What Is KYC Compliance: Your 2026 Business Guide

Aadhaar-based eKYC authentication in India has crossed well over 90 billion lifetime transactions according to Plaid's overview of KYC in India. That single figure should change how boards think about KYC. This is no longer a narrow compliance task for banks. It's an operational system at national scale.

If you're still asking what is KYC compliance, ask the better question. How does your business verify identity, assess risk, and keep that decision current without slowing growth, frustrating customers, or exposing the company to avoidable risk? For banks and NBFCs, that's a regulated obligation. For real estate, EdTech, SaaS, healthcare, and e-commerce, it's often the difference between controlled scale and expensive chaos.

KYC deserves board attention because it sits at the intersection of risk control, customer experience, and process design. A weak framework creates fraud exposure, broken onboarding journeys, poor audit readiness, and reactive operations. A strong one makes onboarding faster, escalations cleaner, and growth more defensible.

Table of Contents

- Beyond the Acronym Understanding KYC

- The Strategic Imperative of KYC Compliance

- Deconstructing the Core Pillars of KYC

- KYC Across Industries What CXOs Need to Know

- Building a Modern KYC Framework Practical Steps

- Common Pitfalls and How to Avoid Them

- Your Executive KYC Compliance Checklist

Beyond the Acronym Understanding KYC

KYC compliance means knowing who your customer is, what risk they present, and whether that risk changes over time. That sounds simple. It isn't.

In India, KYC has been a formal compliance control for financial institutions for more than two decades, anchored in the Prevention of Money Laundering Act, 2002 and the RBI's Master Direction on KYC, with requirements tied to identity verification, customer due diligence, and ongoing monitoring throughout the relationship, as outlined in this Indian AML and KYC compliance overview. The key point for directors is that KYC isn't document collection. It's a controlled decision-making system.

That distinction matters because executives often treat KYC as an onboarding checklist owned by operations. That's a mistake. KYC informs who you accept, what friction you introduce, when you escalate, and how confidently you can scale.

Board view: KYC is a trust infrastructure. If identity, risk review, and monitoring are weak, every downstream process inherits that weakness.

For a bank, this governs account opening and transaction risk. For a brokerage, it shapes suitability and surveillance. For a real estate company, it influences whether buyer and investor funds are handled with confidence. If you want a practical industry-specific example, this guide to real estate investor verification is useful because it shows how KYC logic extends beyond pure banking workflows.

Three executive truths define KYC in practice:

- It's continuous: Initial verification isn't enough if customer details, ownership structure, sanctions exposure, or behavioural risk changes later.

- It's operational: Your compliance policy is only as good as the workflow, escalation path, and data quality behind it.

- It's strategic: Good KYC reduces avoidable risk while preserving conversion and service quality.

If your organisation handles customer onboarding at volume, KYC isn't a legal footnote. It's part of your growth engine.

The Strategic Imperative of KYC Compliance

Enforcement action under India's anti-money laundering regime is not a theoretical risk. The RBI Master Direction on Know Your Customer (KYC) makes board accountability, customer identification, monitoring, and recordkeeping explicit. Directors should treat KYC the same way they treat credit controls, cyber resilience, and financial reporting. It protects revenue quality, preserves operating capacity, and limits losses that scale fast once bad customers enter the system.

Governance risk starts at the top

KYC belongs in board reporting because it affects three numbers executives already care about. Loss rates, onboarding conversion, and operating cost per customer.

If your teams cannot show why a customer was approved, rejected, or escalated, you have a control problem. If reviews sit in inboxes, if policy exceptions are undocumented, or if ownership data cannot be retrieved during an audit, you have a governance problem. Those failures do not stay inside compliance. They disrupt fundraising, delay partnerships, weaken audit outcomes, and increase the cost of expansion into new products or geographies.

Boards in financial services already understand this. Leaders in other sectors should adopt the same standard. This article on the operational realities of banking compliance is useful because it shows how policy becomes workflow, approval logic, and evidence.

