Mastering Financial Services Compliance in 2026

USD 1.5 billion in 2025, on track for USD 5.1 billion by 2031 at a 21.50% CAGR. For boards and executive teams, that growth signals a clear shift. Compliance is now an operating model decision with direct implications for risk exposure, cost to serve, and speed to market.

The pressure is no longer limited to periodic audits or policy updates. Financial institutions are expected to control customer onboarding, transaction monitoring, recordkeeping, disclosures, and third-party activity in real time, across digital and human channels. Firms that still treat compliance as a downstream review function usually pay for it through slower onboarding, higher exception rates, fragmented oversight, and avoidable remediation work.

One gap deserves more attention than it gets. Voice interactions remain a weak point in many compliance programs, even though they sit inside sales, service, collections, and advisory workflows where regulated statements, customer consent, identity verification, and dispute handling all happen live. A policy can be well written and still fail in practice if the call flow, agent guidance, monitoring, and evidence trail are not designed to support it.

That is why financial services compliance should be evaluated as an execution discipline, not just a legal requirement. The central question is whether controls hold up during customer-facing interactions at scale, especially when conversations move quickly and decisions are made in the moment. Teams that understand what compliance in banking requires at the operating level are in a better position to reduce enforcement risk without creating unnecessary friction for customers or front-line staff.

Data quality sits at the center of that effort. Poor data breaks screening, weakens surveillance, slows investigations, and creates false confidence in management reporting. The article on financial data quality challenges shows why institutions lose money when compliance data is incomplete, inconsistent, or disconnected across systems.

An effective compliance program protects more than regulatory standing. It protects margin, reputation, and the firm's ability to grow without adding operational instability.

Table of Contents

- The New Compliance Imperative in Financial Services

- Understanding the Core Pillars of Financial Compliance

- Strategic Risk Assessment and Control Frameworks

- Building a Modern and Resilient Compliance Program

- Leveraging Technology as a Compliance Enabler

- Addressing the Compliance Blind Spot of Voice Interactions

- Common Pitfalls and Your Strategic Implementation Checklist

The New Compliance Imperative in Financial Services

Compliance spending is rising because the old operating model is failing under digital volume, tighter supervision, and higher customer expectations. As noted earlier, RegTech investment is growing quickly in India. The strategic point for directors is simpler. Firms are replacing manual, fragmented controls because those controls are too slow, too expensive, and too hard to defend when regulators ask for evidence.

The compliance question has changed. Boards no longer need proof that policies exist on paper. They need proof that controls work during onboarding, payments, servicing, complaints, collections, and third-party interactions. In practice, that means the institution must show consistent decisions, accurate records, and reliable evidence across every customer touchpoint, including voice calls that many firms still treat as operational rather than regulated interactions.

That shift has real cost implications. Weak data quality creates false alerts, duplicate reviews, delayed remediation, and inconsistent customer treatment. It also creates a credibility problem with regulators because the firm cannot reconstruct decisions cleanly. This article on financial data quality challenges explains that connection well.

The biggest gap is operational, not legal. Many institutions understand their obligations, yet fail when those obligations must be applied in real time by frontline teams, outsourced partners, and customer support channels. Voice is a common weak point. A written policy may be sound, but if an agent gives the wrong disclosure, mishandles consent, or fails to capture an escalation properly, the firm has already created compliance exposure.

Legacy models usually fail for four reasons:

- Manual work dominates control execution: Teams spend time reviewing routine exceptions instead of focusing on higher-risk activity.

- Ownership is split across functions: Compliance, operations, IT, and service teams often apply different standards to the same customer event.

- Evidence is incomplete: Firms struggle to prove what was said, what was approved, and whether the required disclosure or consent occurred.

- Controls do not match customer behavior: Many control frameworks were built for documents and branch processes, while risk now emerges across apps, contact centres, and vendor-managed voice interactions.

I have seen this pattern repeatedly. A bank can pass a policy review and still create avoidable exposure if its call centre scripts, escalation paths, and recording practices are inconsistent. In that environment, execution is the control.

