and enhance compliance operations from the ground up.

Instead of relying on slow, error-prone human review, RegTech applies automation to execute high-volume tasks with superior precision and speed. The strategic imperative is to move faster, gain clearer insights, and act with greater intelligence. Adopting this proactive posture is essential for any institution serious about its compliance obligations.

For executives, the ultimate advantage comes from elevating beyond simple automation to predictive intelligence. This is the domain of Artificial Intelligence (AI) and Machine Learning (ML).

The Strategic Value of AI and Machine Learning

AI and ML are game-changers for identifying risks before they escalate into material incidents. These systems can analyze millions of transactions in real-time, detecting subtle patterns and anomalies that are invisible to human teams. This capability is fundamental for building a robust defense against increasingly sophisticated financial criminals.

So, where does AI deliver immediate, tangible impact for a CXO?

- Advanced Transaction Monitoring: AI algorithms excel at distinguishing between normal and suspicious behavior. This can slash false positive alerts by up to 75%, liberating skilled compliance officers to focus their expertise on investigating genuine threats.

- Predictive Risk Analytics: By learning from historical data, ML models can forecast potential compliance hotspots, enabling you to allocate resources more effectively and strengthen controls where they are needed most.

- Intelligent Fraud Detection: AI can identify and block fraudulent activities in real-time, protecting both the bank's assets and its customers' trust.

Case in Point: A leading European bank integrated AI into its transaction monitoring system and improved its detection of complex money laundering schemes by over 60%. Simultaneously, it reduced investigation times by 50%. This is a clear demonstration of how strategic technology investment creates a stronger, more efficient compliance framework.

How Voice AI Strengthens Your Compliance Posture

Technological innovation is not confined to back-office functions; it is now enhancing compliance at the front lines of customer interaction. Modern Voice AI agents are emerging as a powerful tool for embedding compliance directly into the customer journey. Every conversation becomes a perfectly documented, fully auditable event.

Consider the KYC verification process. A Voice AI agent ensures every mandatory disclosure is delivered flawlessly, every single time. This eliminates the risk of human error or omission. The resulting call recordings and transcripts create an unimpeachable audit trail, providing definitive proof that established processes were followed meticulously.

This level of consistency is unattainable with human agents alone. The benefits extend beyond risk management. Firms that have adopted Voice AI have seen lead-to-booking rates increase from 2% to 8% while maintaining a 97% qualification accuracy.

Explore a real-world example of this synergy in action and learn how RCBC credits its AI and human customer service model for a compelling look at how AI enhances both operational excellence and compliance.

Frequently Asked Questions About Banking Compliance

Even with a robust strategy, senior leaders often have pressing questions about navigating the complexities of banking compliance. Here are direct answers to the questions we hear most frequently from executives.

What’s the Biggest Compliance Challenge for Banks Today?

Without question, the single greatest challenge is the velocity and volume of regulatory change. Regulators are constantly issuing new rules to address modern risks, from sophisticated cyber threats and digital assets to geopolitical instability.

Simultaneously, the delivery of banking services is being fundamentally reshaped by technology. The key for leadership is to architect a compliance framework that is agile by design. This involves using technology to anticipate regulatory shifts, not merely react to them. It demands strategic investments in both flexible systems and high-caliber talent capable of navigating this dynamic environment.

A recent global survey of financial services executives revealed that 72% expect the volume of regulatory information to increase significantly in the next year. Furthermore, 68% believe the pace of this change will accelerate.

These figures underscore the strategic necessity of a forward-thinking, adaptive compliance posture.

How Do We Build a Genuine Culture of Compliance?

A true culture of compliance is seeded from the top. It cannot be a platitude in a mission statement; it must be a visible, unwavering commitment from the board and C-suite, demonstrated through their actions.

This means integrating compliance objectives directly into performance metrics and incentive structures. It involves publicly recognizing employees who are proactive in managing risk and making it unequivocally clear that ethical conduct is prioritized—even when it means forgoing short-term revenue. When your entire team sees leadership making every strategic decision through a compliance lens, that ethos becomes embedded in the corporate DNA.

Can Smaller Firms Afford a Robust Compliance Programme?

Yes, absolutely. Effective compliance is more about strategic efficiency than budget size. Smaller institutions can now leverage powerful RegTech and cloud-based solutions that were once the exclusive domain of large global banks.

These technologies automate essential functions like transaction monitoring, risk assessments, and reporting at a fraction of the cost of traditional methods. By adopting a risk-based approach, smaller firms can identify their most significant vulnerabilities and concentrate their resources accordingly, building a highly effective and defensible compliance program without prohibitive capital expenditure.

Ready to fortify your compliance framework with technology that delivers results? DialNexa provides intelligent Voice AI agents that ensure standardised, auditable customer interactions for KYC and support, reducing human error and strengthening your defence against risk. Discover how DialNexa can transform your compliance strategy today.

This is a highly insightful and comprehensive piece that clearly shows how compliance can evolve from a regulatory obligation into a strategic business advantage. The strong focus on technology, culture, and proactive risk management makes it especially valuable for modern banking leaders.

[…] when conversations move quickly and decisions are made in the moment. Teams that understand what compliance in banking requires at the operating level are in a better position to reduce enforcement risk without creating unnecessary friction for […]