Bad KYC raises cost and lowers growth quality

Poor KYC design creates expensive friction. Teams ask for the same document twice, reviewers make inconsistent calls, customers wait longer, and higher-value applicants abandon the process. The result is measurable. More manual touchpoints, more exception queues, and more rework per approved customer.

Well-run KYC does the opposite. It reduces review time for low-risk applicants, pushes high-risk cases into clear escalation paths, and gives operations teams a standard way to work at volume. That matters in BFSI, but it matters just as much in Indian SaaS, EdTech, and real estate businesses where onboarding speed affects CAC recovery, sales velocity, and partner trust.

The strategic payoff is straightforward:

- Lower fraud and exposure costs: Early screening keeps bad actors, sanctioned parties, and misrepresented entities out of your funnel.

- Better unit economics: Fewer manual reviews and cleaner data reduce cost per onboarding case.

- Higher conversion quality: Good applicants face fewer avoidable delays, which protects revenue without weakening controls.

- Stronger audit defensibility: Decision logs, documented exceptions, and traceable approvals cut remediation effort when auditors or regulators ask questions.

Strong KYC supports scale because it standardises judgment.

Regulation is converging on operational proof

Supervisors increasingly test whether controls work in practice, not whether a policy document exists. That pattern is visible across markets. This explainer on the market conduct authority for SA businesses shows the wider direction of travel. Firms are expected to embed conduct and verification into daily operations.

India is moving the same way. A KYC programme that lives only in policy files will fail under stress. CXOs need a model that connects identity checks, risk scoring, exception handling, refresh cycles, and monitoring into one operating system. That is how compliance stops being a cost centre and starts protecting margins, customer experience, and expansion readiness.