A useful reference point for leadership teams is this overview of compliance in banking, especially when the board needs a shared definition of the full compliance scope before setting investment priorities.

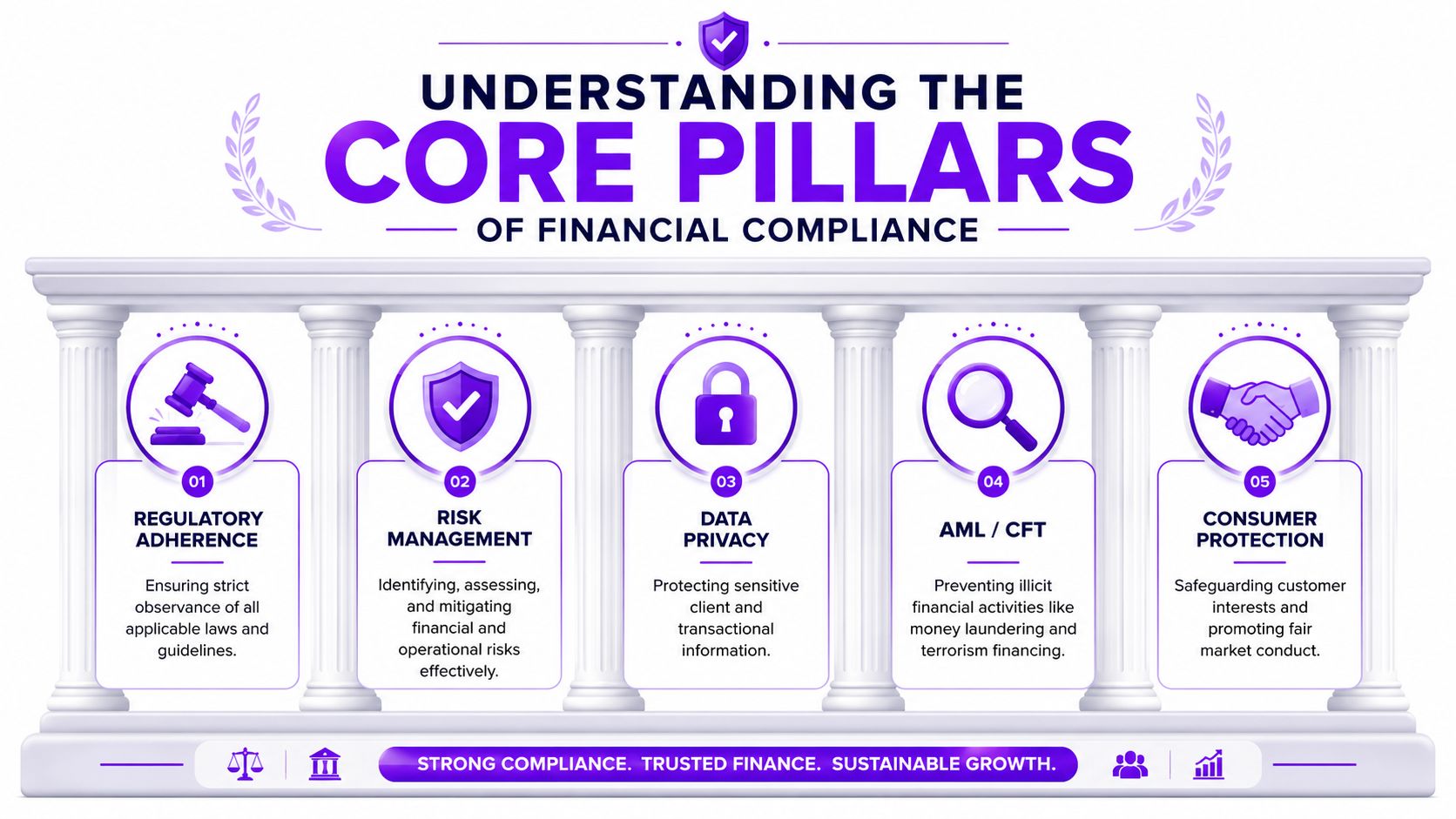

Understanding the Core Pillars of Financial Compliance

The strongest compliance programmes don't treat regulation as a checklist. They treat it as a set of operating disciplines that shape how customers are onboarded, how information is handled, and how risk is detected before it becomes an incident.