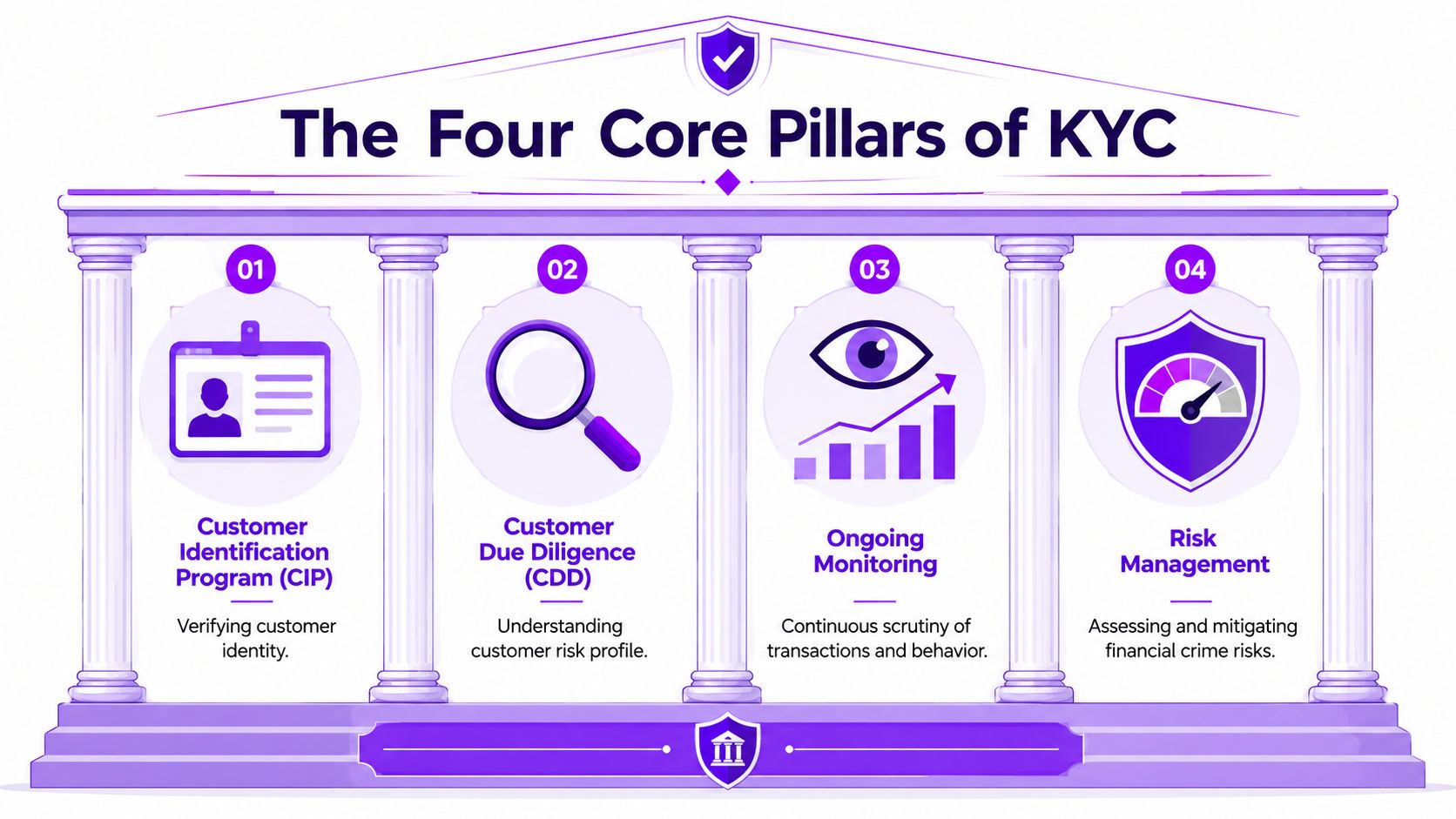

Deconstructing the Core Pillars of KYC

KYC works when leaders understand it as a layered control model rather than a single check. The core pillars are interconnected. If one breaks, the whole system becomes unreliable.

Identity is only the starting point

The first layer is the Customer Identification Programme, often shortened to CIP. You verify that the customer is who they claim to be using reliable evidence. In digital environments, that usually means combining document review with checks that reduce impersonation risk.

The second layer is Customer Due Diligence, or CDD. This isn't about identity alone. It's about context. What is the nature of the relationship? What type of customer is this? What level of risk does that profile suggest?

Here is the simplest executive breakdown:

- CIP verifies identity

A name, an ID, and a matching person or authorised entity. - CDD assesses risk

Why is this customer here, what's the expected pattern, and does anything require escalation? - EDD goes deeper

Higher-risk cases demand stronger review, more evidence, and tighter approval controls. - Ongoing monitoring keeps the file alive

Risk doesn't stay frozen after onboarding.

Layered controls beat checkbox compliance

Industry guidance for financial services describes the technical stack as layered controls that include document verification, biometric and liveness checks, watchlist screening, and enhanced due diligence for higher-risk customers, with AI and machine learning increasingly used to automate identity verification and risk scoring, as described in Sumsub's KYC and fintech compliance guide.

That layered model matters because each pillar answers a different risk question:

| Pillar | Core question | Typical executive concern |

|---|---|---|

| CIP | Is this person or entity real? | Fraud, impersonation, fake identities |

| CDD | Should we onboard this customer? | Risk classification, business fit |

| EDD | Do we need stronger scrutiny? | High-risk clients, adverse exposure |

| Ongoing monitoring | Has anything changed? | Drift in risk, missed alerts, stale records |

A mature programme doesn't force every customer through the same intensity of checks. It applies proportionate controls. Low-risk cases move quickly. Higher-risk cases trigger deeper review and tighter sign-off.

That's where tooling matters. Some businesses use document verification vendors. Some add biometric matching. Some need specialist controls such as voiceprint authentication in customer verification workflows when voice-led interactions are part of the operating model. The point isn't to collect tools. It's to align controls with risk.

Practical rule: If your team can't clearly explain why one customer received standard review and another received enhanced review, your KYC model isn't mature enough.