AML and KYC as the front door

AML and KYC are the digital gatekeeper of the institution. They determine who gets in, how risk is classified, and what level of monitoring follows.

In India, financial institutions must implement a KYC framework with four specified acceptable identity documents, Passport, Voter ID, PAN Card, and Aadhaar, and the KYC process must be completed within 72 hours of account opening. There is also a strict ₹50,000 threshold for transactions requiring enhanced due diligence, with suspicious activity reports filed within 24 hours of detection (LSEG glossary on regulatory compliance). Whether every institution operationalises this through branch staff, app-based onboarding, or assisted support, the board implication is the same. Delay or inconsistency at the front door creates risk downstream.

A practical example: if onboarding staff or an assisted voice workflow give mixed instructions on acceptable documents, the institution doesn't just frustrate the customer. It creates duplicate reviews, delayed activation, and weak audit trails.

A useful executive refresher on this area is this guide to KYC compliance, particularly for teams trying to align product, operations, and risk language.

Privacy, records, and monitoring as operating discipline

The next pillars are less visible to customers, but they define whether the organisation can defend its decisions under scrutiny.

Consider this simplified view:

| Pillar | What it protects | Business process it changes |

|---|---|---|

| Data privacy | Customer information and lawful handling | Consent collection, storage design, access controls |

| Transaction monitoring | Detection of suspicious activity | Alerts, investigations, escalation workflows |

| Record-keeping | Proof that controls operated | Audit readiness, complaint handling, regulator responses |

| Consumer protection | Fair treatment and accurate communication | Scripts, disclosures, dispute resolution |

| Risk management | Prioritisation of limited compliance resources | Control design, issue remediation, reporting to leadership |

Data retention often gets treated as a legal footnote. It isn't. Retaining too little leaves gaps in evidence. Retaining too much creates privacy and governance problems. Even outside BFSI, teams can learn from adjacent examples like these recruiting data policies, which show how retention rules must match operational realities rather than generic templates.

Strong compliance design answers three questions clearly. What data are we allowed to collect, who can use it, and how do we prove we handled it properly?

Record-keeping is where many firms discover whether their controls are real. A dispute may be handled correctly, but if the institution can't show the timeline, the customer communication, the verification step, and the final resolution basis, the control is weaker than leadership assumes.

For CXOs, the key takeaway is simple. Each compliance pillar changes a core business process. Boards that treat these areas as policy topics miss the bigger point. They are workflow topics, technology topics, and customer experience topics.

Strategic Risk Assessment and Control Frameworks

Reactive compliance is expensive, but the larger problem is timing. By the time a control failure shows up in an audit, complaint trend, or regulator query, the institution has already absorbed the operational damage. In customer-facing environments, especially voice and assisted-service channels, that lag matters. A disclosure missed on a call, an authentication step handled inconsistently, or an escalation not recorded properly can create legal exposure long before the issue appears in a dashboard.

Boards should treat compliance risk assessment as an investment decision. The question is not whether every rule matters. The question is where control failure would create the highest combined cost across enforcement exposure, remediation effort, customer harm, and strategic delay.

That shifts the discussion from policy coverage to business reality.

Why reactive compliance costs more

Reactive programmes spend money after risk has already converted into loss. That spend rarely stops at fines or legal review. It spreads into manual remediation, control redesign, customer outreach, consultant support, backlog growth, and postponed launches. In practice, the commercial cost can be just as serious as the regulatory one. Firms slow product changes, tighten approval layers, and accept more friction in onboarding and servicing because leadership no longer trusts the control environment.

The pattern is familiar. A firm identifies an issue in KYC, complaints handling, communications monitoring, or transaction review. It responds with broad manual checks across multiple teams. Service levels drop. Exception volumes rise. Staff create workarounds to keep queues moving. That introduces a second layer of risk, particularly in high-volume contact centres and branch-assisted channels where decisions happen in real time and evidence is often fragmented across systems.