KYC Across Industries What CXOs Need to Know

India processed millions of Aadhaar authentication transactions every day, and UIDAI's monthly authentication updates make one point clear: identity verification now sits inside mainstream digital operations, not just regulated finance, as shown in UIDAI's authentication and e-KYC transaction reports. CXOs who still treat KYC as a narrow banking obligation are making an operating mistake.

The executive question is broader. Where does your business face identity risk, payment risk, fraud loss, regulatory exposure, or onboarding friction that can be reduced through structured verification? Answer that properly and KYC stops being a cost line item. It becomes a control system for margin protection, conversion quality, and scale.

Regulated sectors need board-level discipline

Banks, NBFCs, brokers, insurers, and payment companies do not have room for informal practice. Their KYC model affects regulatory standing, fraud loss, investigation cost, and onboarding speed at the same time. Weak controls create direct financial consequences. More false positives increase review headcount. More false negatives increase loss events, audit findings, and remediation spend.

Real estate deserves the same board attention, even if the exact legal structure differs from BFSI. High-ticket transactions, layered ownership, intermediaries, and source-of-funds concerns create obvious exposure. A developer or brokerage that cannot verify buyers, investors, and beneficial owners will eventually pay for it through delayed closings, disputes, reputational damage, or all three.

Non-regulated sectors still need structured verification

EdTech, SaaS, healthcare, marketplaces, and consumer internet businesses often frame verification as a fraud feature owned by operations. That is too limited. In these sectors, identity checks shape refund abuse, account takeover rates, financing misuse, duplicate accounts, trust and safety incidents, and support workload.

A simple example makes the point. If a SaaS platform allows fake business sign-ups at scale, sales metrics get distorted, trial infrastructure costs rise, abuse teams grow, and conversion forecasting becomes unreliable. If an EdTech company cannot validate the learner, guardian, payer, or consent trail, chargebacks and disputes rise while collections efficiency falls.

Customer experience also depends on the design of these controls. Poorly placed verification steps increase abandonment. Well-designed checks reduce manual review and keep legitimate users moving. Companies already investing in digital service journeys should connect identity controls to the same operating model used for chatbots in banking customer journeys. The point is consistency. Risk checks should support speed, not work against it.

A board-level view helps separate legal obligation from business necessity:

| Sector | Primary business driver | Executive risk exposure | Verification priority |

|---|---|---|---|

| BFSI and fintech | Regulatory compliance and fraud control | AML breaches, sanctions exposure, impersonation, supervisory action | Identity proofing, due diligence, monitoring, periodic refresh |

| Real estate | Transaction integrity and source-of-funds control | Fraud, opaque ownership, delayed closings, reputational damage | Buyer or investor identity, beneficial ownership, supporting records |

| EdTech | Enrolment quality and payment integrity | Fake applicants, refund abuse, financing misuse, consent disputes | Student or guardian verification, payer validation, consent capture |

| SaaS | Platform trust and revenue quality | Fake companies, trial abuse, account misuse, bad pipeline data | Business verification, authorised user checks, risk-based escalation |

| E-commerce and D2C | Order protection and margin control | Account takeover, return fraud, refund abuse, payment disputes | Identity signals, payment verification, exception handling |

| Healthcare platforms | Patient safety and record accuracy | Misidentification, misuse of benefits, billing conflict, privacy incidents | Patient identity, consent records, verified contact details |

The recommendation is straightforward. Map KYC intensity to transaction value, fraud exposure, and regulatory risk by industry. Do not copy a bank workflow into a SaaS product. Do not run a high-value real estate transaction with consumer-grade checks. And do not assume a non-regulated label protects the business from verification failures. It does not.

Strong operators treat KYC as part of commercial infrastructure. It protects revenue, improves approval quality, reduces manual handling, and gives the business a cleaner path to scale.

Building a Modern KYC Framework Practical Steps

Most companies don't fail because they ignore KYC entirely. They fail because they bolt controls onto a broken onboarding process and call it compliance.

India's digital KYC infrastructure has evolved rapidly, especially with Aadhaar-based e-KYC, and modern KYC programmes increasingly use real-time monitoring because manual review is too slow for a high-volume digital financial ecosystem, as explained in Sumsub's guide to modern KYC operations.

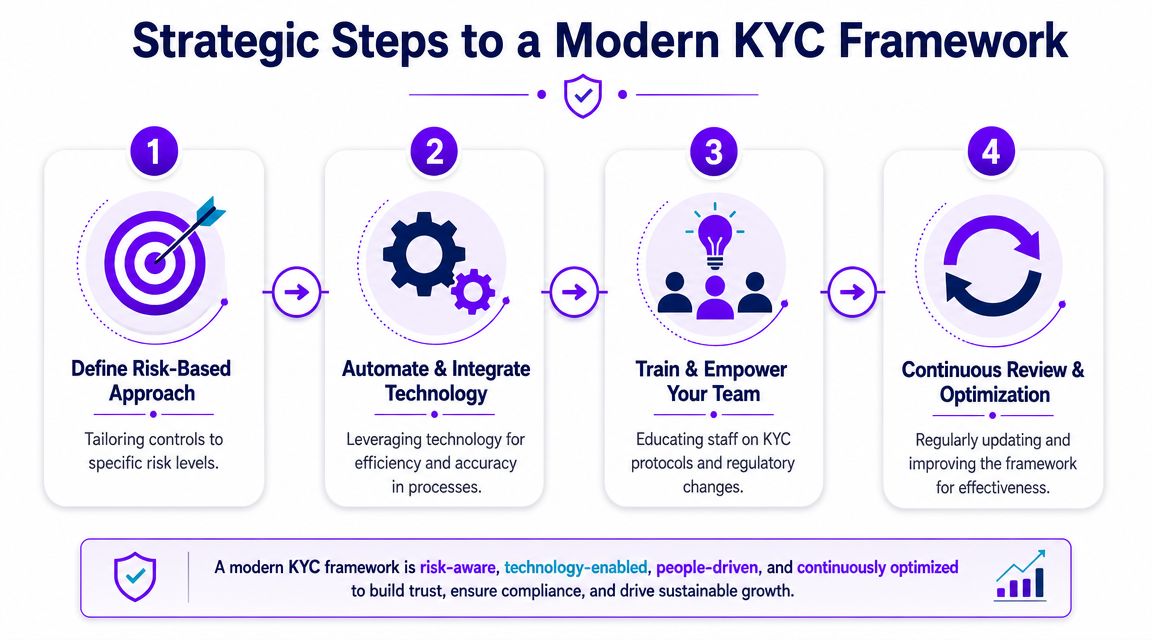

A workable framework starts with operating discipline, then adds technology.

Set the operating model before buying tools

Step one is risk design. Define your customer segments, risk indicators, approval thresholds, and refresh triggers. If your organisation can't describe which customers are low, medium, or high risk and why, no software will fix the confusion.

Step two is workflow design. Decide what happens at onboarding, what evidence is mandatory, where exceptions go, who can approve overrides, and how records are stored. Many firms lose control in this area when the process operates based on team habits instead of a governed workflow.

Use a simple decision structure:

- Standard journey: Low-friction path for straightforward cases

- Escalation path: Additional review when documents are unclear, expired, inconsistent, or incomplete

- Enhanced review path: Senior review for higher-risk profiles or unusual fact patterns

- Refresh cycle: Periodic re-checks and trigger-based monitoring during the relationship

A short explainer can help teams visualise the customer side of this operating model:

Automate the journey and keep humans for judgement

Step three is technology integration. Use automation for repeatable checks and humans for exception handling. Document verification, liveness prompts, watchlist screening, data extraction, and case routing should not sit in disconnected tools if you expect scale.