Voice channels deserve special attention here. Many firms monitor written communications more closely than live conversations, even though calls often contain the highest-risk moments: consent capture, product explanation, vulnerability indicators, complaints, collections language, and dispute handling. If risk assessment ignores those interactions, the framework looks stronger on paper than it is in operation.

A control framework leadership can actually use

Useful frameworks start with customer and employee journeys. They do not start with a spreadsheet of regulations. Review the points where the business makes promises, collects information, gives advice or guidance, approves activity, or refuses a request. Then test whether the control is preventive, detectable, and provable.

For board and executive teams, four questions usually separate mature programmes from superficial ones:

Which journeys create the highest concentration of risk?

Focus on journeys where customer impact, regulatory sensitivity, and transaction volume intersect. Account opening, payments, lending conversations, complaints, collections, and fraud-related support often sit at the top.Do controls operate in the workflow, or beside it?

Controls embedded in systems and scripts hold up under pressure better than controls that depend on staff memory, after-the-fact reviews, or local workarounds.Can the firm prove what happened at the point of interaction?

Evidence matters as much as policy intent. That is especially true for voice, where firms may need to show what was said, what the customer agreed to, whether required disclosures were delivered, and how an exception was escalated.Who owns failure when a control breaks?

Compliance can define standards, but business, operations, and technology must own execution in measurable terms. Shared accountability often turns into diluted accountability unless ownership is explicit.

The distinction between preventive and detective controls is still useful, but leadership teams should view it through a timing lens. Preventive controls stop avoidable failures before the customer is affected. Detective controls help contain damage quickly and show whether the preventive layer is working. In high-risk service environments, waiting for batch reviews or periodic sampling is often too slow.

A simple example makes the point. If a suspicious transaction alert is generated after a delay, while frontline teams continue interacting with the same customer across phone, chat, or branch channels, the institution has a coordination problem, not just a monitoring problem. The same logic applies to customer calls. If required disclosures are checked only through small retrospective samples, management may be measuring quality while missing active compliance exposure.

Strong risk assessments also account for control strain. A control that works at normal volumes may fail during seasonal spikes, product launches, fraud events, or complaint surges. Boards should ask where controls are most likely to degrade under pressure, which channels depend too heavily on manual judgment, and where fragmented records would make regulator response slow or incomplete.

That is where many frameworks break down. They score inherent risk and residual risk, but they do not test operational survivability.

A sound framework gives leadership three things: a ranked view of exposure, a clear case for where investment will reduce future loss, and an honest picture of whether customer-facing interactions, especially voice, are being controlled in real time or reviewed too late to matter.

Building a Modern and Resilient Compliance Program

A resilient compliance programme isn't built by writing more policies. It's built by deciding who owns risk, how behaviour gets reinforced, and how third parties are brought inside the control perimeter. For most organisations, that's where the hard trade-offs sit.

Governance that works in practice

Start with governance that can survive pressure. When volumes rise, new products launch, or customer complaints spike, weak governance shows up fast. Policies get interpreted differently, exception approvals become informal, and issue escalation slows down.

A solid programme has a few essential elements:

- Board visibility: Directors should receive concise reporting on material issues, remediation progress, and channel-specific exposure.

- Executive accountability: The business can't outsource compliance responsibility to legal or internal audit.

- Embedded operating roles: Product, operations, service, and vendor-management teams need named compliance responsibilities in their daily work.

- Escalation discipline: Material control failures need a defined path to leadership, not informal side conversations.

Culture matters here, but not in the abstract. Culture is whether managers reward staff for stopping bad activity, whether service teams know when to escalate a suspicious interaction, and whether commercial teams accept that a delayed sale can be the right decision.

Third-party risk is part of your compliance perimeter

Many firms still treat vendor management as procurement plus security review. That's far too narrow. Financial institutions must adhere to standards like PCI DSS, which require secure networks, data protection, vulnerability management, strong access controls, regular testing, and information security policies. These requirements also govern third-party risk management, because vendor security failures can lead to systemic breaches and trigger immediate regulatory scrutiny (Arctic Wolf on regulatory checklists for financial institutions).