This is also where customer communication matters. If users don't understand what to upload, why they were flagged, or how to correct an issue, your support queues swell and completion rates suffer. Some organisations use conversational support tools to guide applicants through those steps. For example, chatbots in banking illustrate how guided interactions can reduce repetitive service load in regulated flows. In the same category, DialNexa Labs Private Limited offers Voice AI agents that can handle KYC-related guidance and support conversations as part of broader onboarding and service workflows.

Step four is governance and review. Train frontline teams, compliance staff, and business owners on roles and escalation logic. Then review the framework regularly. Not every problem is a compliance problem. Some are product design flaws, poor customer instructions, or fragmented data models.

If your KYC backlog grows every time customer volume rises, your issue isn't just compliance capacity. It's process architecture.

Boards should ask for evidence of turnaround times, exception reasons, and rework patterns. Those indicators reveal whether KYC is scalable or merely staffed.

Common Pitfalls and How to Avoid Them

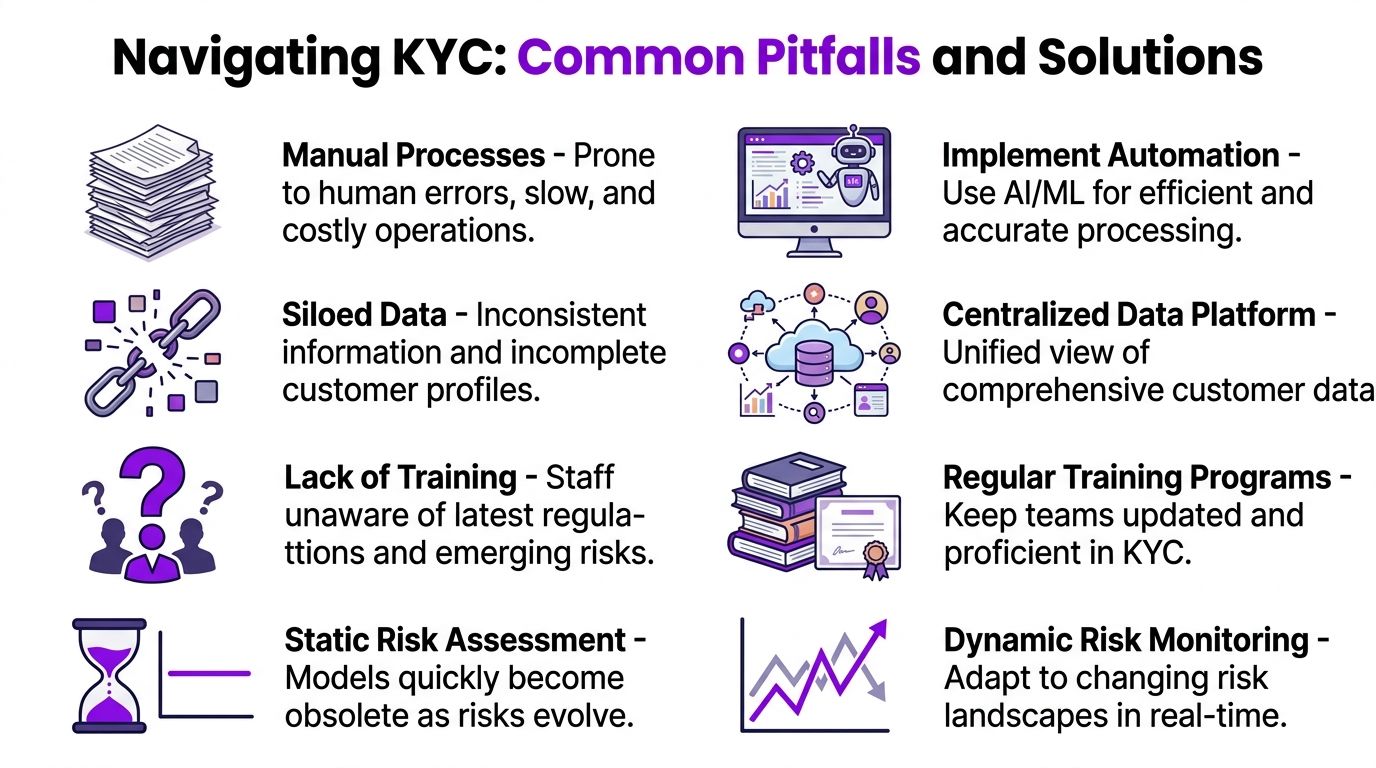

Most weak KYC programmes share the same habits. They rely on heroic manual effort, stale assumptions, and fragmented data. That combination creates false confidence.

The failure patterns boards should challenge

Pitfall one is treating KYC as a one-time event. This is the most common strategic error. Customer risk changes, ownership changes, documents expire, and new alerts emerge. If the organisation only verifies at entry, the control deteriorates from day one.

Fix it: Build review triggers into the lifecycle. Refresh records periodically and re-assess when customer behaviour, profile, or exposure changes.

Pitfall two is over-reliance on manual review. Manual checks look safer because humans are involved. In reality, they often produce inconsistent decisions, backlogs, and preventable errors when volumes rise.

Fix it: Automate repeatable tasks and reserve specialist review for exceptions, edge cases, and high-risk escalations.

Pitfall three is poor data quality. If customer information sits across email threads, spreadsheets, CRM notes, and vendor dashboards, monitoring becomes unreliable. Your team can't detect patterns if the record isn't coherent.

Fix it: Create a single governed customer record or, at minimum, a controlled system of synchronised data ownership.

Pitfall four is static risk logic. Risk models become obsolete when product lines, customer types, channels, or threat patterns change. Boards often approve a policy once and assume it remains fit for purpose.

Fix it: Review risk rules with business changes, not just annual policy cycles.

A sharp executive test is useful here:

- Can we explain our current escalation thresholds clearly?

- Can we show why a customer was approved, rejected, or escalated?

- Can we identify where delays come from in the verification journey?

- Can we update controls quickly when the operating model changes?

Weak KYC programmes don't usually collapse from a single dramatic error. Teams let small exceptions pile up until the framework stops being credible.