The practical implication is straightforward. If a fintech partner, support vendor, or outsourced service provider handles cardholder information, onboarding conversations, or customer disputes, your institution remains exposed when that vendor fails.

A board-level vendor review should ask:

| Review area | Weak approach | Strong approach |

|---|---|---|

| Due diligence | Collect questionnaires only | Test evidence, review controls, challenge gaps |

| Contracting | General compliance clauses | Specific audit rights, reporting duties, breach obligations |

| Ongoing oversight | Annual tick-box review | Periodic control testing tied to actual service risk |

| Customer interactions | Assume scripts are enough | Validate execution, recordings, complaints, and escalations |

What doesn't work is approving a vendor because its feature set is attractive, then trying to bolt on oversight later. What does work is evaluating customer-facing control design before the contract is signed. That includes disclosure handling, record retention, dispute resolution, and operational resilience.

A modern programme treats every external party with customer or data access as part of the compliance architecture. If they influence customer outcomes, they belong in risk reporting.

Leveraging Technology as a Compliance Enabler

Compliance costs rise quickly when controls depend on manual review, disconnected records, and after-the-fact reconstruction. Technology earns its place when it reduces control variation, speeds evidence collection, and gives management a clearer view of where customer-facing risk is building.

The board decision is not whether to buy more compliance software. It is where standardisation should be built into the operating model, where exceptions should route to human judgement, and how much fragmentation the institution is willing to tolerate before cost and risk start compounding.

Where automation creates value first

Automation usually delivers the fastest return in areas with high volume, repeatable decisions, and a clear evidentiary requirement. Surveillance, onboarding workflows, and case documentation fit that profile.

Three categories tend to justify investment early:

Transaction and behaviour surveillance

Best suited to environments where alert quality is weak, investigators spend too much time clearing obvious false positives, or data sits across separate systems.Workflow-based KYC and due diligence

Effective when onboarding slows because document checks, approvals, and follow-ups still rely on email, spreadsheets, or inconsistent team practices.Audit trail creation across customer journeys

High value when the institution struggles to reconstruct what happened across onboarding, servicing, complaints, or escalations.

The trade-off is straightforward. Automation reduces repetition and improves consistency, but it can also hard-code weak logic at scale. A bad manual process creates isolated errors. A bad automated process creates systemic ones. That is why model governance, exception handling, and clear control ownership matter more than feature breadth.

What disciplined technology decisions look like

A useful test case is assisted onboarding. A customer starts in a mobile app, fails an identity step, and moves to live support. If the support process records the verification attempt, captures consent, timestamps the interaction, and writes back to a central case record, the institution gets lower abandonment, cleaner evidence, and fewer remediation headaches. If the same handoff moves into free-form calls and manual notes, the file becomes harder to defend and more expensive to review.

Voice technology now sits inside that control question, not outside it. DialNexa Labs Private Limited is one example of a provider used for Voice AI support and KYC-related guidance. The value is not the voice layer by itself. The value comes from whether the tool enforces approved workflows, standardises disclosures, captures records in a usable format, and feeds oversight teams with evidence they can test. Firms assessing this area should pay close attention to the FINRA regulatory update on transforming voice AI compliance in finance.

Technology should make the compliant path the easiest path.

Boards should press management on a small set of practical questions. Does the tool improve evidence capture in real customer interactions? Does it reduce variation across channels and teams? Can compliance, internal audit, and operations review the same record without manual reconciliation? Does the implementation lower servicing cost without creating a new monitoring gap?

If those answers are vague, the business case is usually weak. In financial services, good compliance technology does not just automate work. It lowers the cost of control, improves defensibility under scrutiny, and protects customer experience in the moments where risk is created.

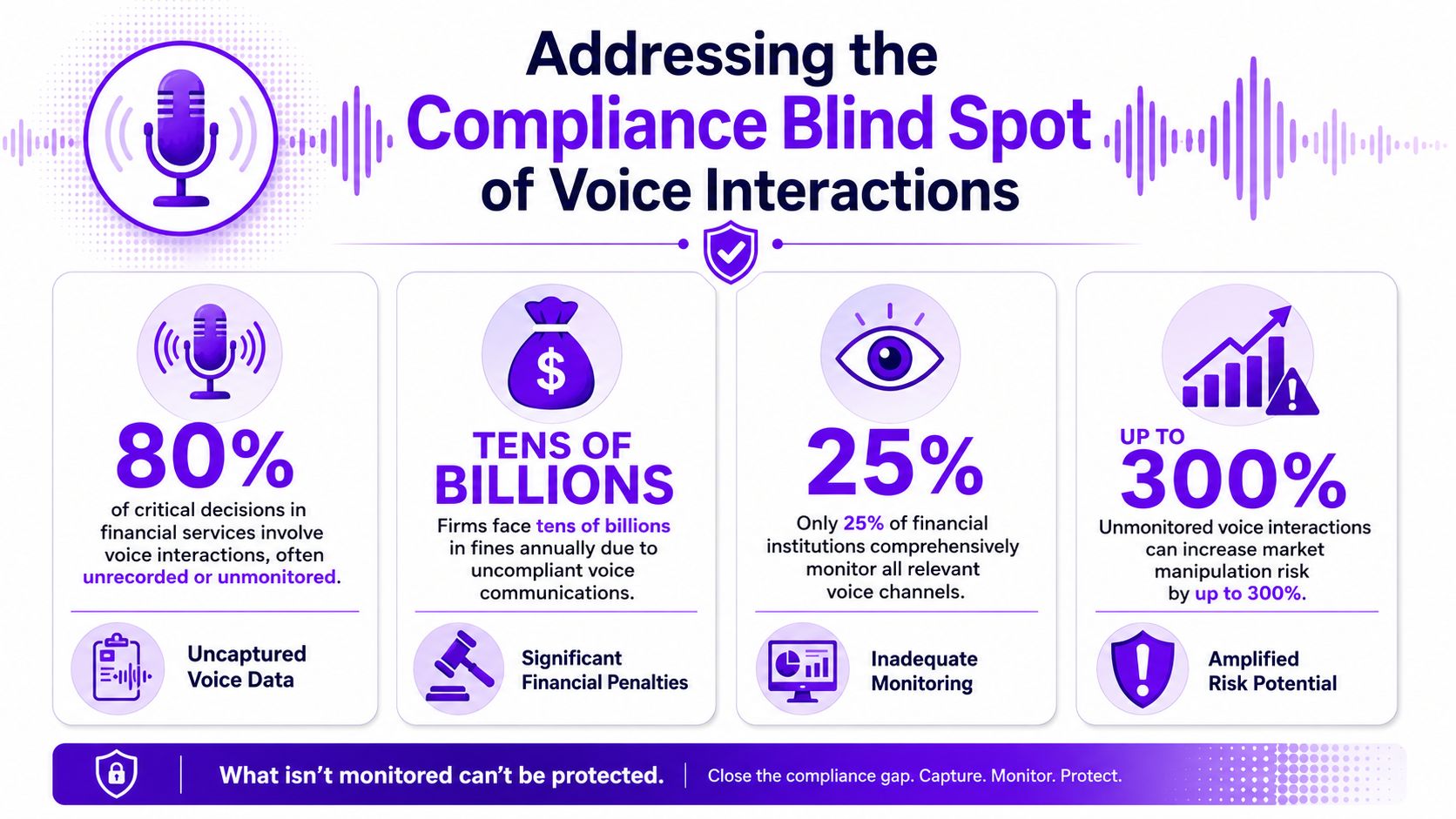

Addressing the Compliance Blind Spot of Voice Interactions

Most compliance frameworks are still document-centric. They monitor forms, transactions, and digital records well enough. They do far less with live conversations, especially when customer service, complaint handling, and dispute resolution sit with outsourced teams or AI-assisted channels. That's a serious blind spot.