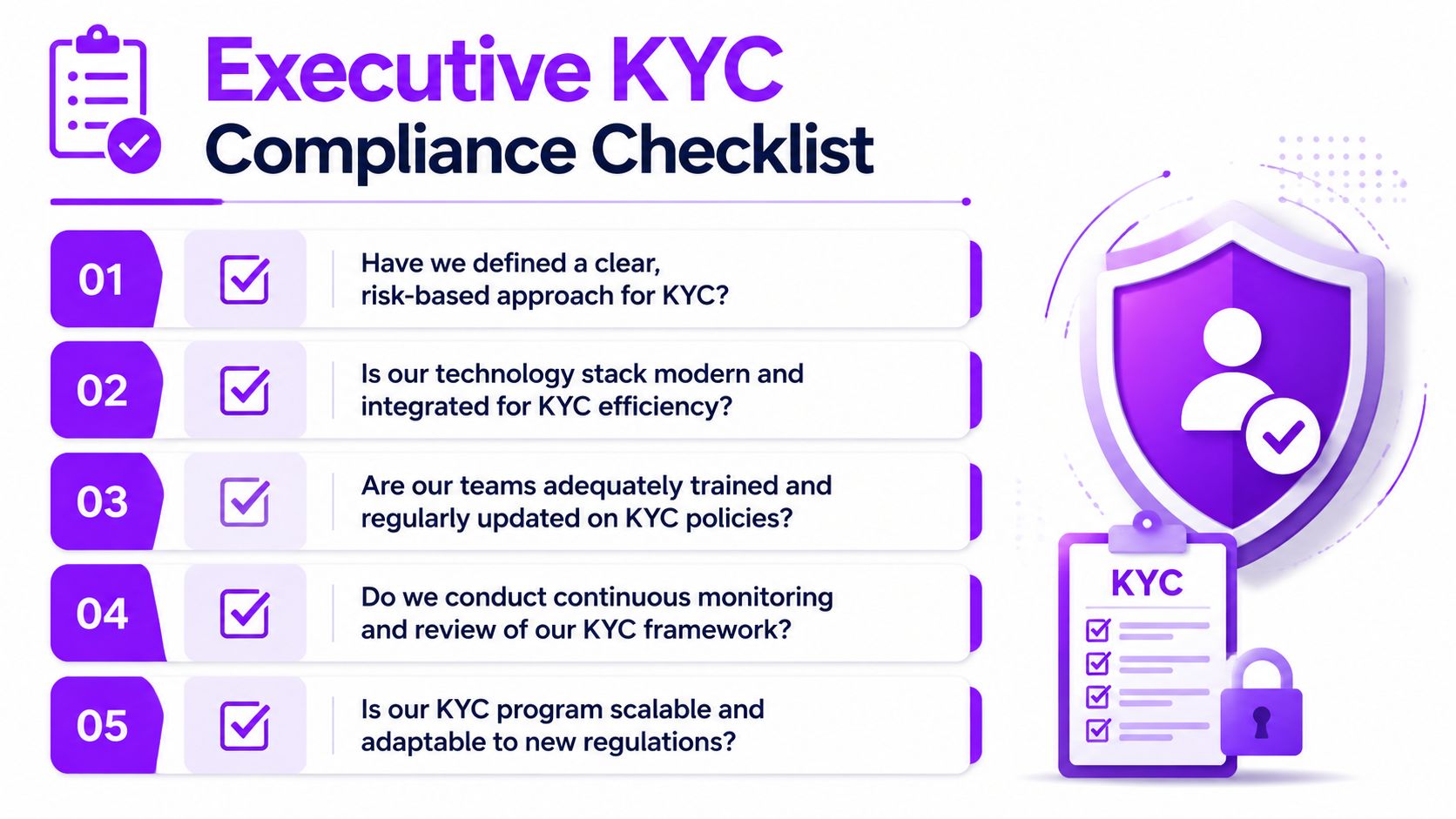

Your Executive KYC Compliance Checklist

Directors don't need to inspect every case file. They do need to know whether the KYC programme is designed to support lawful, efficient growth.

Use these questions in your next operating review:

- Have we defined a risk-based model clearly? Management should be able to explain customer segmentation, risk triggers, enhanced review criteria, and refresh logic without ambiguity.

- Is the onboarding workflow governed end to end? That includes evidence requirements, exception handling, ownership, and audit trail quality.

- Is our technology stack integrated enough to support scale? Disconnected tools create blind spots, duplicate work, and inconsistent decisions.

- Do teams know what good looks like? Frontline staff, compliance reviewers, support teams, and business owners need role-specific training and escalation clarity.

- Are we monitoring the programme, not just individual customers? Boards should review operational signals such as exception patterns, turnaround bottlenecks, repeat document requests, and unresolved review queues.

If the answer to any of those questions is vague, your KYC programme needs attention. The right goal isn't maximal friction. It's proportionate control with clean execution.

KYC becomes a strategic asset when the business can onboard legitimate customers confidently, escalate risk consistently, and adapt the framework without operational drama. That's the standard boards should demand.

If your team wants to reduce repetitive KYC support work while keeping onboarding conversations structured, DialNexa Labs Private Limited provides Voice AI agents that can guide applicants, answer verification-related questions, and support customer operations across BFSI, real estate, EdTech, healthcare, e-commerce, and SaaS workflows.

An outstanding article that explains KYC as a strategic business infrastructure rather than just a compliance requirement. The clear industry examples and focus on governance, risk-based controls, and scalable operations make this a valuable resource for executives and decision-makers.

[…] useful executive refresher on this area is this guide to KYC compliance, particularly for teams trying to align product, operations, and risk […]