Why voice creates a governance gap

Regulators mandate that banks oversee customer service and dispute resolution by third parties, yet a critical gap persists. In AI-driven voice scenarios, connect rates are rising to 91%, while few firms have audit frameworks for qualitative compliance in verbal disputes, creating a significant blind spot (Ankura on the regulatory roadmap for third-party compliance).

That gap matters because many high-risk moments happen in speech, not on forms. A customer asks whether a document is acceptable. An agent explains a dispute process. A collection conversation turns heated. A service partner gives incomplete information. Those are compliance events even when no transaction is posted in that moment.

Common failure points in voice channels include:

- Misstated guidance: Agents improvise answers on KYC, account restrictions, or process timelines.

- Weak consent capture: The firm can't prove what permission was sought or granted.

- Poor complaint handling: Disputes aren't classified, escalated, or resolved consistently.

- Vendor opacity: The institution receives reports on volumes, but not on conversation quality or regulatory adherence.

This short video is relevant because it highlights how voice AI and compliance expectations are starting to converge in financial services.

How to make voice interactions auditable

Boards don't need every call reviewed. They do need a framework that makes voice channels testable.

A practical model includes:

- Approved conversation paths for onboarding, disputes, and sensitive support scenarios.

- Recording and transcription controls aligned to legal and privacy requirements.

- Exception detection for prohibited phrases, missing disclosures, or failed hand-offs.

- Targeted QA reviews focused on regulatory moments, not just customer sentiment.

- Vendor oversight that tests actual interactions, not only reports and policy attestations.

A helpful reference point for teams evaluating this shift is this analysis of FINRA's regulatory update on Voice AI compliance in finance. The broader lesson applies even beyond that specific context. Voice can no longer sit outside the compliance operating model.

If customer risk is created in conversation, compliance evidence must also be captured in conversation.

Common Pitfalls and Your Strategic Implementation Checklist

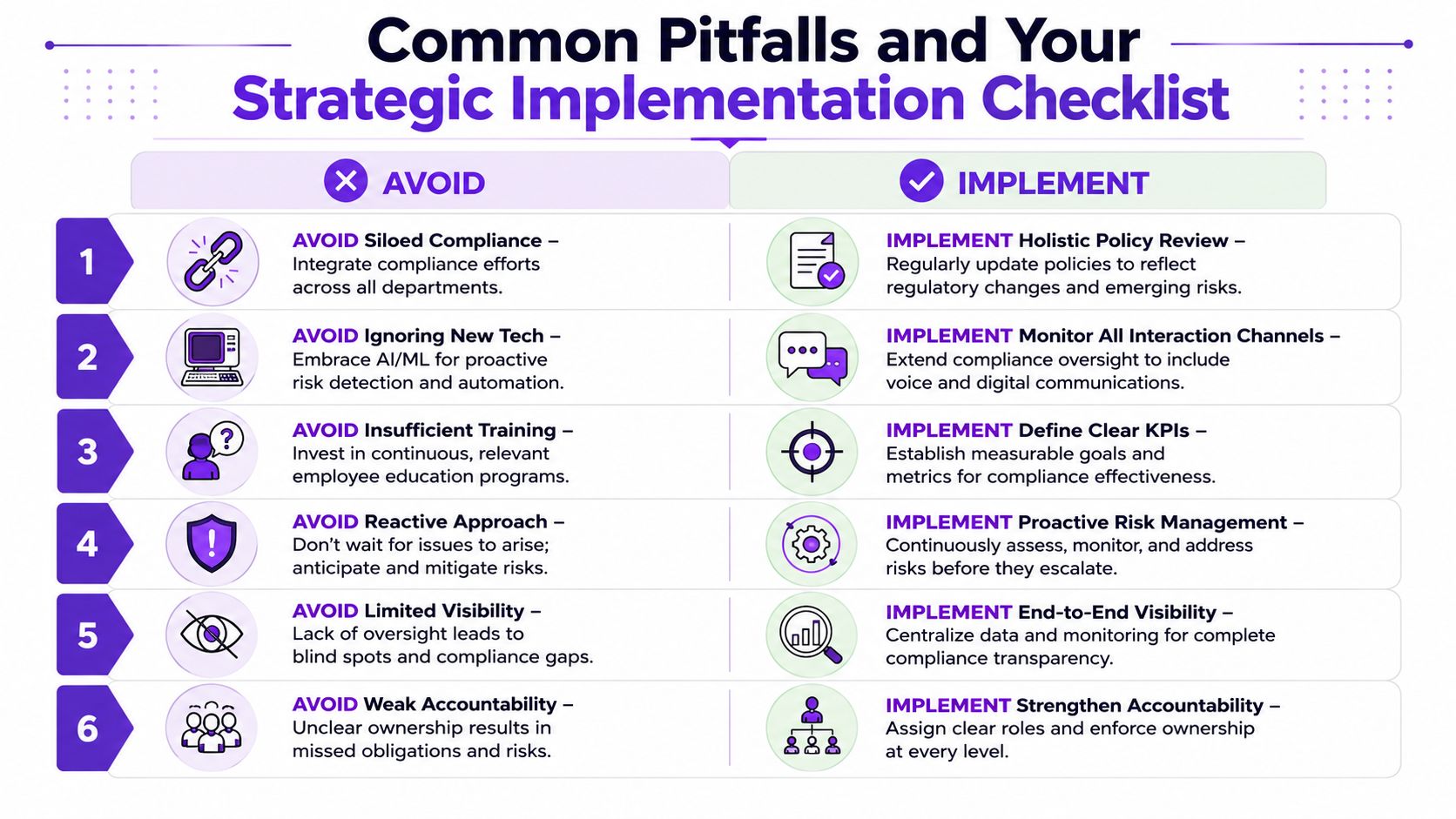

Financial services compliance programmes rarely fail because leaders don't care. They fail because execution drifts into silos, old assumptions, and partial visibility. The same mistakes show up repeatedly across institutions that otherwise appear mature.

The mistakes that keep recurring

The first mistake is treating compliance as an IT or legal problem. It isn't. It's an operating model issue that cuts across customer journeys, data ownership, service quality, and vendor oversight.

The second is relying on training that teaches policy text but doesn't prepare frontline teams for real conversations, judgment calls, and escalations. The third is assuming third-party providers are outside the main risk perimeter once contracts are signed. They aren't.

Other recurring weaknesses include:

- Siloed controls: Teams monitor their own area but miss the full customer journey.

- Evidence gaps: Decisions are made correctly, yet the institution can't prove how or why.

- Legacy reporting: Boards receive lagging indicators instead of actionable risk signals.

- Channel blind spots: Voice, assisted support, and outsourced interactions stay under-governed.

Board-level implementation checklist

Use this as a strategic self-audit.

- Board oversight: Is the board reviewing compliance exposure in operational terms, not only policy and audit summaries?

- Journey mapping: Have we mapped the highest-risk customer journeys end to end, including hand-offs between teams and vendors?

- Control design: Are preventive and detective controls clearly separated, owned, and tested?

- Data governance: Can we prove data lineage, access control, record retention, and localisation where required?

- Third-party assurance: Do we test how vendors handle customer interactions, disputes, and sensitive information in practice?

- Voice governance: Are customer-facing calls and AI-assisted interactions captured, reviewed, and auditable where they create compliance risk?

- Technology fit: Do our tools reduce manual variation and create evidence automatically, or have they added another silo?

- Frontline readiness: Can managers show that staff know how to escalate unusual behaviour, not just recite policy terms?

A board that can answer those questions with evidence, not assumptions, is in a stronger position. Compliance then becomes more than defence. It becomes a cleaner way to scale products, partnerships, and customer service without multiplying unmanaged risk.

If your team is rethinking how compliance should work in customer-facing conversations, DialNexa Labs Private Limited is worth evaluating as part of that discussion. The company builds Voice AI agents for support, qualification, and KYC-related guidance workflows, which makes it relevant for BFSI teams that need more structure, consistency, and auditability in high-volume voice interactions.

Leave a Reply